Personal Wealth Management / Market Analysis

Ken Fisher: “Nothing Is Better—Stocks Are Stocks.” Even Small Caps.

A check-in on market leadership by size.

Mere months ago, you couldn't venture too far onto the World Wide Web without some pundit telling you small-cap stocks are the bee's knees. After all, small caps' long-term average annualized return beats the broader market, and they're ahead during this bull market. Open and shut case, they argued. So it might surprise you to know small caps are down this year. While the broader market is up. It might also surprise you to know small usually falls behind as a bull market matures. As our boss, Ken Fisher, wrote in the Financial Times in June, "Nothing is better-stocks are stocks. Every category, correctly calculated, has its day in the sun and also the rain." There is mounting evidence clouds may be gathering, dimming small cap's shine.

The myth of small caps' permanent superiority stems from the category's long-term and recent returns. From 1926 through 2013, small caps returned roughly 11.5% annualized-slightly higher than large cap's-represented by the S&P 500-10%.[i] Small cap also led for much of this bull market's first five years, leading many to extrapolate its leadership forward. But as Ken also wrote in that June Financial Times piece, "that's recency bias and a great way to lead yourself to trouble." Past performance, as ever, doesn't predict future returns.

Small cap's leadership is largely cyclical. It does great early in a bull-small caps usually get hammered the hardest late in a bear, then bounce disproportionately off the bottom. That high long-term return stems from some really, really big bounce-back years, like the early goings of the bull markets that began in 1932, 1942, 1974 and 2002. As bulls age, small fades and big does better.

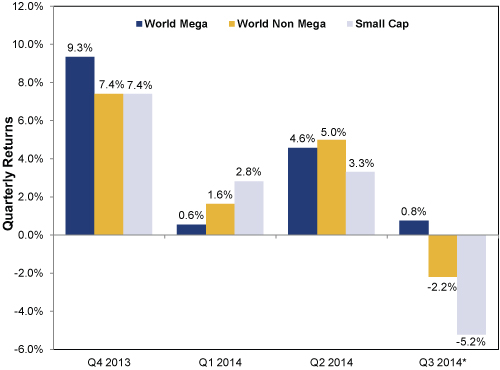

This seems to be where we are now. Year to date, the Russell 2000-a small cap-heavy US index-is down -3.0%, while the S&P 500 is up +8.9%.[ii] This is not just a US phenomenon, either. Size leadership has been choppy for the past year, with small leading in only one quarter. Exhibit 1 shows global small cap's performance compared to other major size categories over the last three quarters and Q3 to date.

Exhibit 1: Small Cap vs. Big and Mega

Source: FactSet, as of 9/24/2014; MSCI World and MSCI World Small Cap Total Returns from 9/30/2013 to 9/23/2014. World Mega returns are the market-weighted total returns of stocks greater than the weighted average market cap of the MSCI World rebalanced annually on December 31.

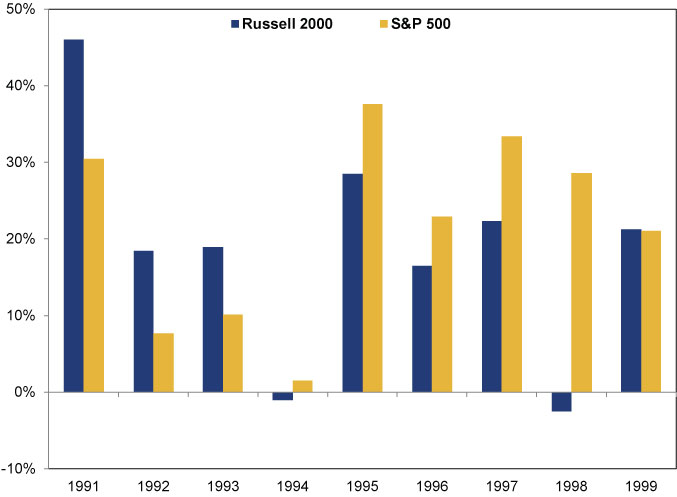

We saw something fairly similarly in the 1990s bull. Small cap led from 1991 to 1993, then trailed the next five years. The Russell 2000 fell in 1998-a year the S&P 500 finished up 28.6%-as the category took it on the chin during the Asian currency crisis. Small did edge out big by a hair in 1999, but that's largely tied to the run-up in smaller tech stocks as the bubble reached its zenith. Junky IPOs that punch above their weight tend to be small, not big.

