Personal Wealth Management / Economics

‘More’ Charts on Unemployment

Another lower-than-estimated jobs report seems to have stirred the ire of some in the punditry. But a broader view suggests this isn’t a major factor for investors, period.

“The report echoes recent data that suggest the U.S. economy is losing steam.”

“Awful.”

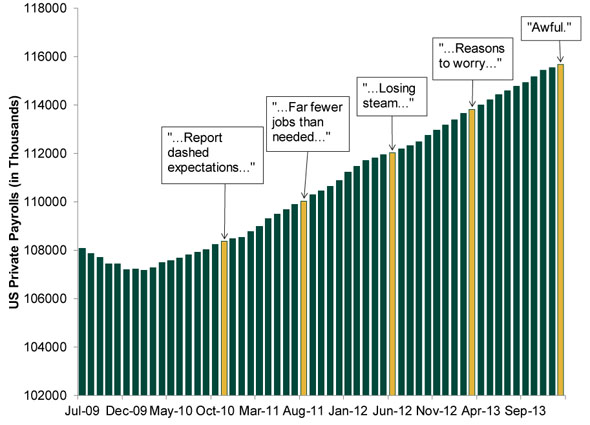

All of the quotes above could have applied to today’s BLS employment situation report showing employers added a total 113,000 jobs—76,000 less than economists’ consensus estimates. But only the last is from Friday’s report. In order, the coverage is of employment reports that missed expectations in November 2010, August 2011, June 2012 and March 2013—a period spanning nearly the entirety of a bull market and economic expansion that’s seen US stocks rise about 200%, the economy grow by an inflation-adjusted $1.6 trillion in output to an all-time high and, yes, total nonfarm payrolls grow by roughly 5 million.i Sometimes, investors would do well to take a step back and take in the totality of the situation to put economic conditions in broad perspective. To help, Exhibit 1 plots total US private sector payrolls (i.e., nongovernment) and overlays the quotes above with the report they refer to. It seems far from alarming.

Exhibit 1: US Private Payrolls, June 2009 – January 2014

Source: Bureau of Labor Statistics; Factset, as of 02/07/2014.

So it seems that on an absolute level, these fewer-than-expected hiring figures add up to more jobs. An obvious point, perhaps, but one often lost in the myopic sentiment of the day.

It’s true the improvement we’ve seen has been gradual, but that isn’t so vastly unusual as to trigger a mystery. Jobs are among the last indicators to improve—a factor neither new nor unique to this cycle. And it makes logical sense. Few employers hire before they need to in order to drive sales growth. Employees are a cost, which is exactly why layoffs happened in 2008 and 2009 in the first place.

You can see the typical historical pattern—stocks move first, then the economy, then employment—in this cycle. The bottom of the bear market immediately preceding this bull was March 9, 2009. GDP began growing in June 2009 (Q2), per the National Bureau of Economic Research (the official arbiter of recession dating). Private payrolls fell through February 2010.ii But if you waited until jobs grew to buy, you missed the first 11 months of this bull market—and a cumulative 67% of S&P 500 index total return. Investing based on unemployment data can be costly—especially if you’re investing not on a broad spectrum of real figures, but a singular, often misperceived data point.

We guess this is just a strange example of a case when less-than-expected can actually be more.

i Source: Factset, as of 02/07/2014. Real GDP for the period Q2 2009 – Q4 2013; Total nonfarm payrolls for the period June 2009 – January 2013; S&P 500 Total Return for the period 03/09/2009 – 12/31/2013.

ii Source: Federal Reserve Bank of St. Louis, Factset. Payrolls data is the Total Private Payrolls from the Establishment Survey of the Bureau of Labor Statistics Employment Situation Report.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

Market Analysis Due Diligence and the DOL’s DOA Fiduciary Rule2026-03-13

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today