Personal Wealth Management / Financial Planning

May the 14th of May Spell Mayday for Muni and Corporate Bond Mark-Ups

What you need to know about the SEC’s new rules on corporate and muni bond mark-up disclosure.

Good news for all you corporate and muni bond investors! Beginning on Monday, you will finally know exactly how much you are paying for your bonds … and how much the seller is pocketing.

When you trade a stock, pricing is very straightforward. Your broker charges you the stock’s price plus a small commission—usually a flat fee or a few cents per share. Because these commissions are visible, brokers have big incentives to compete for your business by keeping them low. Hence, over the years, commissions have fallen—from $49 per trade (or more) before the May Day reforms took effect in 1975 to as little as $10 (or less) per trade at many online brokers today. Ah, the benefits of transparency!

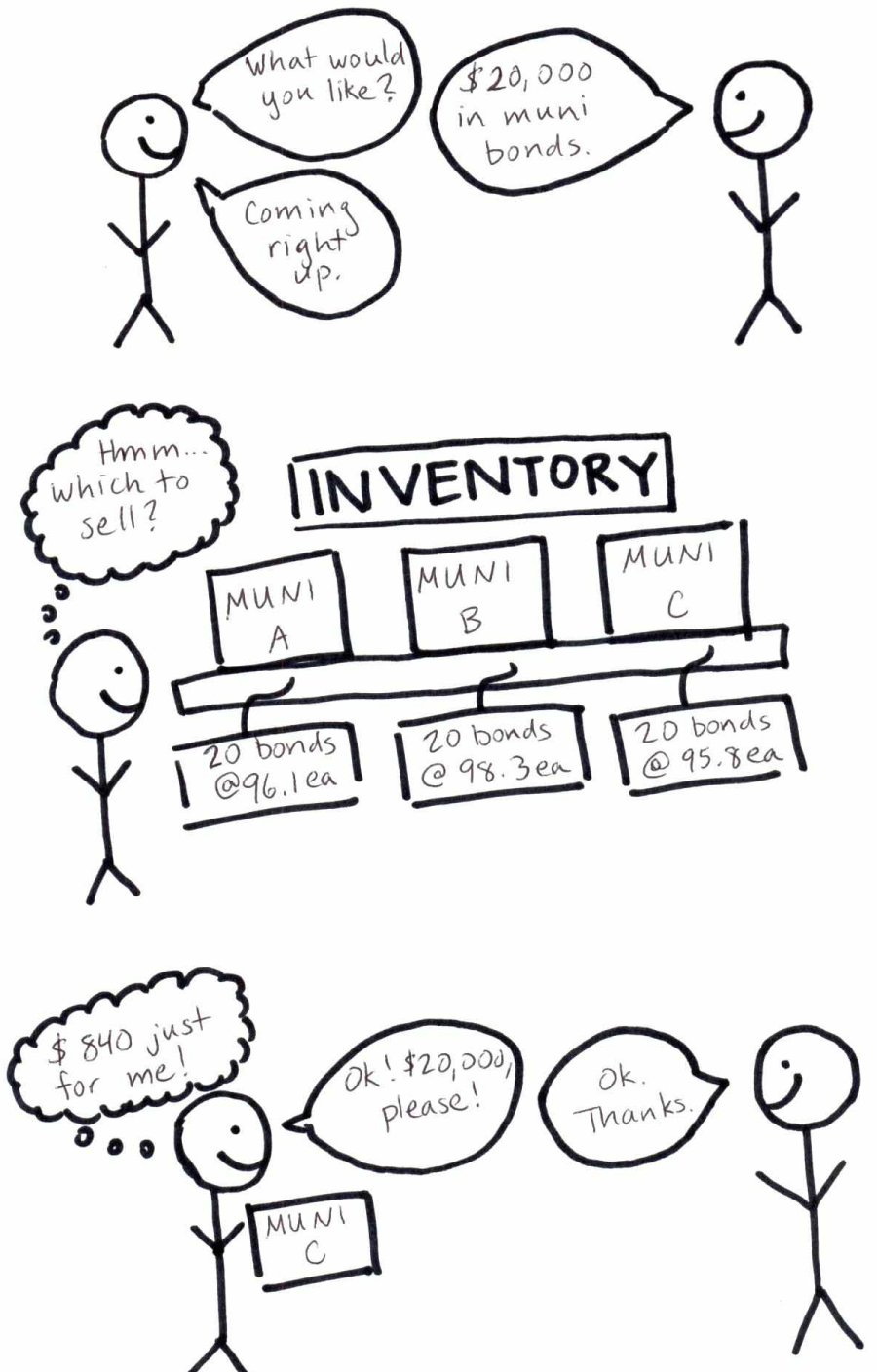

But bond markets have historically been more opaque—especially corporate and muni bond markets. Unlike stocks, bonds don’t trade on open exchanges. They trade over-the-counter, between private parties. Individual issues often don’t trade frequently, making it hard for the individual investor buying or selling the bond to know the actual price in advance. Until now, dealers have been able to further cloud the picture by marking up the bond’s price when they sell it and not telling the buyers how much the markup was. These markups are unlimited beyond regulatory requirements that they be “reasonable.” Over the years, some investigators found markups could be 4% or more of the bond’s price, potentially eating a year’s worth of interest payments. Exhibit 1 is an oversimplified (entirely hypothetical!) stick figure example of how this worked.

Exhibit 1: A Simplistic Picture of Dealer Mark-Up

Source: My nutty brain, math, two pens and Thomas Perez’s scanner.

As the pricing indicates, the three bonds in the inventory cost the dealer 96.1, 98.3 and 95.8 cents on the dollar, respectively. So our stick-person dealer took Muni Bond C, which cost $958 a pop, marked the price up to $1000, and sold 20 of them to our stick-person client. The client gets his bonds, and the broker gets his $840 mark-up and doesn’t have to worry about that month’s car payment.

