Personal Wealth Management / Economics

Keeping Score on GDP in Q4

Data show the global economy ended 2017 on a solid note.

Politics have dominated headlines in the US and UK to start the year. In the US: government shutdowns; DACA deal-making; Davos speeches! In the UK: Brexit; cabinet reshuffling; Davos speeches! With all that noise, it would be easy to lose sight of less-heralded news items, like steady economic growth—something both the US and UK delivered at the end of 2017. While that is in the past, we expect these solid fundamentals to persist into 2018, supporting profits—and stocks.

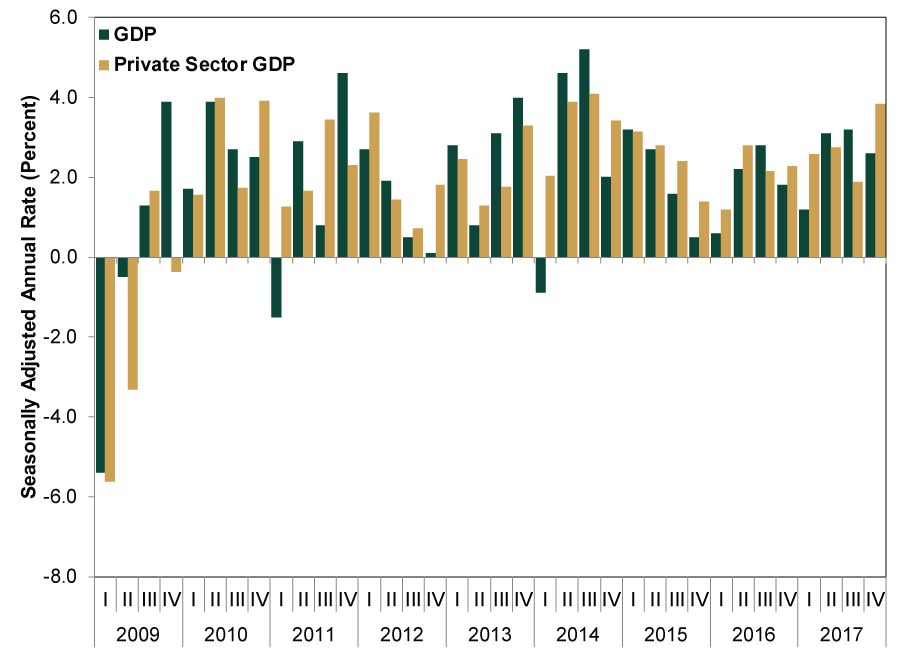

In 2017, US GDP expanded 2.3%, up from 2016’s 1.5% rate. Looking at the more recent data, the economy grew 2.6% annualized in Q4, slowing from Q3’s 3.2%. However, this slowdown doesn’t look worrisome. For one, consumption is healthy: Personal consumption expenditures grew 3.8%, jumping from Q3’s 2.2%, as spending on both goods and services picked up. Nonresidential fixed investment (i.e., business investment) growth accelerated from 4.7% to 6.8% thanks to a rebound in structures investment and continued growth in equipment and intellectual property products. Trade was even more robust. Exports rose 6.9% from Q3’s 2.1% while imports popped from -0.7% to 13.9%. The latter’s big rebound is related to activity at Gulf of Mexico ports, which was delayed due to Hurricane Harvey. While imports aren’t bad for the economy—they represent domestic demand—GDP calculates them as a negative. In Q4, they detracted -1.96 percentage points from headline growth, the most since Q4 2009.

Zeroing in on the private sector—namely, private consumption expenditures, business investment and residential investment—Q4 was the strongest quarter since Q3 2014—and the fifth-strongest in this expansion.

Exhibit 1: The US Economic Expansion Since 2009

Source: US Bureau of Economic Analysis, as of 1/26/2018.

