Personal Wealth Management / Economics

Lower for Longer

A broader look at the affordability of US debt shows a crisis isn’t likely any time soon.

When other fears fade, it seems US debt concerns often rise anew, particularly in our currently debt-phobic, skeptical world. After all, the recent Fiscal Charade—err, we mean “Cliff”—was at root a debate between two parties that each presume our debt is hugely problematic and must be reduced. They merely disagreed (and will disagree) on the means. In addition, it seems we have another showing of the US debt ceiling’s political theatre underway now.

But all these are just derivatives of fear of the debt itself. Headlines shriek of deals that solve nothing, assure eventual insolvency, burden our children or represent quick roads to become Grecian. However, when you take a broader look at the US’s debt, it’s hard to reach the conclusion we have much of a crisis.

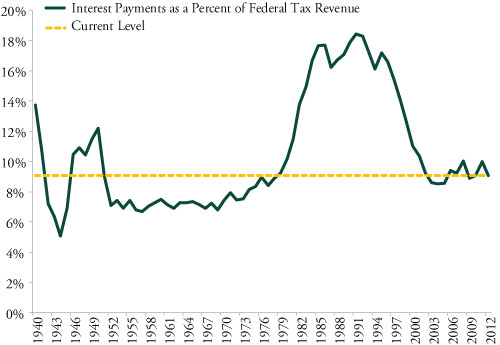

Exhibit 1 cuts right to the heart of the matter, showing net debt interest payments’ share of US federal tax revenue. Currently, that level is roughly 9%—a level easily met in the past and lower than the entirety of the 1980s and 1990s.

Exhibit 1: US Net Debt Interest Payments as a Percent of Federal Tax Revenue

Source: Federal Reserve Bank of St. Louis, accessed on 1/8/2013.

Several major factors combine to determine the affordability of our debt. For example, Exhibit 1 comprises three major data points: tax revenues (determined by economic activity and tax policy), government spending (current and past) and interest rates on the debt.

One key factor in our currently easily affordable interest payment load is multi-generational low interest rates exist across the entirety of the Treasury curve. Which might beg the question: What might happen if they rise? The answer is: in the near term, probably not much. Here’s why.

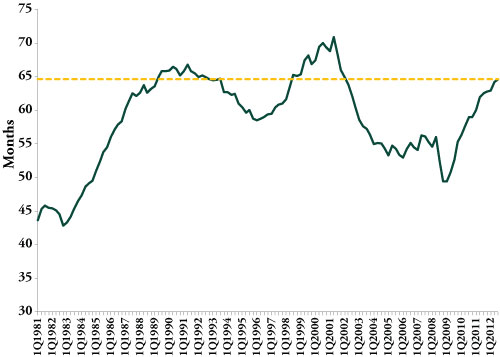

With rates so low, the Treasury has embarked on a strategy pushing the maturities of Treasurys longer. (See Exhibit 2.)

Exhibit 2: Weighted Average Maturity of US Debt

Source: Bloomberg, LP, as of 1/8/2013.

The weighted average maturity across all US Treasury debt is now 64.6 months—over five years—essentially meaning it would take years for the full effect of rate changes to be felt. It also means Treasurys still haven’t experienced the full impact of recent years’ declining rates. Consider, today’s roughly 2% 10-year Treasury rates are fully 200 basis points lower than a decade ago—so a maturing bond today is refinanced at rates roughly half as high. Similarly, five-year Treasury rates—near the average maturity of US Treasury debt—were at 1.18% at the end of 2012, also about 200 basis points lower than five years earlier.i And this is nothing new—we’ve been refinancing bonds at lower rates for many years.

And it would take quite an upward move in interest rates for that to change soon. Currently, five- and 10-year bond rates would have to more than double for Treasury refinancing to result in higher per-bond interest costs. And it’s important to note that even if Treasurys were refinancing at higher levels, that wouldn’t necessarily cause an affordability pinch.

As we mentioned, other factors could change, impacting the affordability of our debt. But when you consider the totality of the situation, there’s just next to no sign our debt is anything resembling a timely problem.

iSource: Federal Reserve Bank of St. Louis, as of 01/11/2013.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why Gas Prices’ Big March Swing Barely Registered at Other Retailers2026-04-21

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—April 13 - April 172026-04-20

-

Market Analysis Easing Hormuz’s Grip for the Long Term2026-04-20

-

Macro Insights Q1 2026 Executive Summary2026-04-20

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today