Personal Wealth Management / Economics

Jobless Claims’ Uptick Isn’t a Recovery Red Flag

New bull markets generally don’t need a strong job market to thrive.

Initial jobless claims increased more than expected last week, crossing back above one million. As we would expect in a young bull market, most coverage argued a deteriorating labor market is holding back the economic recovery. We won’t argue everything is in fantastic shape, and job losses are indeed devastating for those directly affected. However, when assessing how economic developments and stocks interact, we think it is important to tune down any emotional response and turn a more critical eye to the data. Do so, and we think you will find unemployment data are backward-looking, and stocks don’t wait for a strong job market to rise.

Initial jobless claims rose by 129,000 to reach 1.1 million in the week ending August 14.[i]

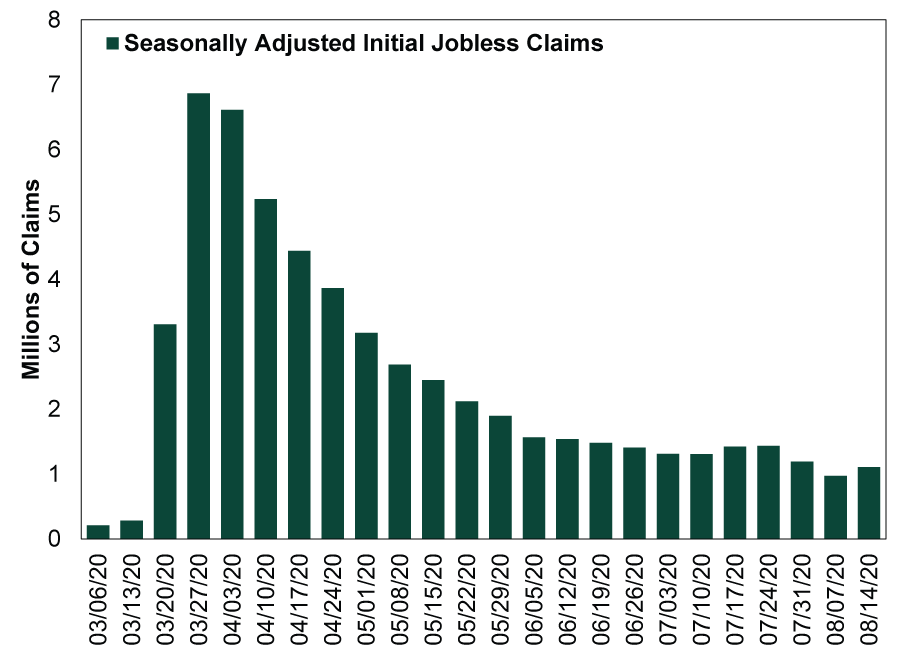

Exhibit 1: Weekly Jobless Claims

Source: FactSet, as of 8/20/2020. Weekly initial jobless claims, 3/6/2020 – 8/14/2020.

While this looks (and is) very bad, there are a couple of caveats. First, unemployment data—which are often subject to heavy revision—are especially squishy right now. COVID restrictions are disrupting normal job market patterns—like restaurant and tourism-related summer hiring—and thus throwing off seasonal adjustment. Unadjusted jobless claims rose much less last week—just 52,776, to 892,000.[ii] In prior weeks, seasonal adjustments intended to scrub the impact of auto factories’ scheduled maintenance transformed unadjusted declines in jobless claims into increases.

Another data oddity: While over 28 million Americans were receiving state or federal unemployment benefits as of August 1, the BLS’s monthly household survey showed 16.3 million unemployed.[iii] The discrepancy may point to double-counting or overlap between state and federal jobless benefit programs. The point here isn’t to say one data series is more accurate or telling than another. Rather, it suggests drawing big conclusions from any single data point is unwise.

Regardless, headlines bemoaned jobless claims’ climbing back above one million. Said one economist quoted in The Washington Post, “I would definitely call it a canary raising alarms in the economic coal mine.”[iv] We agree labor market conditions are still quite bad, and businesses aren’t in perfect shape. Anecdotally, many small businesses that survived the initial lockdown have begun succumbing to the devastating effects of prolonged COVID restrictions keeping their doors shut and/or limiting the number of customers they can serve. For the many small businesses operating on thin margins in the best of times, such long-lasting disruptions can be a death sentence, putting their owners and employees out of work.

Yet at a higher level, the overall picture doesn’t seem very different from a typical recession, when small businesses risk folding as they run low on customers and credit. This is hugely painful for business owners and workers, and we don’t dismiss the stress and suffering of either. But these drawbacks have never prevented an economic recovery from taking root. Jobless claims and unemployment typically remain elevated well after recessions and bear markets end. The reason: Bankruptcy and unemployment numbers reflect past economic damage, not future—particularly today, given state governments are struggling to process far more unemployment applications than they are accustomed to.

In our view, investors ought to imitate markets and not read too much into terrible jobs data. We have ample evidence from both this and past early-stage bull markets that woeful labor market conditions don’t impede forward-looking stocks. The previous global bull market began on March 9, 2009—yet jobless claims peaked at March’s end and didn’t revert to pre-recession lows for almost three years.[v] Their descent wasn’t smooth—there were several short-lived increases along the way. Jobless claims were similarly jagged after the bear market that ran from 11/20/1980 – 8/12/1982. They peaked in early October 1982, nearly two months after stocks bottomed out, then had a choppy recovery to pre-recession levels over the next year.[vi]

In our view, the heavy focus today on jobless claims’ allegedly troubling signals underscores the extent to which observers, overall and on average, appear to be out of sync with stocks. Observers seem to be dwelling on the near future, while we think stocks are focusing on the longer end of the 3 – 30 month time window they typically price—as they generally do in new bull markets. At such times, we think markets—reasonably—anticipate a world with viable COVID treatments or one that has learned to live with the virus.

Given the fact labor market weakness is a near-constant headline presence, we don’t think it has the surprise power to knock markets. Rather, with sentiment still so pessimistic, we think there is plenty of room for reality to keep surprising to the upside, fueling this young bull market.

[i] Source: Department of Labor, as of 8/20/2020.

[ii] Ibid.

[iii] “New Unemployment Claims Top 1 Million. Again.” Eli Rosenberg, The Washington Post, 8/20/2020. Also, Bureau of Labor Statistics, as of 8/20/2020.

[iv] “New Unemployment Claims Top 1 Million. Again.” Eli Rosenberg, The Washington Post, 8/20/2020.

[v] Source: Federal Reserve Bank of St. Louis, as of 8/20/2020.

[vi] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis On the Iran Flare Up2026-07-08

-

Expert Commentary 3 Things You Need to Know This Week | Midterm Miracle, US Jobs, Tax Planning

2026-07-07

2026-07-07 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 29 - July 32026-07-07

-

Market Analysis Can Germany Engineer Faster Growth at Last?2026-07-07

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today