Personal Wealth Management / Behavioral Finance

MarketMinder’s 2015 Not-Exactly-Annual Portfolio Guide

Here is our not-exactly-annual guide to thinking about your portfolio as the Earth embarks on another trip around the sun.

Jot these down and keep them handy! Or you can just print this article. Up to you. Photo by Comstock/Getty Images.

Only nine days remain before 2014 ends, and the annual traditions of popping champagne, watching a giant glass orb slowly descend in Times Square and singing Auld Lang Syne loom. In investing, the end of the year isn't all that significant fundamentally-stocks do not change cycles based on the calendar. However, one tradition personal finance publications adhere to is the annual "Review Your Portfolio" article, usually trotted out in December or early January. These are not devoid of positive pieces, of course, but most of them follow a pretty basic recipe that includes: Prepare for volatility; save more/cut down on unnecessary expenses; think really hard about your risk tolerance.[i] Others point out behavioral errors but provide you little insight as to how to avoid them. More discerning readers and investors deserve better. Since studies have shown regular MarketMinder readers are 56.2% more discerning than the reader of average media[ii], here is a more actionable review-your-investments article.

The place to begin is with your goals-the bedrock of any investing strategy. You simply cannot know the best mix of assets to employ if you don't know where you're going. Perhaps that seems obvious. But too often, investors get distracted. Some place too much emphasis on avoiding volatility, which can ironically mean you take much more risk of not earning enough return to reach your goals. Others get greedy and seek a quick road to riches. They discard discipline and goals, instead looking for tactical or product-based short cuts with big upside and no downside. Here is a reality to accept in 2015: Every investment has risk, and every investment has return. The key question for you is whether the balance of risk and return targets your goals. And, are you willing to accept that balance? If not, you must reassess your goals.

The standard "Save More!" or "Cut Unnecessary Expenses" is fairly good advice, but you don't need to come to our website to find it. What's more, a retirement devoid of unnecessary expenses doesn't seem too attractive to us. You could save $74.88 not buying your grandkid the Lego Arctic Base Camp set. But is it worth it? Anyway, we'd suggest whether you are retired or still working, having a very good understanding of your current income and expenses is crucial.

Spend most of your time on expenses. Think of them in categories: Fixed and variable; fun and must-haves. This is not just a boring budgeting exercise. This is preparation for volatility. After all, if a bear market hits and you are taking cash flow from your portfolio, you may want or need to reduce the amount. That may seem harsh, but the better prepared you are for that today, the better off you'll be if and when that harsh reality comes true. Use an average (12-month, preferably) of variable expenses like heating and electricity bills. Oh! And this is critical: Make sure you confirm with your spouse or significant other if what you think is discretionary is so discretionary to them. Simply put, if you have to cut back, getting buy-in early is key.

Diversify! That's another common piece of advice these sorts of articles provide. And we agree! Here are some tools to actually help you do it.

- Go global.

The US has outperformed foreign markets in this cycle, but that doesn't mean you should avoid foreign stocks. That's heat chasing, which is no-no time in investing, because the only permanent truth is there is no permanently superior category of stock. Leadership rotates! Today, the US amounts to just over half of the developed world's markets. Global investing provides many more opportunities to diversify. And diversifying globally can mitigate specific-country risks like political risks.

If you are investing in foreign stocks, you should also know that many countries are very top-heavy in certain large stocks and sectors. More than half of Israel's market capitalization is in one health care firm, Teva Pharmaceuticals. Similarly, Statoil is 17% of Norwegian market capitalization. [iii]

- Avoid sector concentration.

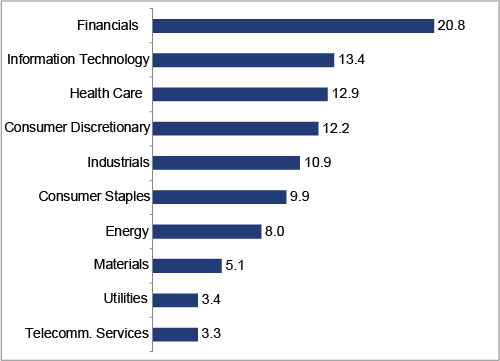

There are 10 sectors in the stock market, as defined by Global Industry Classification Standards (GICS). The 10 are:

- Financials

- Information Technology

- Health Care

- Consumer Discretionary

- Industrials

- Consumer Staples

- Energy

- Materials

- Utilities

- Telecommunication Services

Exhibit 1 shows the current breakdown of the global stock market by sector. Comparing this to your portfolio may reveal areas where you are too concentrated. Why does this matter? Too many investors didn't practice this basic check and balance in 2000, massively loading up on Technology and dot-com stocks instead. The market taught them a harsh lesson. Use this tool to avoid a repeat. You can find this breakdown for yourself here on page two.

Exhibit 1: MSCI World Index Sector Weights, as of 12/22/2014

Source: FactSet.

If you're unsure which sector a stock is in, Morningstar (https://www.morningstar.com/) uses GICS. If you punch the ticker in get a stock quote, the sector is listed under the subheading "Company Information" and is intuitively labeled, "Sector."

- The Five Percent Rule

The Five Percent Rule states that no single company holding should exceed about 5% of your total portfolio value (across all of your investments). This is expressly designed so company-specific issues don't blow up your portfolio. Now, if you are a senior executive of a public company, we get that this may not be doable. But in pretty much every other case, you shouldn't concentrate in a few stocks. Too much risk!

Note: This doesn't apply to ETFs or other internally diversified holdings. Here, the thinking is different. If you own too many stocks, you can really jack up costs and water down returns. That's particularly true if you invest using funds-if you own 10 funds, you may have more than a thousand stocks. You may even own the same stocks in more than one fund, which is pretty inefficient. And it makes it hard to know if you're too overweight to a sector or country.

Maybe this all seems like a lot of work to you. You're right! It is! But if you follow these steps, we believe you'll be a better investor for it-one less subject to the risk of behavioral errors. But this is also your retirement nest-egg we're talking about. You put a lot of work into saving the principal, now the challenge is to care for it properly.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] This year, we are betting you'll get more of the first and last, considering we're already seeing them in articles discussing the mid-December dip.

[ii] This is a joke. There are no such studies. We do, however, generally believe you are more discerning and more intelligent than most readers. Better looking, too! But that's a different article altogether.

[iii]Source: FactSet, as of 12/19/2014. Teva was 54.4% of the MSCI Israel Investible Market Index (IMI), a gauge covering about 99% of Israeli market capitalization. Statoil was 17.0% of the MSCI Norway IMI.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today