Personal Wealth Management / Market Analysis

Low Volatility, High Pain

Low-volatility investments are just one more way to chase heat.

Editor's Note: MarketMinder does NOT recommend individual securities; funds referenced herein are merely cited as examples of a broader theme we wish to highlight.

If you want growth with less volatility but need equity-like returns, a "low-volatility" exchange-traded fund (ETF) probably sounds great. By tracking indexes that include the least volatile stocks around, these funds aim to follow markets' general direction, with less swinging. Recently, however, some have swung more than regular-volatility broad markets, surprising many who bought the promise of stable equity-like returns. To us, this highlights an important fact: Low-volatility equity funds' premise is and always was too good to be true.

These funds largely grew out of a mid/late 20th-century obsession with "factor-based" performance models. Back in the early 1970s, some studies found stocks with less price variation performed better than those with more. Even if the data are correct,[i] you must still determine which stocks will be less volatile-volatility might have correlated with concurrent performance, but it isn't predictive. Earlier this year, low-volatility ETFs attracted billions of dollars while "trouncing the market." Recently, however, those same funds plunged, while gyrating more than broad indexes. Thus proving: There is no such thing as an inherently low-volatility stock.

Stocks are stocks, period. Measures of volatility (e.g., standard deviation and beta, which measure how much a stock/category moves relative to the market) are temporary observations. A stock or fund cannot "have lower beta." It can only "have a low beta over the specific time period measured." Any stock can be "low volatility" ... until it isn't. Some sectors are less economically sensitive (think: Utilities, Telecom, Consumer Staples) and widely considered "defensive" but they aren't immune to declines. They merely have different drivers, headwinds and tailwinds than other sectors, so they often lead or lag at different times.

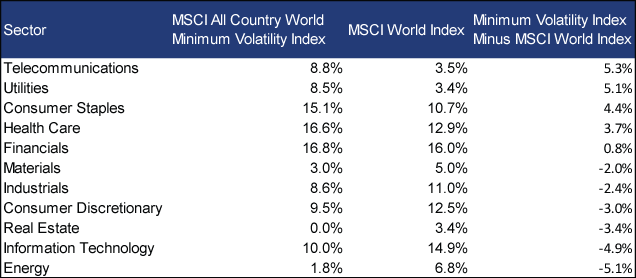

Sector concentration is one problem with low-volatility funds. These ETFs track niche indexes that favor certain sectors over others. For example, the iShares Edge MSCI Minimum Volatility Global ETF mirrors the MSCI All Country World Minimum Volatility Index, which rebalances biannually, using rules to select stocks with "minimum variance" and "lowest possible risk."[ii] In the process, it overweights Utilities and Telecommunications while underweighting IT, Energy, Real Estate and Materials.

Exhibit 1: Minimum Volatility Index Sector Weightings vs MSCI World Index

Sources: MSCI World Minimum Volatility Index and MSCI World Index, both by Morgan Stanley Capital International. Sector weightings as of 10/25/2016

