Personal Wealth Management / Market Analysis

Low Yields Do Not Equal Low Returns

Even with bond yields near historic lows, investors needn't flock to exotic alternatives to find a decent return.

"In today's low-yield, slow-growth environment, it's impossible for investors to get a decent rate of return with traditional assets like stocks and bonds. You need something like ____________ to boost your returns."

We've seen this argument-cum-sales pitch hundreds of times in the past few years, as Wall Street has cooked up all manner of "alternative" investments to fit that blank. Non-traded REITs. Non-traded MLPs. Business development companies. Non-traded business development companies. Private placements. "Unconstrained" bond funds. Leveraged loan ETFs. "Smart beta" funds. "Liquid alternative" funds. Gold. Silver. Water. Promissory notes and insurance products. And many more. All prey on investors' fears and misunderstandings about yield, return and more in order to lure them to niche markets, often with high fees, limited liquidity and excess risk. One study that caught our eye today claimed that while it was possible to get a long-term 7.5% annualized return with cash and bonds in 1995, to get that expected return from here, you'll need 25% of your assets in private equity and real estate (along with 12% in bonds and 63% in stocks). In other words, to get the same expected return, you'd need to take a heck of a lot more risk.

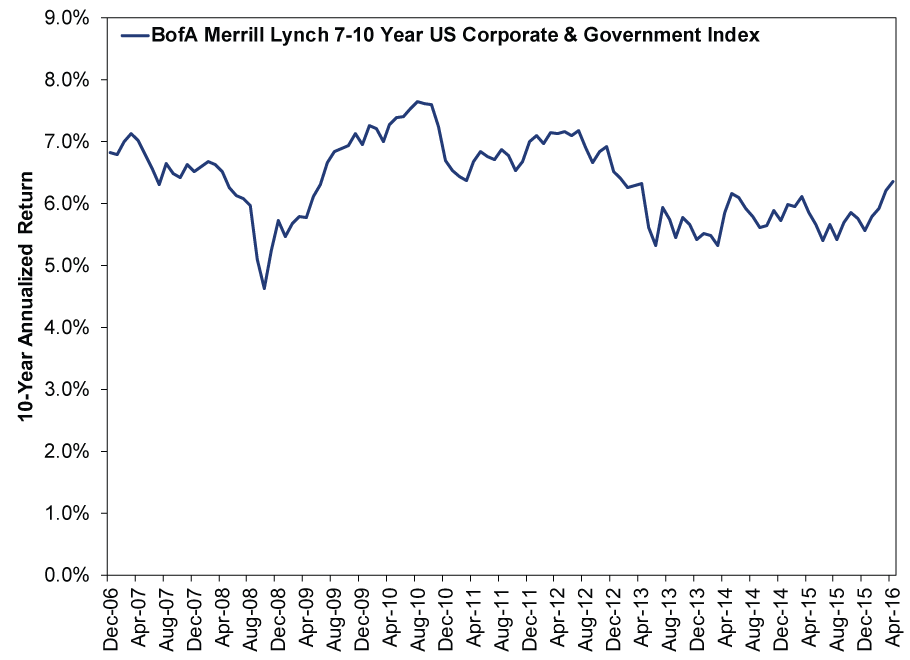

Public service announcement: This is false. Most of the "you have to get creative" literature distorts bond returns, focusing on yields only. But yields are only one component of bonds' total returns. Price movement matters, too, and bonds' total returns have been much better than most give them credit for. Exhibit 1 shows bonds' rolling 10-year annualized returns since 2006. As you'll see, they have not cratered.

Exhibit 1: Fixed Income Is Doing Better Than You Think

Source: FactSet, as of 5/31/2016. BofA Merrill Lynch 7-10 Year US Corporate & Government Index, 10-year annualized return, December 2006 - April 2016.

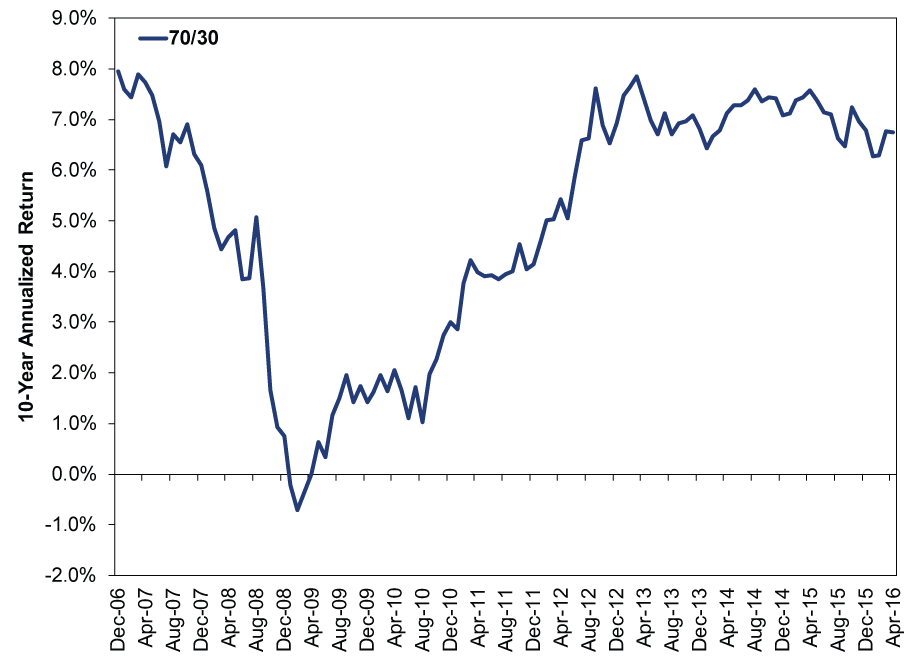

Stock returns are more variable, of course, and returns in blended portfolios (70% stocks/30% bonds and the like) did take a hit during the global financial crisis and its aftermath. But as Exhibit 2 shows, 10-year annualized returns were back near pre-crisis levels by late 2012-and remain there today, even though that rolling 10-year window still includes the crisis. Despite the occasional bear market (even a huge one like 2008), stocks can generate the returns most folks need to reach their goals. That's true of a blended portfolio as well, for those with higher cash flow needs or who prefer less expected short-term volatility.

Exhibit 2: So Are Blended Stock/Bond Portfolios

Source: FactSet, as of 5/31/2016. BofA Merrill Lynch 7-10 Year US Corporate & Government Index and S&P 500 Total Return Index, 10-year annualized returns, December 2006 - April 2016.

The "you need to get creative in this day and age" narrative often makes a convincing sales pitch, but it is a dangerous myth. It steers folks away from something simple and understandable that matches their goals and needs-and toward something that is unnecessarily complicated, potentially out of whack with their needs, costly and often not nearly as good as advertised (we're looking at you, non-traded REITs and MLPs). If you encounter that sales pitch, ask questions and dig deep. Any credible pitch will admit that bonds' total returns remain quite fine to this point, thankyouverymuch, and won't use incomplete information to play on your fears.

Now then, perhaps over the next 10 years bond returns will be lower, even much lower, than recent history shows. But that is a forecast not a fact, and it is a long-range forecast subject to error. It is hard enough to forecast the gyrations of yields and markets over the next 12-18 months. The idea one can foresee interest rates and price movements in May 2026 today is a fallacy of the highest order-and something you should outright discard.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Insights Ken Fisher on Crypto, Inflation, Annuities and More - June 20262026-06-30

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today