Personal Wealth Management / Market Analysis

More IPOs Shouldn’t Slow Stocks

Despite recent Tech IPO buzz and bubble warnings, 2019 doesn’t appear to resemble 1999.

After years of relative calm, the IPO scene seems to be heating up. As several big-name firms—frequently Tech-related and referred to as mythical beasts[i]—go public, some investors see great buying opportunities. Many more, though, seemingly see threats—like new share supply overwhelming demand and knocking stock prices. Others fret high valuations for not-yet-profitable companies signal frothy markets—drawing comparisons to the late 1990s’ Tech bubble. In our view, these concerns lack support. Despite some high-profile IPOs, stock supply doesn’t seem set to surge—and present IPO activity is no bubble-like frenzy.

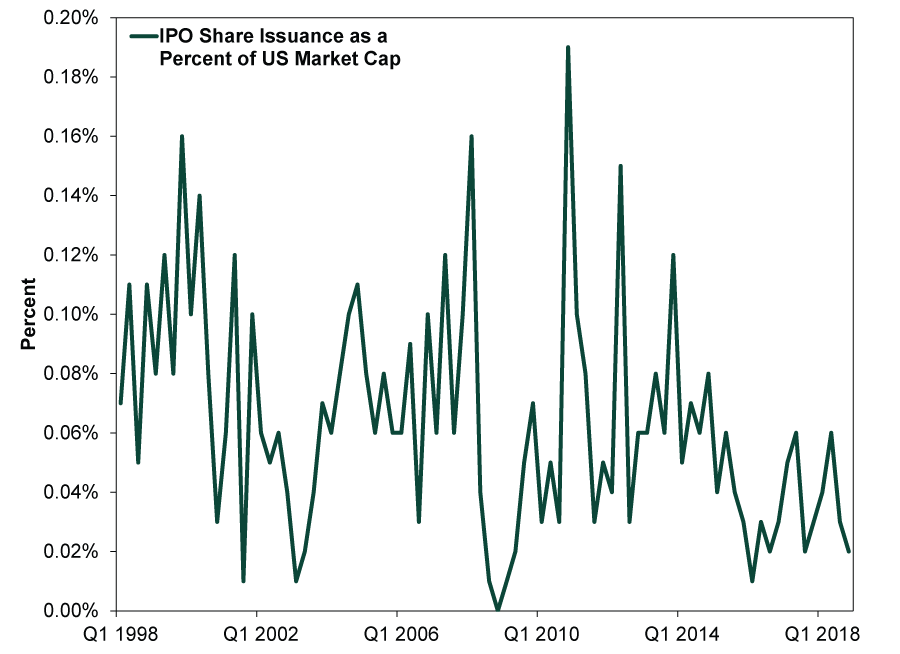

Digging into (and scaling!) the numbers helps illustrate this. IPO analysis firm Renaissance Capital estimates 234 companies may go public this year—good for $100 billion in new shares, a post-2000 record.[ii] While this sounds like a lot, measured against US stocks’ overall market capitalization, new IPO issuance is tiny. (Exhibit 1) Even with this year’s larger expected influx of new shares, IPOs would represent just a few drops in the bucket—far too minor to impact prices, in our view.

Exhibit 1: US IPO Share Issuance, Scaled

Source: FactSet and Bloomberg, as of 3/13/2019. US share issuance via IPOs and MSCI USA Investable Market Index (IMI) market capitalization, Q1 1998 – Q4 2018. MSCI USA IMI used in lieu of the Wilshire 5000 due to data availability, though the difference is negligible, as the former represents 99% of total US market cap.

