Personal Wealth Management / Market Analysis

May 2013 Japanese Trade Update

An increase in Japanese export values doesn’t mean Japan’s quantitative easing program (QE) is working.

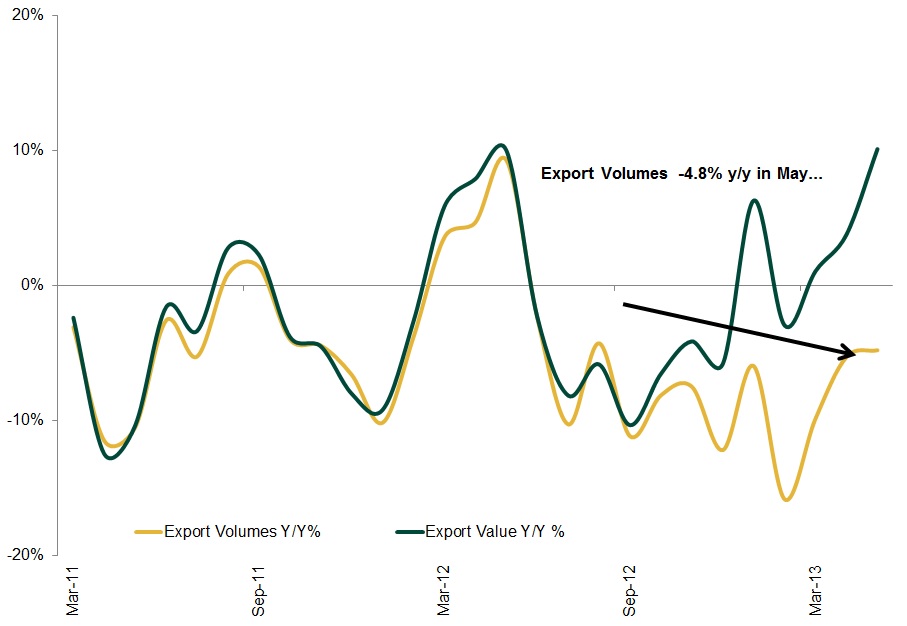

Japanese exports beat expectations in May (+10.1%y/y versus 6.5%y/y), thanks largely to the weak yen—a byproduct of Abenomics’ second arrow, monetary stimulus. However, evidence still suggests the weaker yen hasn’t yet been a net benefit or even fostered real improvement in exports. (Click here for my recent comments about the weaker yen’s impact on exports.) Export volume fell again in May—i.e., exporters are earning more, but they’re producing and selling less. (See Exhibit 1.)

Exhibit 1: Exports Improve, Yet Volumes Remain Negative

Source: Ministry of Finance, Japan; Fisher Investments Research.

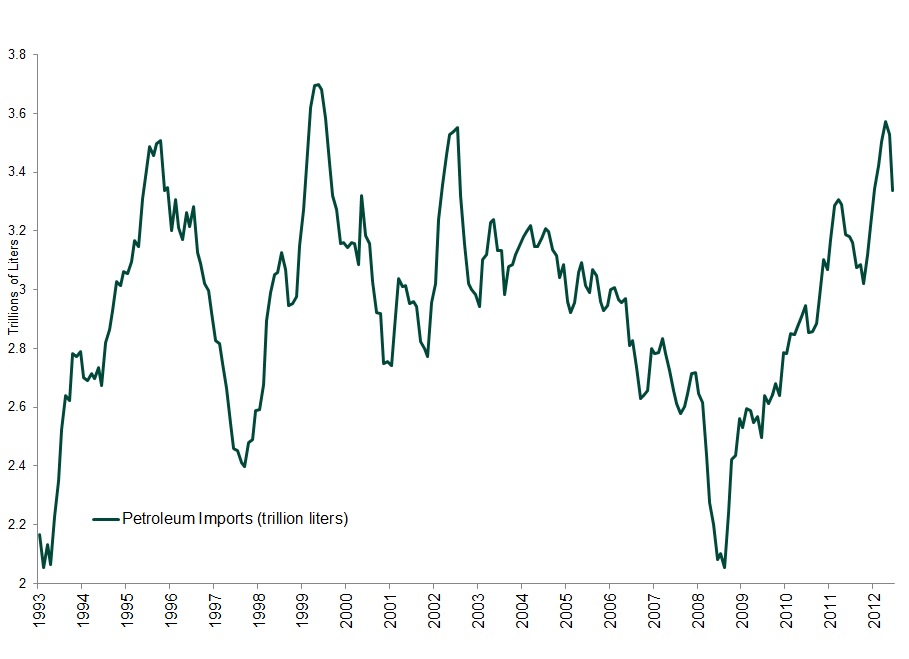

The weaker yen has also created economic headwinds through higher import prices. This puts Japan in a tough spot. For example, because nearly all of Japan’s nuclear reactors remain offline, fuel imports constitute 90% of Japan’s energy, and the weaker yen exacerbates the burden (Exhibit 2), increasing firms’ operating costs. Additionally, few goods are produced start to finish in Japan—many Japanese manufacturers import raw materials and intermediate components. A weaker yen makes these pricier, offsetting much of the cheaper currency’s benefit to the final exported good.

Exhibit 2: Japan’s Rising Fuel Imports

Source: Petroleum Association, Japan; Fisher Investments Research.

Higher export values can provide a nice profit tailwind, but that won’t necessarily translate to higher business investment as policymakers envision. Without rising export volumes, firms likely have excess production capacity, giving them little incentive to expand or purchase new equipment.

Whether this trend lasts remains to be seen. Typically, when a country weakens its currency, export improvement follows higher import prices at a substantial lag, so export volumes could very well rise looking forward. However, even if that happens a weaker yen alone isn’t a panacea for Japan. The nation’s economic issues run much deeper, and Japan needs structural reforms that free up stagnating businesses and remove restrictive barriers. Absent meaningful change, there appears a low likelihood Japan maintains the quick growth seen in Q1.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Investment Implications of Record-Low Consumer Sentiment2026-05-19

-

Market Analysis More Positive Surprise in Japan’s Q1 GDP2026-05-19

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 11 - May 152026-05-18

-

Behavioral Finance Investing Lessons From the Indianapolis Motor Speedway2026-05-18

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today