Personal Wealth Management / Economics

Meanwhile, in Non-Politics …

While the media focuses on everything Trump, the global economy is expanding.

Have you heard the one about how global politics are going topsy turvy, creating massive uncertainty for stocks? So did we. Yet after all the Executive Orders, tweets, polls and scandals, markets finished last week up a smidge, looking past the noise-and, based on all the data that have come out these last couple weeks-at a growing global economy. Yes, while headlines dwelled on sociology, plenty of good economic news flew under the radar, providing a timely reminder that investors shouldn't overemphasize presidential politics as a market driver. Hence, we present a brief tour of recent data you may have missed.

US

Q4 GDP expanded 1.9% annualized, down from Q3's 3.5% and missing expectations for 2.2%. Growth is growth, and Q4 happened to be the second-fastest growth of the year, but the miss caused many to look for clouds in the silver lining. They found it in exports, which fell -4.3%, causing pundits to fear the strong dollar is finally taking a toll. Dig a bit deeper, however, and exports' plunge amounts to a hill of beans ... soybeans, that is. Soybean exports surged in Q3, as poor weather wrecked harvests in South America, artificially inflating Q3 GDP. That normalized in Q4, creating some drag.

Trade, along with inventory change and government spending, is what econ-types might call an "erratic"-peripheral data points subject to interpretation. For example, imports' 8.3% rise subtracted -1.17 percentage points from headline GDP growth.[i] Yet high imports signal healthy domestic demand. GDP math penalizes imports, but they are a key part of total consumer spending and business investment.

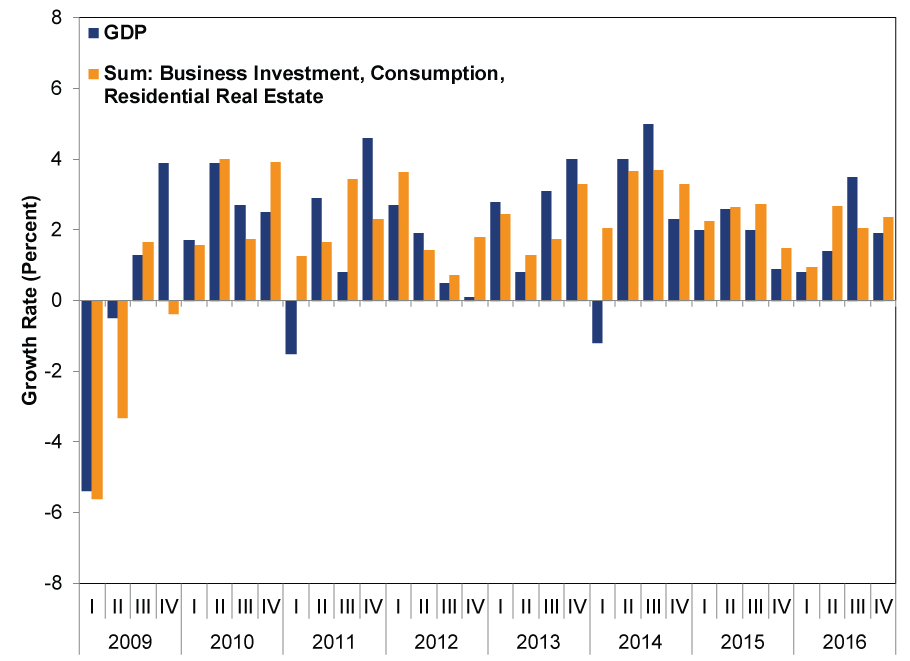

Erratic components are worth considering, but we think tracking pure private-sector GDP components-business investment, consumption and residential real estate-provides a better look at core economic trends. Do that for this expansion, and you see the private sector actually gained steam in Q4.

Exhibit 1: Headline GDP Versus Pure Private-Sector GDP

Source: US Bureau of Economic Analysis, as of 2/6/2017. Q1 2009 - Q4 2016.

The private sector measure traces a smoother path, neither leaping in Q3 nor plummeting in Q4. This is in keeping with the generally modest but positive trend of the last few years.

Energy investment was partly responsible for Q4's private sector pickup, contributing positively for the first time in seven quarters and rising 24.3% annualized.[ii] While this seems massive, it's mainly due to the very low base that resulted from seven straight drops of -30% or worse-the primary headwind against business investment in recent quarters, and largely responsible for its declines in Q1 and Q2. Oil's uptick helped business investment rise 2.4% annualized in Q4, and may remain a modest tailwind moving forward as US shale firms respond to stable or higher oil prices.

January's ISM Purchasing Managers' Indexes (or PMIs) also point positively, suggesting growth continued as 2017 dawned. PMIs survey businesses to see what percentage grew-readings topping 50 indicate a majority did. In January, manufacturing and nonmanufacturing PMIs were above 50, at 56.0 and 56.5, respectively. New orders-which presage future business activity-were even stronger, at 60.4 for manufacturing and 58.6 for non-manufacturing. Even more encouraging, The Conference Board's Leading Economic Index (LEI) rose 0.5% m/m in December-no recession has begun while the LEI is high and rising-bolstered by a steeper yield curve, which encourages further loan growth. All told, continued economic growth should support rising earnings-and stocks-in 2017.