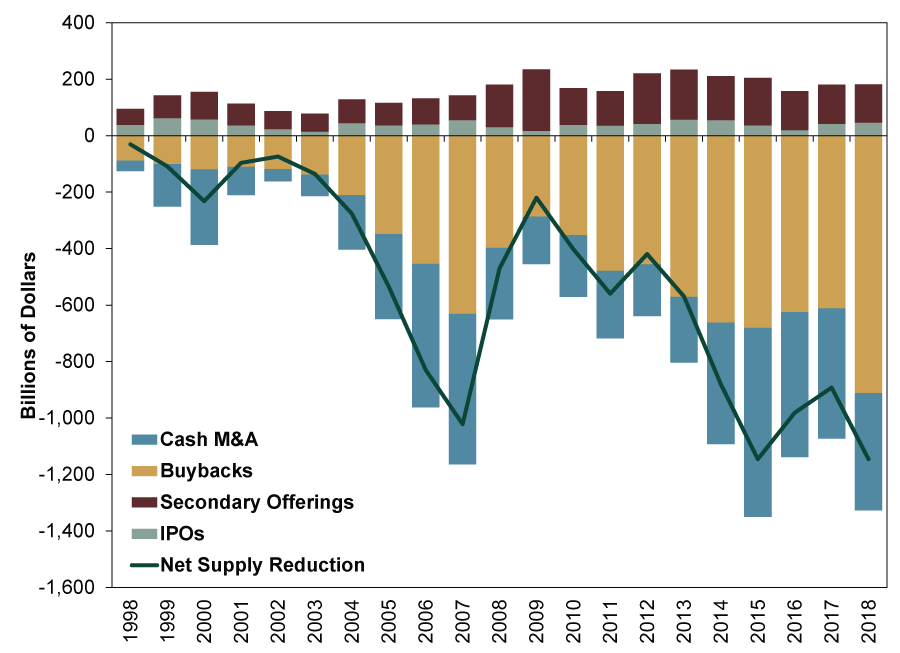

Folks fearing runaway stock supply could outstrip demand are at least barking up the right tree, conceptually, as this contributed to the dot-com bust and 2000 – 2002 bear market. But we see no evidence it is happening now. Not only is IPO issuance a tiny slice of overall share supply, it doesn’t automatically mean expanding supply, as there are other components. Some, like secondary offerings and share-based M&A, also expand it. Others, like cash-based M&A and buybacks, reduce it. Hence, even in a hot IPO market, share-destroying activities can outweigh new issuance, reducing supply overall. This has been the case for years, thanks mostly to abundant buybacks and cash-based M&As.

Exhibit 2: US Share Supply Is Falling

Source: FactSet and Bloomberg, as of 3/18/2019. US IPOs, secondary offerings, buybacks and cash-based M&As, Q1 1998 – Q4 2018.

Again, these data don’t capture 2019’s anticipated IPO pickup. But given projected buyback announcements in 2019 approach last year’s record levels, share deletion likely continues apace. To be sure, companies don’t always follow through on announced share repurchases. But if enough do, they will likely mitigate—if not fully offset—IPOs’ contributions to supply.

All this said, we don’t think volume alone reveals whether an IPO boom signals euphoria. To that end, assessing IPOs’ quality, not just quantity, is key—and we see a qualitative gulf between today’s IPOs and late-90s Tech offerings. The latter featured scores of firms with few sales and little by way of proven results or viable business plans—just associations with the dot-com craze. Euphoric investors snapped them up anyway, believing faddy slogans like clicks are the new profits and the new economy has arrived.

Consider the case of VA Linux, a computer company that went public in December 1999 with a $1.6 billion valuation despite negative earnings and a meager $17.8 million in sales.[iii] It soared 698% on its first day of trading—a record that still stands.[iv] Or theGlobe.com, an early social networking website with (again) negative earnings and just $1.2 million in revenue through the first half of 1998.[v] This didn’t prevent a 606% first-day surge when it went public in November.[vi] These, admittedly, are outliers—and had many skeptics at the time. But mostly giddy investors paid the skeptics little mind, instead bidding anything loosely tech-related up massively. In our view, we are miles from that frenzy today. Not all firms going public presently are profitable. But they aren’t fly-by-night upstarts, either. Plus, crucially, investors are scrutinizing their business plans. Those speculating on unprofitable firms can at least (rightly or wrongly) point to strong revenues, R&D plans and the like. Also, even the most anticipated recent IPOs didn’t soar anything like some of the 2000-era high fliers.

Overall, euphoria seems absent. Tech valuations aren’t surging.[vii] In 1999, Technology valuations averaged 36.1 versus 23.0 for the S&P 500 overall.[viii] Currently, they are 18.9 and 16.7, respectively.[ix] Some headlines hype IPO deals, but plenty more counter with skepticism and warnings. Caution abounds, not “it’s different this time!” pronouncements. All this isn’t to say you should rush out and buy newly public firms—see Ken Fisher’s recent USA Today column for more. But we think investors should distinguish between a healthy IPO market and a boiling one signaling a possible market peak. The latter seems a ways off yet—and plenty of worries remain to fuel this bull.[i] Unicorns, that is.

[ii] “Stampede of the unicorns: will a new breed of tech giants burst the bubble?,” Dominic Rushe, The Guardian, 3/30/2019.

[iii] “This IPO market is nothing like late 1990s craziness,” Paul R. La Monica, CNN Business, 4/1/2019.

[iv] “VA Linux Smashes IPO Record, Soaring Almost 700%,” Kevin Max, The Street, 12/9/1999.

[v] “This IPO market is nothing like late 1990s craziness,” Paul R. La Monica, CNN Business, 4/1/2019.

[vi] “Theglobe.com Sets Record for 1st-Day Trading,” Walter Hamilton, The Los Angeles Times, 11/14/1998.

[vii] Worth noting: The two ridesharing companies whose IPOs have garnered huge hype of late will actually reside in the Industrials sector—the Road and Rail industry, specifically. But Renaissance Capital estimates over half of 2019 IPOs will be Tech firms.

[viii] Source: FactSet, as of 4/8/2019. Average daily 12-Month Forward Price-to-Earnings Ratio for the S&P 500 Information Technology sector and S&P 500, 1/29/1999 – 12/31/1999 and 1/4/1999 – 12/31/1999. Tech valuations unavailable for 1/4/1999 – 1/28/1999.

[ix] Ibid. 12-Month Forward Price-to-Earnings Ratio for the S&P 500 Information Technology sector and S&P 500, 4/5/2019.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis What to Think of Another Aussie Rate Hike2026-05-05

-

Expert Commentary 3 Things You Need to Know This Week | PMIs, Consumer Confidence, US Housing Market

2026-05-04

2026-05-04 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—April 27 - May 12026-05-04

-

Expert Commentary This Week in Review | April Recap, UAE OPEC Announcement, US & Eurozone Q1 GDP

2026-05-01

2026-05-01

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today