Personal Wealth Management / Economics

Misinflation

Do February data indicate inflation will soon be on the rise?

Is inflation about to start inflating again? You might get that impression from recent headlines announcing inflation may have turned a sharp corner and is headed for greater heights. The evidence? US and eurozone prices rose in February. In our view, though, everyone is being a tad hasty-a deeper look at the data shows February's figures are likely a blip rather than the start of a new trend.

In the US, the Consumer Price Index ticked up from January's -0.1% y/y to 0.0%[i], as prices rose 0.2% m/m, the first monthly rise since last October. The eurozone's annual inflation rate decline slowed from January's -0.6% to -0.3%, with prices increasing 0.6% m/m. The UK, however, didn't follow suit-while prices rose 0.5% m/m in February, its annual inflation still dropped from January's 0.3% to 0% due to falling food and energy prices. Pundits cheered overall, welcoming higher prices in the US and Europe and the prospect of "good" deflation in Britain. Some suggested the US report "could give the Fed confidence inflation is slowly heading toward its 2% target." In euroland, many breathed easier, saying fears of prolonged deflation were "eased." In Britain, some welcomed the lowest inflation rate on record by pondering a new term for falling prices during a growing economy.[ii]

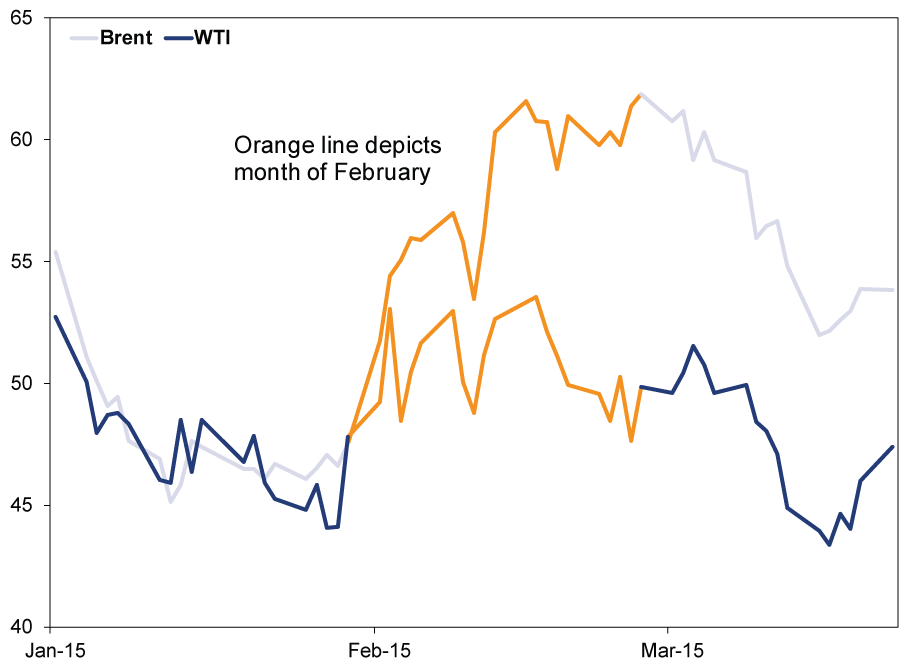

Far be it from us to pooh-pooh optimism, but in our view, this all misses the elephant in the room. February's m/m CPI upticks result from a short-lived jump in oil prices-the same oil prices that drove deflation in prior months. From June 2014 through January 2015, Brent Crude oil prices fell from $111.03 to $47.52.[iii] That pulled down headline monthly CPI from September through January. But in February, Brent prices rose a bit reaching $61.89 by month's end.[iv] So, they naturally boosted February CPI. But they will probably detract from March CPI, considering crude is down 11.4%[v] this month (through 3/23/2015). WTI Crude, the US benchmark, moved similarly.

Exhibit 1: 2015 Brent and West Texas Intermediate Crude Oil Prices in US Dollars

Source: St. Louis Federal Reserve, as of 3/25/2015.

