Personal Wealth Management / Market Analysis

Media Still Fret a Growing Global Economy

The dour reaction to July’s PMI data signals the reappearance of skepticism—a reason to be bullish.

As we trudge through the dog days of summer, the heat seems to be making the financial media even grumpier than usual. For all the speculation tariffs and increased protectionism would knock growth, most available data don’t show any major repercussions yet. The latest business surveys out of major economies show businesses, while wary of tariffs, are still expanding overall. Yet headlines harped on the slowdowns hitting manufacturing[i] and services sectors[ii] globally. The dour reaction to solid economic data is further evidence of the disconnect between sentiment and a better-than-appreciated reality—reason to be bullish, in our view.

These growthy economic data are purchasing managers’ indexes (PMI)—monthly surveys measuring business activity. Responding firms confirm whether activity rose or fell that month. PMI readings above 50 mean a majority of those surveyed reported higher activity; under 50 means more saw activity fall. Though PMIs register only growth’s breadth, not magnitude, they are useful snapshots of how businesses are doing. July PMIs of major economies all exceeded 50—a sign firms across manufacturing and services industries are growing overall, which is consistent with other data pointing to a broad global expansion. Yet many media took the glass-half-empty approach.

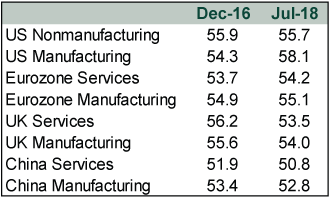

In the US, the Institute for Supply Management’s (ISM) July manufacturing PMI hit 58.1 while its nonmanufacturing PMI was 55.7. Headlines fretted US manufacturers were encountering “roadblocks”[iii] and services industries were losing momentum.[iv] This theme persisted overseas, too. IHS Markit’s eurozone July services PMI recorded 54.2 while its manufacturing PMI registered 55.1. Experts responded with comments about eurozone growth “ebbing”[v] and trade uncertainty hampering manufacturers.[vi] The UK’s IHS Markit/CIPS July services and manufacturing PMIs were 53.5 and 54.0, respectively. Folks worried services—about 80% of UK GDP—were now moving into the “slow lane”[vii] and weakening domestic demand was hurting manufacturing businesses.[viii] Even in China, where the Caixin PMIs for services and manufacturing remained above 50 with July readings of 52.8 and 50.8, respectively, analysts argued the twin issues of the US trade spat and softening domestic demand were hurting growth.[ix]

We aren’t shocked media are so dour, as anxiety over issues like a potential trade war and Brexit remain prevalent today. However, we don’t think the mood aligns with reality. Considering recent history, today’s PMI readings don’t deviate much from the past couple years’. Yet the media’s tone is noticeably different.

The eurozone provides a telling example. In December 2016, the currency bloc’s manufacturing PMI registered 54.9 while services reported 53.7. Media said this was evidence eurozone businesses were on “strong footing.”[x] A month later in January 2017, eurozone manufacturing and services PMIs of 55.2 and 53.7, respectively, prompted one analyst to say, “I certainly continue to be amazed by the skewed negativism towards Europe.”[xi] Compare that to July 2018’s eurozone manufacturing PMI of 55.1, which one article described as “relatively weak.”[xii] Seems to us like that “skewed negativism” is as rampant as ever!

The general optimism about PMIs going into 2017 looked like a global phenomenon, too. Check out this Reuters article[xiii] from January 31, 2017, which gauged the state of the global economy, focusing on the manufacturing sector:

Manufacturers in the United States, the world’s biggest economy, last month increased activity quicker than at any time since late-2014, took on far more workers than was expected and saw heightened demand for their goods. Euro zone factories registered the fastest activity rate for nearly six years, China’s activity expanded for the sixth month and Japanese manufacturing growth was the fastest in almost three years. Even in Britain, where a slump in sterling since the June referendum stoked the sharpest rise in factory costs on record last month, growth remained robust.

A strikingly more optimistic tone—yet are the numbers that different? See for yourself.

Exhibit 1: December 2016 PMIs vs. July 2018 PMIs

Source: FactSet, as of 8/8/2018. US PMIs are from ISM; Eurozone PMIs are from IHS Markit; UK PMIs are from IHS Markit/CIPS; China PMIs are from Caixin.

In several cases, July’s figures were actually better! But you wouldn’t necessarily know that based on the news coverage alone.

