Personal Wealth Management / Market Analysis

Jobs Marched on in March

Whatever your gauge, the US economy added jobs in March.

Stocks fell Friday amid talk of escalating trade tensions between China and the US. The BLS seemed to add to the bad news, reporting US nonfarm payroll employment rose by just 103,000 in March—short of expectations for 185,000 and the smallest gain in six months. Some even argued trade worries may have affected hiring decisions. But wait! Two days earlier, another closely watched employment report said hiring was “rip-roaring” in March as the private sector added 241,000 jobs. So which is right and which is wrong? In our view, there is no clear answer. Rather, this difference highlights why investors should consult a broad swath of data when assessing the state of the economy rather than rely on a single econometric as all-telling.

While both the BLS’ Employment Situation Summary and the ADP’s National Employment Report track employment, their approaches differ. The BLS surveys employers nationwide, reaching about 149,000 businesses and government agencies. ADP focuses on the private sector and uses live payroll data. Both approaches have pros and cons. The BLS’ survey is more comprehensive, but it’s also subject to more revisions, and surveys aren’t airtight. Its initial report often gets updated—sometimes significantly—and the margin of error is large. ADP’s data are less volatile and typically have smaller revisions, but the firm serves only about 20% of the US private sector, and its client base’s sectoral makeup isn’t perfectly in line with the broader economy, forcing statisticians to do some scrubbing. Moreover, neither report counts all workers, missing folks like private household workers or unpaid family workers.[i] So while both provide a snapshot of the employment situation, neither is all-encompassing.

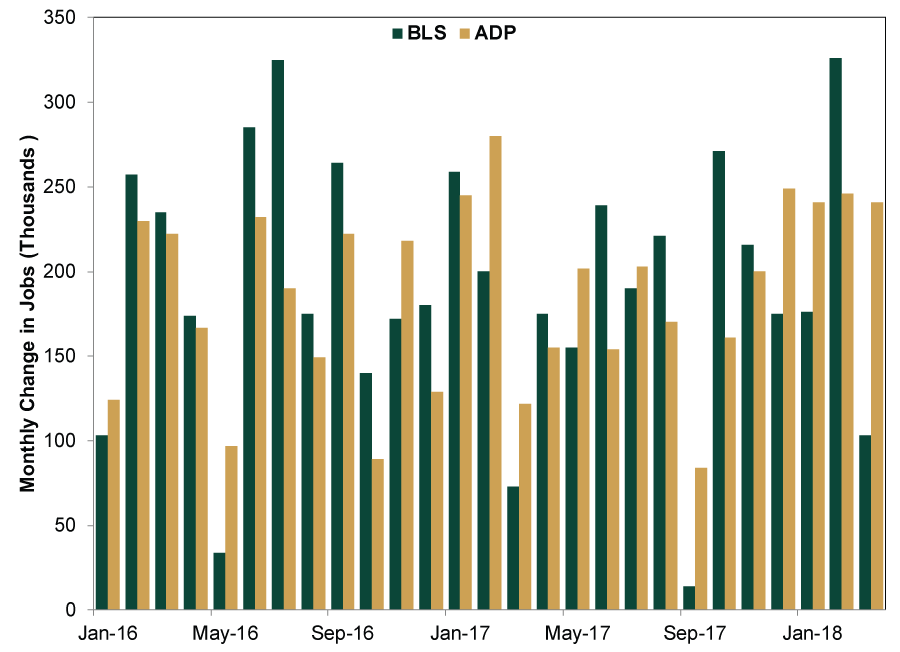

While the March difference between the two reports seems big, it isn’t uncommon. Just last month, the BLS’ payroll survey said February nonfarm payroll employment climbed by 326,000 jobs compared to the ADP’s 246,000 gain. Exhibit 1 shows the monthly change in payrolls for both the BLS and ADP since January 2016. Sometimes they are close, but sometimes they aren’t.

Exhibit 1: How Do the BLS and ADP Compare?

Source: FactSet and ADP Research Institute, as of 4/6/2018. January 2016 – March 2018.

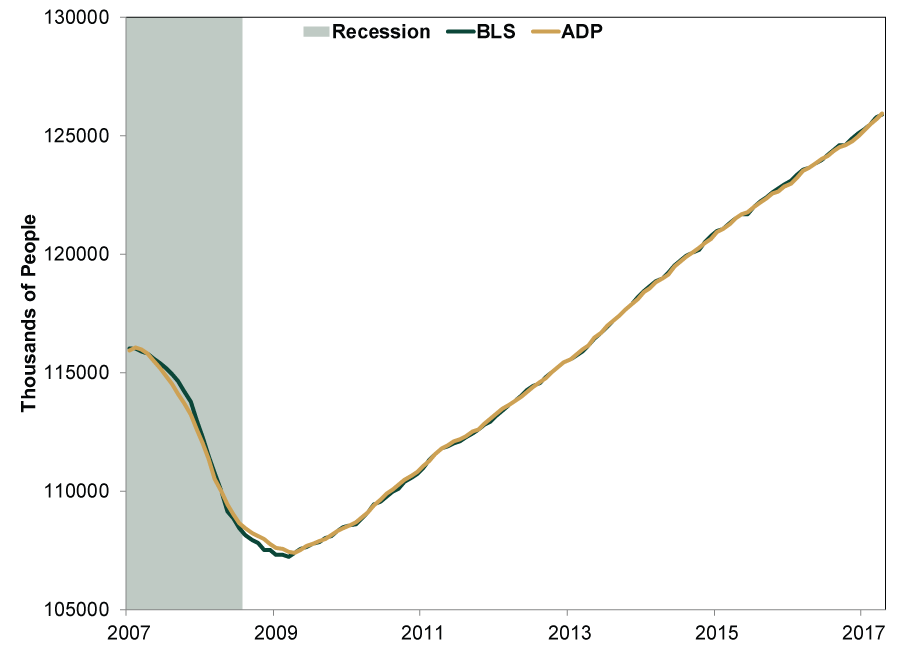

However, when taking a longer view, both show the same trend. Exhibit 2 gives a more apples-to-apples look by comparing how the ADP and BLS track total nonfarm private employment—there isn’t much difference in their findings.

Exhibit 2: Private Payrolls Since the Last Expansion’s Peak

Source: BLS, St. Louis Federal Reserve and NBER, as of 4/10/2018. Monthly total private employees (all employees) and monthly total nonfarm private payroll employment, December 2007 – March 2018. NBER recession dating used.

Both datasets paint the same picture: The private sector has kept adding jobs over the past nine years, consistent with an expanding economy.

Despite the BLS’ weakest number in six months, jobs data overall still look good. There may be some weather skew: An unusually warm February may have boosted some sectors like construction, and a cool start to spring could have driven a pullback. Future reports may end up showing some substantial revisions. For investors, though, backward-looking jobs data tell you nothing about what is to come. They are confirmation of an expanding economy—not an indication of further growth. However, other forward-looking indicators suggest growth will continue for the foreseeable future—an important driver underpinning the bull market.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today