Personal Wealth Management / Economics

Japan’s Quantitative Easy Button

Is Japan taking the easy way out with its uncompetitive economy?

Can Prime Minister Shinzo Abe implement what Japan’s economy really needs? Photo by Brendan Hoffman/Getty Images.

Do economies come with an Easy button? Japanese Prime Minister Shinzo Abe sure seems to think so! Recession? Hit the fiscal stimulus button! Deflation? Hit the monetary button! (Again and again!) Uncompetitive economy? Hit the ... err ... there isn’t an app for that. Reforming an antiquated system takes actual reform—no easy task. And despite promising big reforms upon taking office last December, Abe has yet to do much. Instead, he’s seemingly relying on his Easy buttons for a quick fix. In the near term, it might appear to be working—Japan is growing! But under the hood, data show the economy isn’t broadly benefiting. Without deeper, politically difficult change, it’ll be tough for Japan to meet investors’ still-lofty expectations.

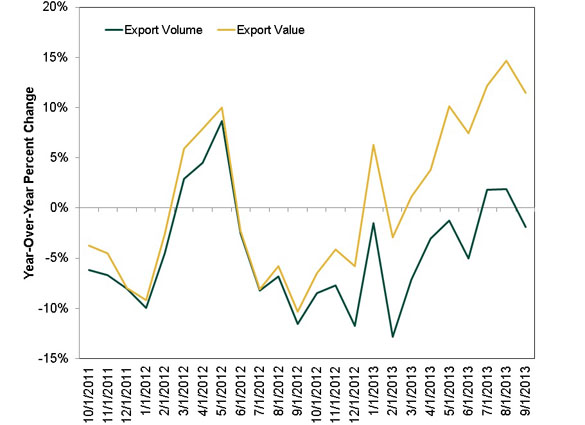

Take recent trade data. Due in part to the Bank of Japan’s bond buying program—quantitative and qualitative easing or QQE—the yen is the weakest it’s been in years. This was one of Abe’s secondary goals—in theory, a weak yen makes exports more competitive, ideally boosting exporters’ profits. Right on cue, export values jumped, and they gained another 12% y/y in September. But if you think this means an export revival in Japan, think again. Export volumes haven’t kept pace—they fell y/y for 2013’s first six months, grew a bit in July and August, then dropped -1.9% in September. (See Exhibit 1) In other words, the weak yen isn’t driving output gains—and all that come with them, like rising business investment, corporate growth and many other downstream benefits. It’s just allowing exporters to make more money on each sale abroad through a currency conversion benefit. Great for their profits, but not exactly a shot in the arm for the broader economy.

Exhibit 1: Year-Over-Year Japanese Export Volume vs. Export Value

Source: FaceSet Data Systems, Inc. and Japan Ministry of Finance, as of 10/21/2013.

Plus, only one subset of businesses reap even this small benefit. The weak yen also raised import costs, so any business importing any good or service faces big headwinds to profit growth. Which is pretty much all Japanese firms these days, given how much energy the country must import in the wake of the Fukushima-Daiichi 2011 nuclear disaster. Ditto for households, which also face higher energy costs. Any manufacturer importing raw materials or intermediate components also takes a hit. This includes many of Japan’s exporters—few goods are made start to finish in Japan. For some of these firms, the weak yen could very well be zero sum! And for the broader economy, it hasn’t yet provided a net benefit—it merely created winners and losers. Based on some recent statements, Abe still seems to expect the weak yen to boost profits for all, but as long as imports stay so darned pricy, it’s tough to see this playing out as he expects.

For Abe to get his wish, he likely needs to tackle the difficult task he has thus far put off: structural economic reform. Since his campaign, Abe has talked about this. A lot. Corporate tax cuts! Labor reforms! Tax incentives for mega-conglomerates to restructure! Free trade! But talk is cheap—actions matter, and so far, actual progress is rare. In June, after delegating reform to a group of party stalwarts, the old guard of corporate Japan and a few entrepreneurs, he previewed a rather shallow package of hazy long-term growth targets, measures to get more women in the workforce and the odd incremental tax adjustment—far from a tangible, actionable roadmap for long-term growth, and far from the politically contentious changes necessary to spur lasting growth. With upper house elections due in July, many gave Abe a free pass—perhaps he was saving the hard stuff until after his Liberal Democratic Party consolidated power! And sure enough, just before the late July contest, Abe claimed another round of reforms would hit in September. Yet here we are in late October, and all anyone has seen is a sales tax hike and the world’s most counterintuitive fiscal stimulus package.

Looking ahead, it’s possible Abe could come through with a sweeping plan for change, but we’d suggest not holding your breath. Last week, Japanese outlets reported Abe has put important labor reforms on ice due to heavy resistance—a reoccurring theme in recent Japanese politics. Labor reforms are a third rail in the Land of the Rising Sun. The labor code safeguards the culture of lifetime employment—a huge albatross on businesses. Most firms can’t cut payroll as they normally would when times are lean, so they have to cut investment. Even when times are better, a roster of lifetime employment contracts gives firms little wiggle room to invest in more growth-oriented endeavors. The antiquated labor code is a big reason business investment has overall fallen since 1997—one of Japan’s biggest drags on growth.

Abe and his deputies know Japan will benefit tremendously from change, but change is hard. For now, Abe seems to be allowing vested interests to thwart reform, in hopes the weak yen will boost profits enough for firms to increase capex without labor reforms. In Q2, he got his wish—profits jumped 8% y/y, supporting a rare capital expenditure increase. But he can’t rely on the Quantitative Easy button to paper over the cracks forever. Investors still have high expectations for Japanese growth and policy. But absent meaningful structural change, reality likely disappoints, and better investment opportunities probably exist outside the Land of the Rising Sun.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30 -

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today