Personal Wealth Management / Market Analysis

More 'Broken Windows' in Japan

Potential post-quake fiscal stimulus isn't a reason to get wildly bullish on Japan.

Barely five years after the Great Tohoku Earthquake and tsunami, Earth's tectonic plates have wreaked havoc on Japan again-this time with several strong quakes in Kyushu, centered on Kumamoto Prefecture. The first, a 6.5 temblor, hit last Thursday. A 7.3 quake hit one and a half days later, followed by a series of aftershocks. Ordinarily, the world's reaction would center on the devastating loss of life and property-42 have perished, over 1,000 more are injured and 110,000 are displaced, at last count-much as it did following Ecuador's 7.8 quake last weekend. Our thoughts are with those impacted by these disasters. But in Japan, many headlines almost immediately leapt to speculating about the economic impact. We saw it in 2011 and we see it again now: Many believe the quake will trigger fiscal and monetary stimulus, boosting prospects for Japanese stocks. While it's possible Japanese stocks might get a short, sentiment-driven boost, we'd advise against trying to capitalize on it. The notion of post-disaster stimulus-fueled growth is a fallacy, and Japan's longer-term fundamentals remain quite lackluster.

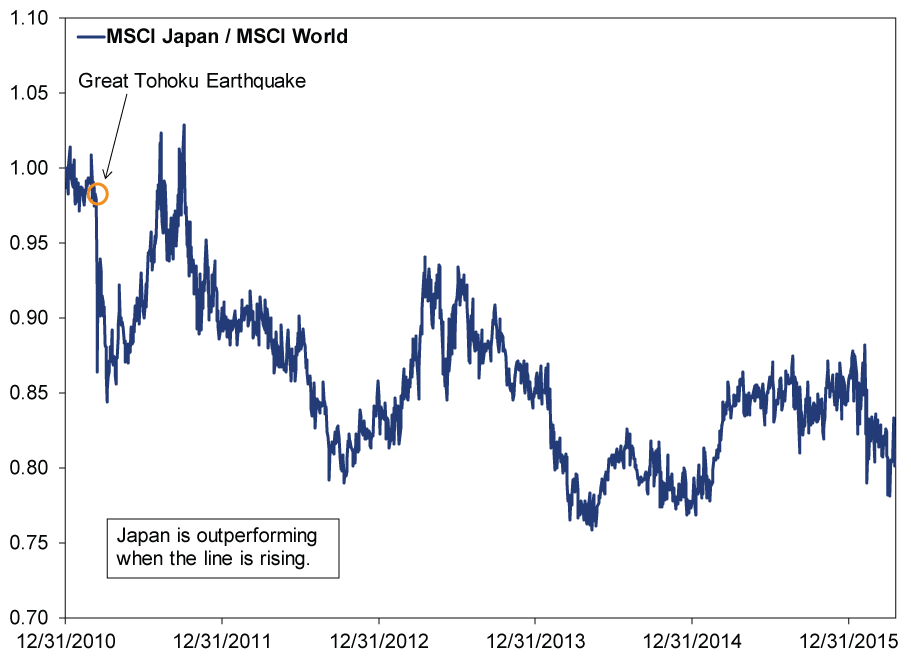

Exhibit 1 shows Japanese stocks' relative performance since the end of 2010. After the Great Tohoku Earthquake and Fukushima Daiichi nuclear disaster, Japanese stocks plunged, trailing the MSCI World Index badly. But in early April Japan stabilized, and the country outperformed handsomely for a few months. The ride was short-lived, however, and by early October Japan was lagging the world again. A couple of sentiment-driven bumps aside, they've lagged, overall and on average, ever since.

Exhibit 1: Japanese Stocks' Relative Performance

Source: FactSet, as of 4/19/2016. MSCI Japan and MSCI World Index returns in USD with net dividends, 12/31/2010 - 4/18/2016. Indexed to 1 on 12/31/2010.

In retrospect, it is perhaps tempting to pin those brief but amazing relative returns on post-quake stimulus, and maybe that had something to do with it, to the extent it boosted sentiment. But "yentervention" to weaken the currency was spotty and had a limited impact. (And the last three years have since proven a weak yen alone doesn't make Japanese GDP skyrocket.) Fiscal stimulus did materialize, but its effects were also temporary and at best questionable (more on this momentarily). Plus, it would be wrong to ignore the rest of the world, which spent much of 2011 mired in a nasty correction as Greece, Portugal, Italy and Spain threatened to collapse the eurozone. Japan has a long and slightly weird history of tending to outperform during sharply negative periods. 2011 was a correction, not a bear, but it isn't unrealistic to suspect Japan benefited from a flight to quality, irrespective of the quake. Today, with the world rebounding nicely from a correction and no bear market in sight, it seems unlikely Japan would benefit from investors' yen[i] for stability from here on.

Then, too, post-disaster stimulus isn't necessarily an economic positive. Whenever disaster strikes, it's fairly common for pundits to offer a silver lining: "Yah, but rebuilding will boost construction, jobs and GDP." In a vacuum, this might appear to be true. But it ignores the counterfactual: Where would that money have gone if the disaster hadn't diverted it to rebuilding?

This is known as the "Broken Windows Fallacy," taking its name from M. Frederic Bastiat's 1850 essay, "That Which Is Seen, and That Which Is Unseen." Part I, "The Broken Window," asked the reader to consider what happened when Jim the shopkeeper's rambunctious son broke a window. When the neighbors stopped by to tut-tut, as neighbors do, one said "ah well, what would the glaziers do if no one ever broke windows?" To him, the six francs it would cost to repair the window were a wonderful windfall, and therefore, the broken window was good. Hooray for the rambunctious kid. Or not: Bastiat then walked the reader through the counterfactual, or that which is unseen-where would those six francs have gone if the kid never broke the window? Maybe Jim would have bought shoes! That makes the glazier's gain the shoemaker's loss and Jim's loss-because rather than have the new kicks and the window, Jim only has a window. Is that really better?

It's a simple example, but it applies to any destructive event. No one in their right mind would ever argue the London Blitz, Hiroshima or Nagasaki were economic positives. Natural disasters aren't any different, economically. Money spent on reconstruction is money not spent elsewhere, in all likelihood more productively. Natural disasters are nature picking economic winners and losers. They shift economic activity, but they don't create it. Society is no wealthier when the reconstruction is done. After the Great Tohoku Earthquake, fiscal stimulus at best offset a post-quake decline in consumer spending. It didn't prevent recession, and it didn't get Japan's economy on a more sustainable long-term track.

Earthquake aside, Japan is in the same predicament it was in last week. Its economy is structurally uncompetitive, with few meaningful domestic growth drivers. Consumers are still feeling the pinch from a 2014 tax hike. The weak yen still hasn't boosted productive capacity. Trade is still quite restricted. And the Abe government still lacks the political capital and/or willingness to take any of these issues on. These longer-term issues are reason enough for long-term investors to stay wary of Japan, regardless of any brief near-term rallies. Better opportunities abound elsewhere in the developed world.

[i] Of course the pun was intentional.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 9 - March 132026-03-16

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today