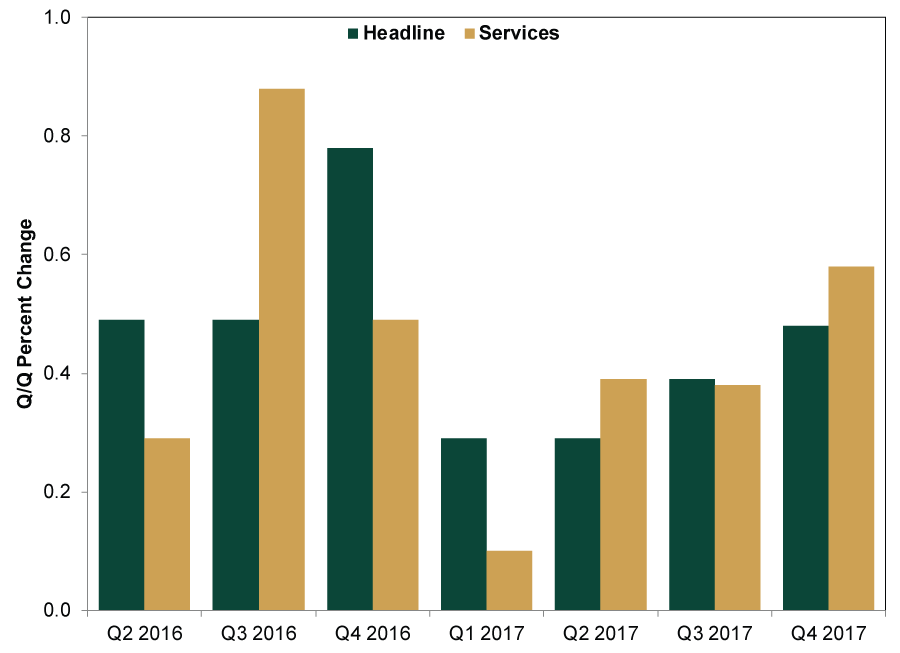

Meanwhile, in the UK, the expansion remains intact despite all those dire Brexit warnings saying otherwise. UK GDP grew 2.0% annualized (0.5% q/q) in Q4—the fastest rate of 2017. The services sector, which comprises about 80% of the economy, accelerated to 0.6% q/q and contributed 0.45 percentage point to headline growth. The production sector also grew 0.6%, with the manufacturing component rising 1.3% and adding 0.13 percentage point to growth. Though smaller sectors—namely agriculture and construction—contracted, services and manufacturing combined account for nearly 90% of GDP. Despite the constant Brexit handwringing, those dour forecasts of a plunging economy haven’t come to pass.

Exhibit 2: Who’s Afraid of Brexit?

Source: FactSet, as of 1/29/2018.

While it is still early in GDP reporting season, some other major players have released their numbers, too. The 19-member eurozone grew a 19th straight quarter, expanding 2.3% annualized (0.6% q/q). Economic reality in Europe remains far better than appreciated. Chinese GDP rose 6.8% y/y in Q4 and 6.9% for 2017—above the government’s target rate of around 6.5% and defying those “hard landing” fears. The Philippines grew 6.6% y/y in Q4 as household spending rose 6.1% and government spending grew 14.3%—its fastest rate since Q4 2015. South Korean Q4 GDP rose 3.0% y/y, though it contracted -0.2% on a quarterly basis. However, a 10-day autumn holiday and strong Q3 growth—which set a high bar to beat—are to “blame.” Exports contracted largely due to a “slump in sectors including automobiles and ships,” but tech exports like semiconductors and other electronics remained strong. Consumption and investment figures also remained solid—a sign the South Korean economy is benefiting from the tailwinds propelling the global expansion.

Looking ahead, forward-looking indicators like The Conference Board’s Leading Economic Index (LEI) point positively. US LEI rose 0.6% m/m in December, with ISM’s New Orders, the Leading Credit Index and the interest rate spread contributing the most. All three components bode well for further expansion. Governments remain gridlocked, but as the UK exemplifies, this isn’t a negative—it decreases the likelihood radical legislation shocks markets. Overall, these data support our view that the US, UK and the rest of the global economy will likely keep growing this year—a big reason to expect more bull market ahead.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Volatility By the Numbers: 2026’s ‘Volatility’2026-06-12

-

Expert Commentary This Week in Review | IPOs, US Inflation, ECB Rate Hike

2026-06-12

2026-06-12 -

Expert Commentary Think Twice Before Buying an IPO

2026-06-11

2026-06-11 -

Market Analysis Are World Oil Reserves Dangerously Low?2026-06-11

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today