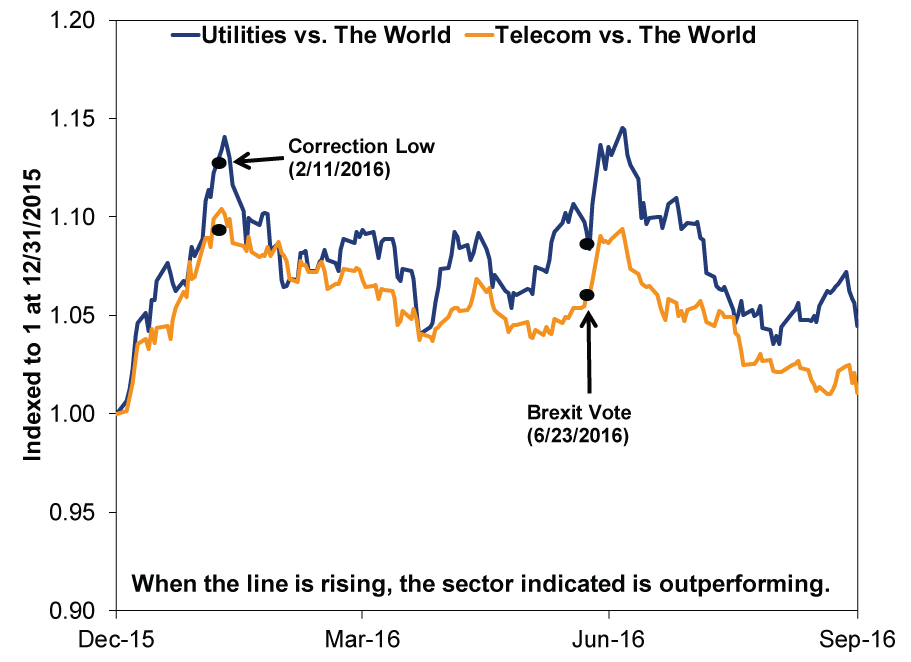

When Utilities and Telecom do well, so do any indexes that favor them. Since these sectors held up nicely during the early-2016 downdraft, they figured prominently in low-volatility funds. But their outperformance this year is concentrated in a couple narrow periods-around the early-2016 downdraft and in the Brexit referendum's immediate aftermath. Most recently, they've underperformed.

Exhibit 2: Utilities' and Telecom's Narrow Outperformance

Source: Factset, as of 10/11/2016

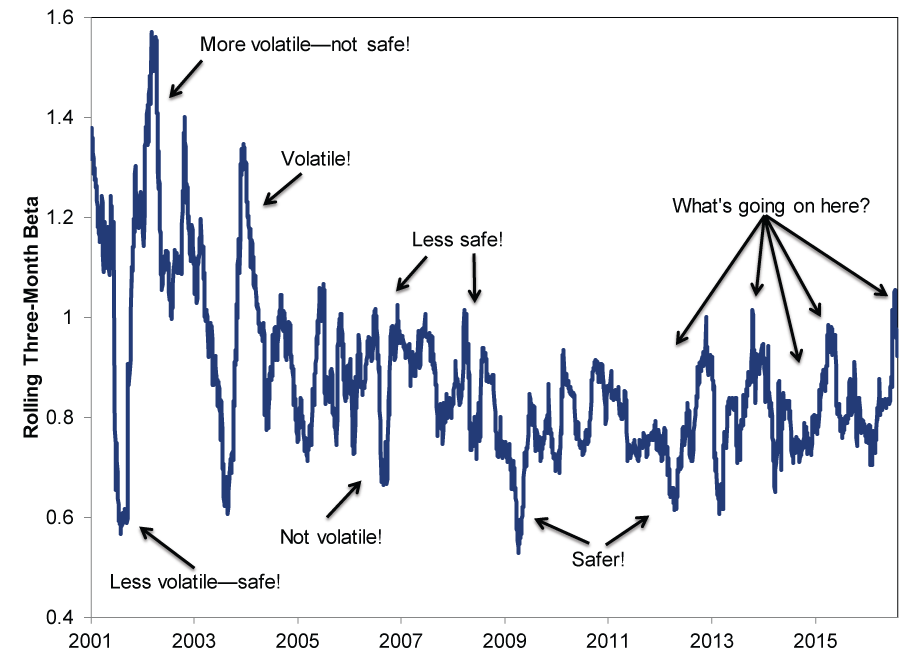

Also, these sectors aren't materially calmer than markets overall. From 2001 to now, Telecom's beta is 0.88. But it swung wildly at times, foiling investors' expectations for existing relationships to hold true.

Exhibit 3: MSCI World Telecom Rolling 3-Month Beta

Source: FactSet, as of 10/27/2016. MSCI World Telecom sector rolling three-month beta, 3/30/2001 - 10/26/2016.