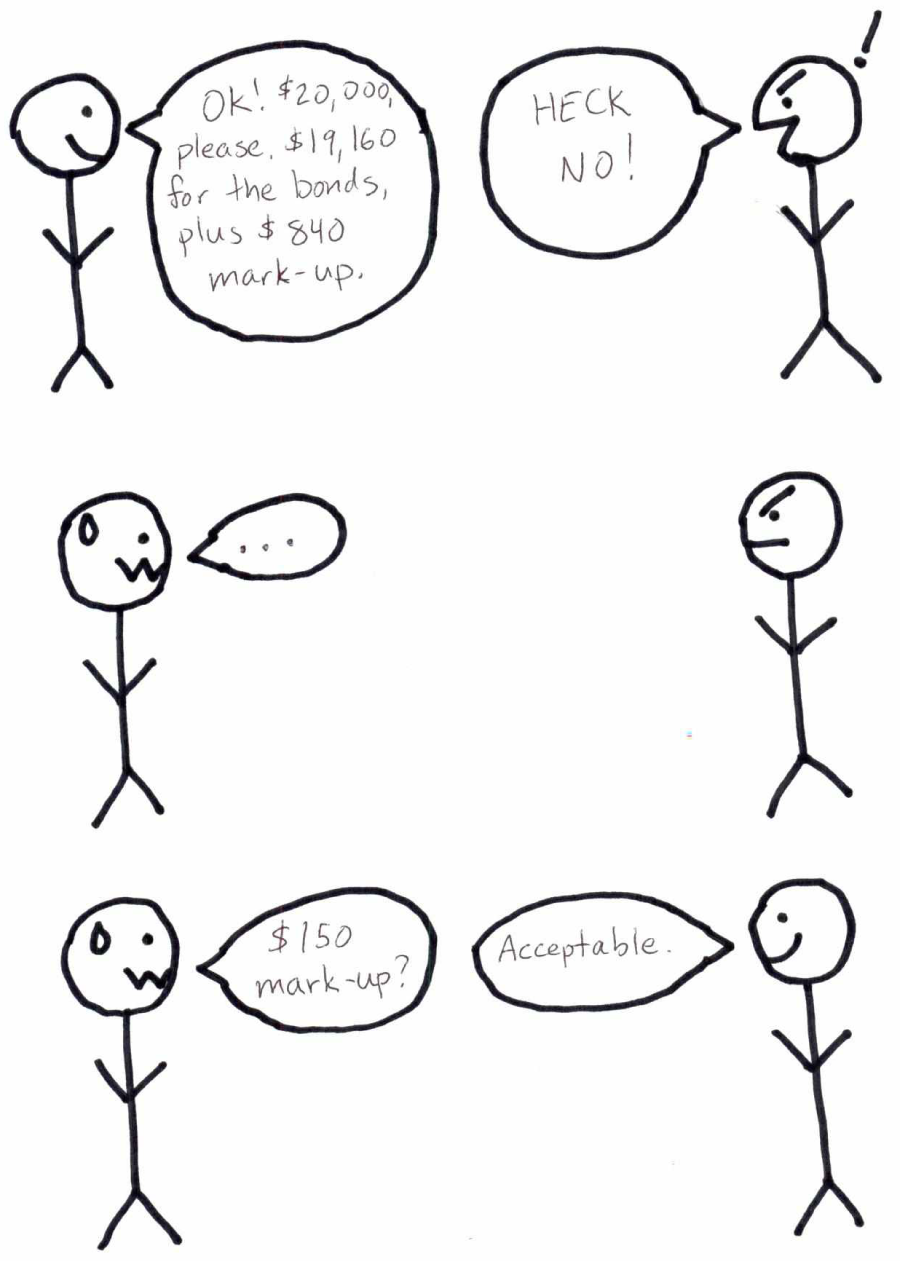

Come Monday, these shenanigans are on the no-fly list. Dealers can still mark up bond prices, but they have to disclose the amount of mark-up on the trade confirmation. So for the first time, clients will know how much they paid for the bond itself and how much they paid the dealer. In mandating this, regulators hope that a dialogue between dealer and client will go something like Exhibit 2 (again this is totally hypothetical, if the stick figures don’t give that away).

Exhibit 2: A Simplistic Picture of Disclosure’s Impact on Bond Pricing

Source: My nutty brain, math, the same two pens and Thomas Perez’s scanner.

Now, whether or not this works as intended remains to be seen. Skeptics worry that because few investors bother looking at trade confirmations, the sun won’t shine as brightly as regulators hope, and investors won’t negotiate mark-ups lower. Additionally, because mark-ups can vary according to bond liquidity as well as from dealer to dealer, some fear even disclosure won’t be enough to jumpstart competition because investors won’t have the information they need to do a proper comparison. It isn’t like the stock brokerage world, where firms can advertise their low, consistent commissions. A bond that trades only a few times a year can be legitimately more expensive to buy due to the greater effort and manpower required compared to a bond that trades regularly. There is no one-size-fits-all model—at least not in the present world.

Some observers think the long-term result might be for investors to gravitate from buying individual muni and corporate bonds to simply owning bond funds and letting the fund managers hash out the mark-up—certainly a possible outcome, and one that might indeed lead to