In our view, this is telling about the deterioration of broad sentiment recently—which should bode well for stocks. Stocks move most on the gap between sentiment and reality. Today, the persistence of false fears (e.g., tariffs leading to a trade war, a looming inverted yield curve, volatile politics, etc.) is weighing on sentiment. Optimism abounded in late-2016, after stocks’ stellar run that year, but in the wake of early 2018’s correction, skepticism has reappeared.

Many investors wonder if these issues could eventually create a negative that causes a recession. Yet as we have written in recent weeks, these false fears are just that: false. More bricks in the Wall of Worry stocks climb during bull markets. With sentiment still plenty skeptical, reality doesn’t have a high bar to clear to surprise to the upside. We believe this situation exists now. The global economy—as evidenced by recent PMIs—remains in fine shape and looks likely to continue expanding for the foreseeable future. Current tariffs—both implemented and threatened—lack the power to derail the expansion. With the positive drivers underpinning this bull market intact, we believe stocks still have plenty of room to charge higher and expect more bull market for the rest of the year.

[i] Source: “Global factory growth slowing; China-U.S. trade war biting,” Jonathan Cable and Marius Zaharia, Reuters, 7/31/2018. https://www.reuters.com/article/us-global-economy/global-factory-growth-slowing-china-u-s-trade-war-biting-idUSKBN1KM3HG

[ii] Source: “Euro zone business growth slowed in July, optimism fading – PMI,” Staff, Reuters, 8/3/2018. https://www.euronews.com/2018/08/03/euro-zone-business-growth-slowed-in-july-optimism-fading-pmi

[iii] Source: “Manufacturers encounter roadblocks as ISM index declines in July,” by Jeffry Bartash, MarketWatch, 8/1/2018. https://www.marketwatch.com/story/fast-growing-us-manufacturers-runn-into-more-roadblocks-in-july-ism-finds-2018-08-01

[iv] Source: “U.S. Service Industries Lose Momentum,” Josh Mitchell, The Wall Street Journal, 8/3/2018. https://www.wsj.com/articles/u-s-service-industries-lose-momentum-1533305997?mod=searchresults&page=1&pos=1

[v] Source: “UPDATE 1-Ebbing euro zone growth saps business optimism,” Staff, Reuters, 8/3/2018. https://www.reuters.com/article/eurozone-economy-pmi/update-1-ebbing-euro-zone-growth-saps-business-optimism-idUSL5N1UU1UI

[vi] Source: “Euro zone factory growth subdued on trade fears, rising prices: PMI,” Jonathan Cable, Reuters, 8/1/2018. https://www.reuters.com/article/us-eurozone-economy-pmi/euro-zone-factory-growth-subdued-on-trade-fears-rising-prices-pmi-idUSKBN1KM43G?il=0

[vii] Source: “Service sector slows as World Cup and hot weather dent growth,” Helen Chandler-Wilde, The Telegraph, 8/3/2018. https://www.telegraph.co.uk/business/2018/08/03/service-sector-slows-world-cup-hot-weather-dent-growth/

[viii] Source: “UK factory activity at lowest level in 3 months, PMI survey shows,” Gavin Jackson, Financial Times, 8/1/2018. https://www.ft.com/content/4787497a-9566-11e8-b67b-b8205561c3fe

[ix] Source: “China's July manufacturing growth slows on trade dispute, softer domestic demand,” Staff, Reuters, 7/30/2018. https://www.reuters.com/article/us-china-economy-pmi-factory-official/chinas-july-manufacturing-growth-slows-on-trade-dispute-softer-domestic-demand-idUSKBN1KL03T

[x] Source: “Euro zone factories entering 2017 in good shape, PMI shows,” Staff, Reuters, 1/2/2017. https://www.reuters.com/article/us-eurozone-economy-pmi-idUSKBN14M0C7

[xi] Source: “Eurozone economy quietly outshines the US,” Chris Giles, Financial Times, 2/5/2017.

[xii] Source: “Manufacturing growth slows despite strong export demand,” Helen Chandler-Wilde and Anna Isaac, The Telegraph, 8/1/2018. https://www.telegraph.co.uk/business/2018/08/01/manufacturing-pmi-slows-despite-export-demand-growth-ahead-interest/

[xiii] Source: “Momentum and risk: world economy enters 2017 with winds fore and aft,” Jonathan Cable and Nichola Saminather, Reuters, 1/31/2017. https://www.reuters.com/article/us-global-economy/momentum-and-risk-world-economy-enters-2017-with-winds-fore-and-aft-idUSKBN15G3EJ

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today