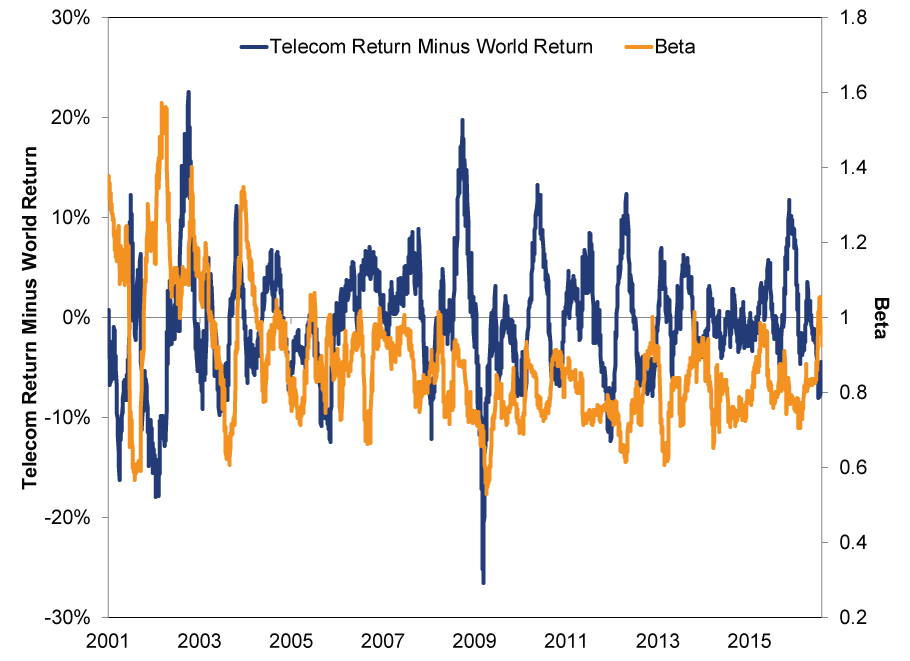

Moreover, Telecom's periods of lower beta (volatility) often aren't coupled with outperformance. Exhibit 4 shows Telecom's three-month rolling relative returns and three-month rolling beta. As you can see, they're all over the map. Since 2001, Telecom has slightly lagged in periods when it sported an above-market beta (greater than 1.0) and in periods when below 1.0. Zoom out and you'll see this too: Telecom's beta is below the market since 2001, but its cumulative return trails the global stocks by more than 50 percentage points.[iii]

Exhibit 4: Less Beta Doesn't Mean More Return

Source: FactSet, MSCI World Telecom sector three-month rolling return minus MSCI World rolling three-month return, both with net dividends. MSCI World Telecom sector rolling three-month beta 3/30/2001 - 10/26/2016.

Always know what you're buying. Prospectuses claim these ETFs use "a 'passive' or indexing approach" and the underlying index eschews "discretionary factors." But there is nothing passive about the index construction. Each May and November, the MSCI Minimum Volatility Index "rebalances" using its "rules-based" methods,[iv] adding firms whose price histories fit the model and removing those that don't anymore.[v] In other words, it buys stocks that were less volatile but don't necessarily stay that way. Past price movement never predicts.

If you want less volatility, you must select an asset with less expected short-term movement than stocks. Most of what investors seek from low-volatility ETFs, they can probably get with a blended stock/bond portfolio. It might not be sexy today, with yields near generational lows, but in our view it is a wiser long-term move than piling into some gimmicky, narrow stock-based thing. Moreover, don't let volatility alone drive your decision making. Consider your comfort with volatility, but ensure your goals and time horizon come first. Otherwise, you might underestimate the amount of volatility necessary to reach your goals.

[i] We lack the space to critique them here, but most of the literature builds off the Capital Asset Pricing Model, which uses flawed inputs, and all make the same basic error of presuming past performance predicts future returns. No correlation without causation!

[ii] Now, mind you, this is misperceived. Risk and volatility are not synonymous.

[iii] Source: FactSet, as of 10/27/2016. MSCI World and MSCI World Telecom sector beta and net returns, 12/31/2000 - 10/26/2016.

[iv] Other low-volatility indexes may rebalance at different times of the year, more or less often, and at the discretion of a manager who doesn't rely on mathematical rules to pick the least volatile stocks. The logic still holds though.

[v] The ETF's prospectus notes that in mirroring the index, turnover was "22% of the average value of its portfolio" in the last fiscal year. So around a fifth of its holdings were sold during the year, as new stocks met (or didn't meet) the index's specifications.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today