Personal Wealth Management / Market Analysis

Meet the New German Government, Same as the Old One

A German coalition redux is the latest milestone in the eurozone’s journey of falling political uncertainty.

Last Thursday, more than 24 hours of talks between the leaders of Germany’s center-right Christian Democratic Union (CDU) and the center-left Social Democrat Party (SPD) finally yielded a coalition deal, pending SPD party members’ final approval. While coverage focuses on who got which ministries, party leadership drama and what all this means for further European integration, we believe the main takeaway is markets’ continuing to gain clarity about the German political scene. Although it seems Germany will soon have a government again, it likely remains gridlocked—a positive, in our view. As investors move past election-season jitters and appreciate strong eurozone economic fundamentals, we think the region’s stocks should benefit.

In September’s general election, incumbent Chancellor Angela Merkel’s CDU and Bavarian sister party Christian Social Union (CSU) took 35% of seats in the Bundestag (Germany’s parliament). Success! But there was a hitch: No party had a majority, and the SPD said it wouldn’t re-up its “grand coalition” with the CDU. And no wonder—the SPD endured a shellacking in the 2009 election after four years as the CDU’s junior coalition partner. After sitting in opposition during Merkel’s second term (2009 – 2013), the SPD again allied with the CDU in 2013—and then posted its lowest tally since WWII (22%) in 2017’s elections. Presenting yourself as a viable alternative to the dominant party is hard when you helped govern.

Understandably then, it took lots of wrangling and apparent concessions to convince SPD leaders to try it again—Merkel’s Plan B after her attempts to form a coalition with the Free Democrats and Greens failed. In the meantime, Germany broke a postwar record for length of time without a government. But at last the CDU and SPD have a deal. Under it, the SPD would get 6 of 14 cabinet positions—more than expected—among them the coveted Finance Minister spot. As one wag put it, “This is the first SPD government led by a CDU chancellor.” This probably overstates it, but a relatively evenly split coalition between two parties on the cusp of parting ways just months ago is a recipe for gridlock.

Though neither is radical, the SPD and CDU differ on many issues—and ideologically split coalitions generally accomplish less. In parliamentary systems, parties may tout bold proposals on the campaign trail, but they generally can’t implement them without an outright majority. Cementing a governing coalition usually involves casting big ideas aside in favor of watered-down policies no one loves but all can mostly agree on.

The “grand coalition” should know this: In 2013, the CDU and CSU promised a host of tax breaks and billions in new infrastructure spending, while the SPD platform talked up tax hikes on the rich and tighter banking rules. But the final “coalition contract” between them was less ambitious, focusing on things like pension tweaks and instituting a minimum wage—typical of coalitions’ tendency to focus on a small number of relatively uncontroversial policies. Little major legislation emerged during Merkel’s last term—and since the 2017 coalition agreement also features compromises on former “red lines” like immigration, health care and taxes, we doubt this time will be different.

More of the same should be just fine for markets. In 2013 – 2017, while the CDU/CSU/SPD coalition was busy not doing a whole lot, German stocks rose 25.6%, in line with eurozone stocks’ 25.8% gain.[i] This isn’t as great as returns during Merkel’s more ideologically aligned coalition with the pro-business Free Democrats (September 2009 – September 2013), when German market returns far outstripped the eurozone’s (40.1% versus 15.4%).[ii] But this is probably due in large part to Germany’s escaping the worst of the eurozone debt crisis. In any case, German stocks have seen grand coalitions before and done just fine.

This isn’t surprising when you consider gridlock’s benefits. Deadlocked governments reduce legislative risk—the odds of radical reforms overhauling property rights or creating new winners and losers. The latter typically feel the pain more, dinging sentiment and stocks. Do-nothing governments might annoy voters, but they give markets one less thing to sweat—a positive, even if investors never consciously realize it.

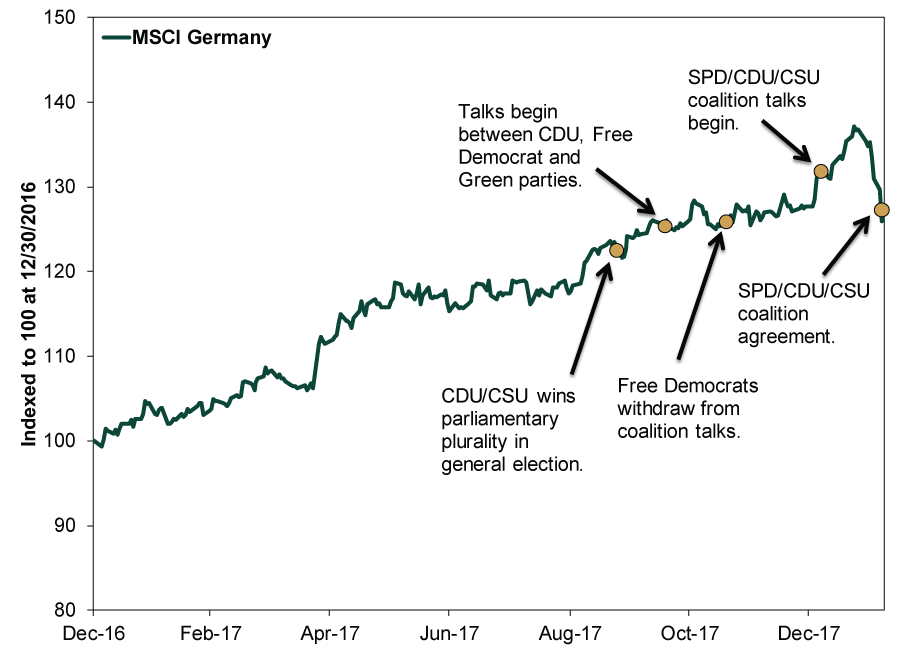

Simply moving closer to resolution—even if it hasn’t arrived yet—is also a positive. As Exhibit 1 shows, German stocks were rising before the coalition deal’s announcement—even well before September’s election. That drop toward the end is part of the global pullback, which wasn’t related to German politics.

Exhibit 1: German Stocks Not Waiting for an All-Clear Signal

Source: FactSet, as of 2/8/2018. MSCI Germany Index returns with net dividends, 12/30/2016 – 2/7/2018. Marked events, in chronological order: here, here, here, here and here.

Markets are efficient. Stocks typically begin digesting probable political realities before votes are counted and coalitions form. By then, markets have likely left behind folks who waited for total clarity. Owning stocks while uncertainty remains—though uncomfortable at times—allows investors to benefit as it fades. We wouldn’t be surprised if this pattern continued for other 2018 elections—including in Italy, the US, Mexico and Brazil. Though recent volatility may obscure it, falling political uncertainty likely provides more fuel for the global bull this year.

[i] Source: FactSet, as of 2/8/2018. MSCI Germany and MSCI EMU Index returns with net dividends, 9/20/2013 – 9/22/2017

[ii] Source: FactSet, as of 2/8/2018. MSCI Germany and MSCI EMU Index returns with net dividends, 9/25/2009 – 9/20/2013

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Big Gas Price Jump, Still a Small Spend2026-05-29

-

Market Analysis ‘Sell in May’ Looks to Be Going Astray. Again.2026-05-29

-

Expert Commentary This Week in Review | Consumer Confidence, Iran Developments, Bond Yields

2026-05-29

2026-05-29 -

Market Analysis What AI Tech Stocks Are Signaling About This Bull

2026-05-28

2026-05-28

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today