lower costs for individual investors over time. Fund managers trading in bulk probably have more clout, perhaps enabling them to force some competition and goad dealers into reducing mark-up. Or individual investors might prove savvier than skeptics presume, and they drive a bond pricing revolution over time. All these are possible, as well as the new rule turning out to be a dud.

Whatever happens, it probably won’t be overnight. Stock trading commissions did fall immediately after May Day ended fixed commissions, but it took decades for them to reach today’s bargain basement prices. Competition helped, but it needed a boost from technology, which helped reduce brokers’ own operating costs. That enabled them to slash commissions without destroying their profit margins. It wouldn’t shock us if this new bond regime sparked some innovation in muni and corporate bond trading as dealers sought ways to compete without hemorrhaging money and going out of business. But it probably takes time.

In the meantime, though, we think investors should benefit from these changes. More sunlight is always better than less, and informed investors are empowered investors. If you buy a muni or corporate bond and see an astronomical mark-up on the confirmation, you can call the dealer and hold them accountable. Make them explain the rationale. If you don’t think it holds up, you can tell them you’ll take your business elsewhere—and see if they become inclined to cut you a better deal next time. If you are feeling extra-gutsy, you can ask them to quote the mark-up before they execute the trade—and then call around to see if anyone can do better. Sometimes a little grass-roots action is all it takes to spark a change.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today