Personal Wealth Management / Economics

Let’s Do the Twist (and QE3)

The Fed announced QE3 and the continuation of Operation Twist Thursday, but what does it mean moving forward?

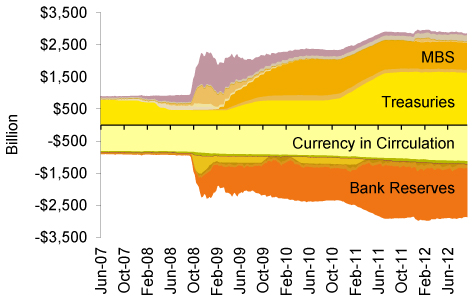

As was generally expected, the Fed announced Thursday it would buy up to $340 billion of agency mortgage-backed securities (MBS) through year end—embarking on a third round of quantitative easing (i.e., the so-called QE3). The aim? To “put downward pressure on longer-term interest rates, support mortgage markets, and help make broader financial conditions more accommodative.” Fed Chairman Ben Bernanke also noted the Fed would continue Operation Twist and reinvest principal of expiring securities back into new MBS purchases. Overall, the moves likely result in the Fed balance sheet’s growing to over $3 trillion for the first time, of which nearly $1 trillion will be in MBS debt. (See Exhibit 1.)

Exhibit 1: Federal Reserve Balance Sheet

Source: Federal Reserve, as of 9/12/2012.

While the announcement was cheered by markets (QE3! QE3!), the longer-term economic effects of QE3 are difficult to determine. First and foremost, interest rates are already historically low: Thirty-year mortgage rates are well under 4%, AAA-rated ten-year debt averages 2.1% and long term junk rates average about 6.6%! It’s unclear to us rates need much pushing down. (Maybe the view is different from the FOMC.)

Still, to us, it’s likely QE3 has as much impact in the coming months as QE2 did—that is, not much. Because the Fed continues to pay 0.25% on banks’ excess reserves, most money pumped into the economy the last two QE rounds has been parked back at the Fed. Free money for the banks! And ahead of increased capital reserve requirements (like Basel III) and the potential for additional burdens when myriad Dodd-Frank rules are finalized, it’s no wonder banks prefer to park their cash back at the Fed.

So why do something the Fed likely already knows isn’t necessary? Well QE3 doesn’t do much, but it also likely doesn’t do much harm either. QE2 hasn’t had much economic impact—at least, not yet—but there was arguably a sentiment boost. Which is a perfectly fine aim. And, very possibly, Bernanke’s posturing for a reappointment in 2013 should Obama win. But either way, heck, maybe mortgages get even cheaper this year—which would be quite remarkable.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today