Exhibit 2: Russell 2000 vs. S&P 500 During the 1990s Bull Market

Source: FactSet, as of 9/24/2014. Russell 2000 Total Return from 1/1/1991-12/31/2000. S&P 500 Total Return from 1/1/1991-12/31/2000.

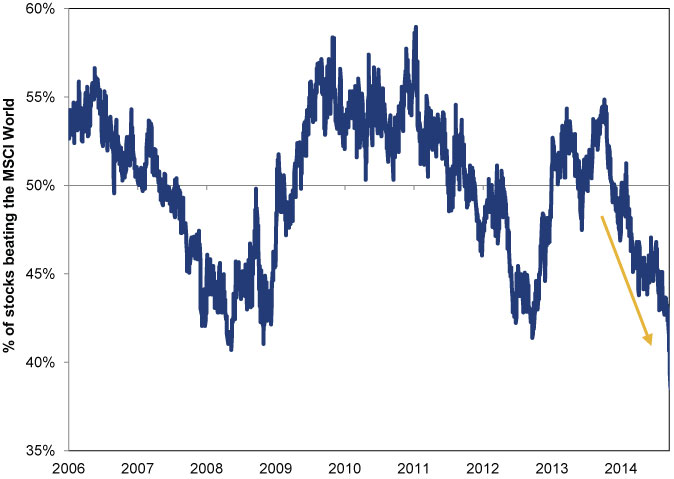

Another way to see this budding leadership transition is market breadth-the number of companies outperforming an index. As the bull progresses and leadership transitions away from small caps, market breadth narrows-more stocks are smaller than the index's weighted-average market cap than bigger. Over a trailing 12-month period, the MSCI World's market breadth has decreased since October 2013. As of September 19, 2014, only 39% of MSCI World's stocks are beating the index. No indicator is perfect-this one has a big false read in 2012-but this is consistent with history, and overall holds true.

Exhibit 3: Market Breadth for the MSCI World Total Return

Source: FactSet, as of 9/23/2014. MSCI World Total Return 12/30/2005-9/23/2014. Uses prior EOY constituents, rebalanced annually. Market breadth refers the percentage of companies whose trailing 12-month returns are beating the index's trailing 12-month returns.

You can see this variance in other indexes, too. One widely circulated factoid last week was that 47% of NASDAQ stocks are in a bear market-they've fallen 20% from their peaks over the last 12 months. Yet the index itself is up 22.4%. 40% of the Russell 2000's stocks are in the same (sinking) boat. Many of these laggards are in both indexes-and those overlapping names are, by definition, small caps. The bigger companies in the NASDAQ are doing a-ok.

Don't get us wrong. We aren't suggesting small caps are destined to go down looking forward-they're just likelier to lag bigger stocks than lead as the bull continues. Pundits might still insist the recipe for success as this bull ages is finding the right hot small stocks and buy the dips, but history and fundamentals suggest big and boring is the way to go.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Morningstar, FactSet and Global Financial Data, Inc., as of 6/2/2014. Small cap returns are based on the Ibbotson Associates Small Stock Total Return Index from 1/1/1926-12/31/1978 (Morningstar) and the Russell 2000 from 1/1/1979-12/31/2013 (FactSet). Big cap returns are based on Global Financial Data's S&P 500 Total Return Index from 1/1/1926-12/31/2013. Monthly data are used through 12/31/1987; daily data are used thereafter. For periods beginning prior to 12/31/1987, first-year returns are computed from the end of the month.

[ii] FactSet, as of 9/24/2014. Russell 2000 Total Return 1/1/2014-9/23/2014. S&P 500 Total Return 1/1/2014-9/23/2014.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Big Gas Price Jump, Still a Small Spend2026-05-29

-

Market Analysis ‘Sell in May’ Looks to Be Going Astray. Again.2026-05-29

-

Expert Commentary This Week in Review | Consumer Confidence, Iran Developments, Bond Yields

2026-05-29

2026-05-29 -

Market Analysis What AI Tech Stocks Are Signaling About This Bull

2026-05-28

2026-05-28

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today