Though this CPI uptick is probably a blip, it underscores an oft-overlooked point about recent deflation: It is probably fleeting.[vi] Not because oil prices will shoot back up! But because higher oil prices will eventually fall out of the year-over-year base comparison-something few beyond BoE governor Mark Carney have noted. Since oil prices have fallen for about half a year, the y/y inflation figures will likely show a downtrend for a few or several months more, depending on where Energy prices go from here. When higher oil falls out of the base comparison, it is a fair assumption we will hear much chatter about prices finally turning the corner-for real this time! And it will all be noise, considering most prices don't have a corner to turn.

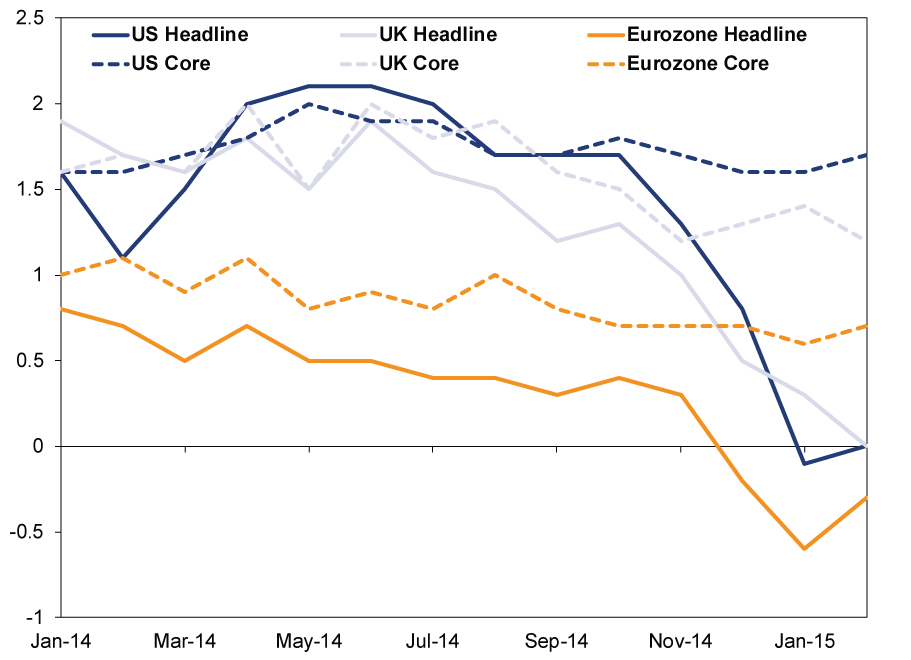

How do we know? Simply-just looking at core inflation, which strips out volatile components like energy and food (supermarket price wars have also pulled down UK CPI). Core prices rose month-over-month in the US, UK and eurozone in February (0.2%, 0.5% and 0.5%, respectively). Annual core inflation rates accelerated in the US (1.7%) and eurozone (0.7%). The UK's core inflation rate decelerated a tad, to 1.2%, but it's in line with longer-term trends. (Exhibit 2).

Exhibit 2: Annual Headline and Core CPI for the US, UK and Eurozone

Source: St. Louis Federal Reserve and the Office for National Statistics, as of 3/25/2015. From January 2014 - February 2015.

Our advice: Don't overthink monthly CPI for the next several months-and don't get swayed by headlines making grand proclamations. Energy aside, the longish-term trend of mildly rising prices persists alongside just-fine growth-the Goldilocks economy remains intact.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[ii] Our horrific suggestions include: Degroflation, grodeflation, expandeflation, groflation, indeflation and happy-happyflation.

[iii] Source: St. Louis Federal Reserve, as of 3/25/2015. Prices from 6/30/2014 and 1/30/2015.

[iv] Ibid., as of 3/25/2015. February high was reached 2/28/2015.

[v] Ibid., as of 3/25/2015.

[vi] Also, it's worth noting deflation is not the economic scourge and growth killer so many folks regularly presume. The Bank for International Settlements recently studied 140 years of history in 38 countries and found no reliable history of deflation being problematic. What's more, deflation spurred by huge output or productivity gains is the aftereffect of a positive, not some negative leading indicator. But all that is an article for another day.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today