Personal Wealth Management /

MLPs and Your Portfolio

As MLPs come further into the spotlight, many investors wonder what exactly they are and what they can do for portfolio returns.

With interest rates on everything from savings accounts to junk bonds at or near generational lows, many income-seeking investors are looking for creative or, to some, exotic means of generating cash flow. Some are turning to a relatively little-known type of security—master limited partnerships (MLPs). MLPs may attract investors for a number of reasons: their high dividend yields and tax incentives, to name a couple. But, like all investments, MLPs have pros and cons, which are crucial to understand if you’re considering investing in them.

MLPs were created in the 1980s by a Congress hoping to generate more interest in energy infrastructure investment. The aim was to create a security with limited partnership-like tax benefits, but publicly traded—bringing more liquidity and fewer restrictions and thus, ideally, more investors. Currently, only select types of companies are allowed to form MLPs—primarily in energy transportation (e.g., oil pipelines and similar energy infrastructure).

To mitigate their tax liability, MLPs distribute 90% of their profits to their investors—or unit holders—through periodic income distributions, much like dividend payments. And, because there is no initial loss of capital to taxes, MLPs can offer relatively high yields, usually around 6-7%. Unit holders receive a tax benefit, too: Much of the dividend payment is treated as a return of capital—how much is determined by the distributable cash flow (DCF) from the MLP’s underlying venture (e.g., the oil pipeline).

DCF is usually higher than the venture’s net income—high depreciation and other non-cash charges are common among MLPs—so investors often receive more distributions than taxable income. These are considered returns on capital and are later subtracted from the initial investment’s cost basis, effectively deferring taxation on the excess income until the partnership is sold.

If you sell an MLP at a price exceeding your original purchase price, the difference between the two is considered a capital gain and taxed accordingly. However, there is an additional caveat to MLPs. Any return of capital in dividend payments reduces the tax basis of the MLP. At sale, the difference between this tax basis and your original purchase price is taxed as ordinary income. If you hold an MLP for a long time, this could be significant.Additionally, MLPs may be inefficient investment vehicles to include in tax-deferred or tax-exempt accounts like IRAs, since the tax benefit is eliminated in these vehicles. Each unit holder is responsible for paying his or her own taxes on MLP gains—consult a tax advisor for more detailed information.

All investments have risks, and MLPs are no exception. Beside tax complications, they’re heavily dependent on debt financing—resulting in highly leveraged balance sheets. So when interest rates are low, investors may be attracted to MLPs’ high cash flow. But rising interest rates can increase MLPs’ debt-servicing costs, leading to reduced earnings (and, therefore, attractiveness) to investors.

Plus, any investment-creating legislation could be revised or revoked at any time. There have even been recent attempts to do so (during the fiscal cliff debate at the end of 2012, for example)—though they haven’t been successful and aren’t likely to be soon, due to extant political gridlock. It is, however, a factor for MLP investors to watch.

Now, this perhaps isn’t the space to address the folly of focusing on high yield when you need income, but it’s crucial to recognize a yield isn’t equivalent to return. It is part of total return. Investments can earn you high yields while not adding—or, worse, detracting—from your total gains. For example, the Alerian MLP Index (comprised of the top 50 MLPs by market capitalization) fell nearly -50% in 2008 including dividends.

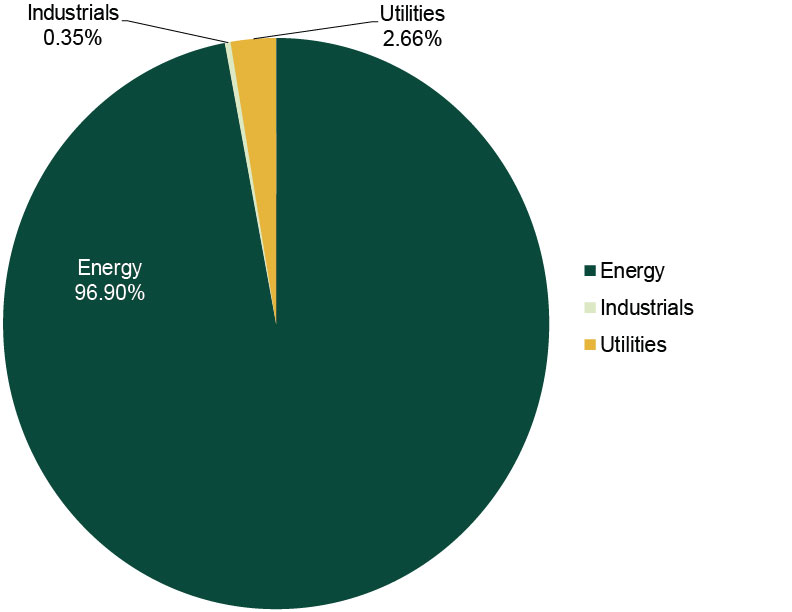

Your outlook for MLPs shouldn’t merely hinge on their dividend yield. Two other factors swamp: Their small market size and lack of diversity. Consider, the Alerian MLP index has a $224 billion adjusted market capitalization. That means the 50 largest MLPs together are outweighed by some of the world’s largest single stocks. The individual MLPs are effectively small cap, so your outlook should account for whether you expect small or large stocks to outperform. Moreover, the Alerian MLP index is nearly exclusively concentrated in the Energy sector. (Exhibit 1) Events positively or negatively impacting that sector’s profitability could materially impact such a concentrated index—affecting distribution yields and prices. For example, lower oil and natural gas prices, a result of the US shale boom, have impacted the profitability of many oil and gas-related projects. This trend appears unlikely to end any time soon. Yet, according to both their 12-month forward and 12-month trailing P/E ratios, MLPs are trading at about twice the MSCI World Energy sector.*

Exhibit 1: Alerian MLP Index Sector Weights

Source: FactSet Data Systems, Inc., as of 11/25/2013.

As bull markets mature, investors usually see a rotation away from small cap into bigger, well-known stocks. And at the end of typical bull markets, the biggest of the big stocks, mega cap, tend to perform best. As this current bull is likely near its halfway point, we’d expect to see that trend materialize moving forward. This factor, in addition to depressed US natural gas prices resulting from the shale boom, argues against a big weight in MLPs in the here and now.

*Source: FactSet Data Systems, Inc. 12-month forward P/E ratio of the Alerian MLP ETF was 2.04 times higher than the MSCI World Energy sector’s, and the 12-month trailing P/E ratio of the Alerian MLP ETF was 1.94 times higher than the the MSCI World Energy sector’s, as of 11/25/2013.

HT: Alex Nelson and Mary Holdener

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

Market Analysis Due Diligence and the DOL’s DOA Fiduciary Rule2026-03-13

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today