Personal Wealth Management / Economics

Japan's Sales-Tax Rerun

Q4 GDP data suggest the government’s attempt to mitigate the impact of October’s sales tax hike may have worked a teensy bit.

On Monday, official Japanese data confirmed what everyone already knew: GDP contracted in Q4, in the wake of October 1’s sales tax hike. But the magnitude was a surprise. The median forecast was -3.7% annualized. The actual: a -6.3% annualized drop, with all major categories except public spending negative.[i] Some interpret the worse-than-expected reading as a sign Japan is extra vulnerable to the coronavirus’s potentially corrosive effects, arguing a recession (using one common definition) is likely. We don’t think there is much benefit from trying to forecast this, considering stocks have already seemingly moved on from the virus and a weak Japanese economy isn’t new news. But there are some interesting nuggets under the hood that may hint at whether this sales tax hike is affecting Japanese demand as much as the last one did in April 2014.

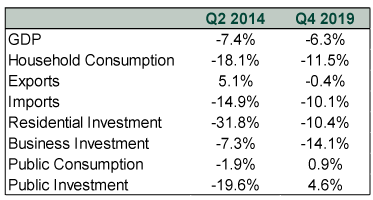

Exhibit 1 shows GDP and select components from Q4 2019 and Q2 2014—each the first quarter after the sales-tax hike to register the immediate impact on behavior. You wouldn’t know it from the tenor of today’s commentary, but results are overall better this time around.

Exhibit 1: Then and Now

Source: FactSet, as of 2/18/2020. All figures are at seasonally adjusted annualized rates.

One obvious difference between then and now: the government. Most expected 2014’s tax hike to disrupt consumption, but there was also a prevailing belief that the BoJ’s aggressive quantitative easing would be sufficient stimulus to cushion the blow. Five and a half years of sluggish growth and negligible inflation later, that mindset has largely faded. Plus, in contrast with 2014, Japanese exports have been weak for several quarters due to the global manufacturing rough patch. So the government turned on the fiscal stimulus spigots.

That will naturally raise questions over how much credit fiscal stimulus should receive for the smaller decline in household spending this time around. The answer will be impossible to determine, considering how many other variables were at play. In addition to exempting some household items from the tax hike, officials adjusted taxation of big-ticket items to reduce the incentives to front-load major purchases before the tax hike took effect. There is some evidence this worked as intended. In the quarter before 2014’s tax hike, household spending jumped 8.8% annualized.[ii] But in Q3 2019, on the eve of October’s hike, it rose just 1.7% annualized.[iii] Imports—which represent domestic demand—jumped 26.5% in Q1 2014 but climbed just 2.8% in Q3 2019.[iv] With a little less noise this time, it could mean the impact will be short-lived, but only time will tell.

The grand economic consensus still expects Japanese GDP to rebound a bit in Q2, as it did in Q3 2014, avoiding the consecutive GDP declines that fit the common definition of recession. Maybe that comes true, or maybe weakness persists a while longer. Maybe domestic demand stabilizes but exports stay weak. Whatever happens, we wouldn’t read too much into it—weak domestic demand and export-reliant growth have been the main features of Japan’s economy for years now, long before “coronavirus” was making a run for word of the year. Also, by the time Japan’s Q1 data come out, we will be halfway through May, and the glorious warm weather of spring will likely have rendered the virus a distant memory. Stocks will probably see Japan as they do now—a country whose huge multinationals have much better prospects than companies relying on domestic demand. We think now is a time to focus on that big picture and avoid getting hung up on data wiggles.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today