UK

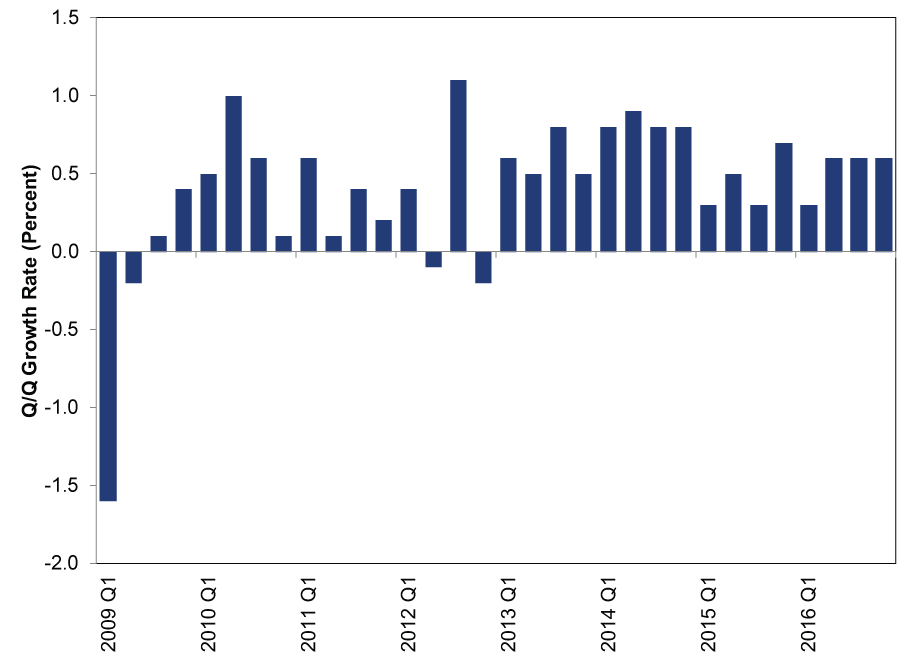

In Q4, Britain grew 0.6% q/q (2.4% annualized), once again belying gloomy pre-Brexit vote forecasts.

Exhibit 2: Brexit Hasn't Fazed UK Growth

Source: Office for National Statistics, as of 2/6/2017. UK quarter-over-quarter GDP growth, Q1 2009 - Q4 2016.

Yet here, too, media coverage managed to find a sad angle: Of the four main output categories (Services, Industry, Agriculture and Construction), only Services contributed positively, renewing fear of an "unbalanced economy" in which manufacturing is a deadweight. For one, this is a bit of a misnomer, as manufacturing output rose 0.7% q/q-it was just canceled out by a 6.9% drop in mining, bringing industrial output's net contribution to zero. Even so, there is nothing unsustainable about service-led growth. Services comprise four-fifths of the UK economy, a natural consequence of economic evolution, and a benefit. Dependence on a single natural resource-say, oil-or factories alone means having a less diversified economy. But under the "Services" catchall is a deep and diverse smorgasbord of retail, entertainment, tourism, finance, health care and much more-a bulwark against trouble in narrow categories, not a danger. If the UK were more "balanced," it would be much more vulnerable to oil's problems or the recent pullback in global trade. Plus, while January's manufacturing PMI did slow from December, it remained well into expansionary territory, as did services.

Exhibit 3: UK PMIs

Source: IHS Markit/CIPS Manufacturing and Services Purchasing Managers Indexes, as of 2/7/2017.

Eurozone

Q4 2016 marked the eurozone's 15th straight expansionary quarter, with 2.0% annualized growth. PMIs-including those of France, Germany, Spain and Italy-remained above 50 in Q4 and January, suggesting eurozone growth is broad-based. (Exhibit 4)

Exhibit4: Eurozone PMIs Also Above 50

Source: Factset, IHS Markit Manufacturing and Services Purchasing Managers Indexes, as of 2/7/2017.

Inflation sped to 1.8% in January, ironically sparking fears hot inflation will squash consumption-even though CPI remains below the ECB's target, and just a couple months ago everyone feared a deflationary spiral. Plus, the rise was mostly a function of Energy prices, which rose 8.1% y/y in January. At any rate, should higher inflation encourage the ECB to taper bond purchases, allowing the yield curve to steepen a bit, lending could perk up further. As in America, political noise hogs headlines, depressing sentiment, but a growing economy provides plenty of support for eurozone stocks.

Asia

Asian countries reporting Q4 GDP thus far have also joined the growth parade.

Exhibit 5: Asia Grows in Q4

Source: Factset, as of 2/6/2017.

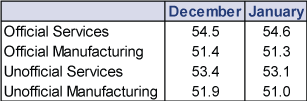

January PMIs suggest 2017 got off to a fine start-even in China, where "hard landing" fears persist. Official PMIs (which cover large, mainly state-owned firms) and Caixin/Markit PMIs (which include smaller, private firms) both topped 50, continuing the recovery that began last year.

Exhibit 6: Chinese PMIs

Source: IHS Markit, China National Statistics Bureau, as of 2/7/2017.

Although these Q4 data aren't forward-looking, they do paint a picture of a growing global economy, something those focused on sociology and beltway bluster don't fully fathom. Markets move on the gap between reality and expectations-when politics weigh on sentiment, positive surprise potential rises, rewarding those who stay disciplined when politics spark emotion.

[i] Mathematically, imports are included in consumer spending and business investment, where they rightly represent domestic demand. But the national accounting superpowers don't think they should be there, so they subtract them later on in the GDP calculation, bringing their net contribution to zero.

[ii] Source: Bureau of Economic Analysis, as of 2/6/2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis New Tax Year, More British Business Tax Fear2026-04-08

-

Market Volatility How Investors Should Think About the Ceasefire2026-04-08

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today