Personal Wealth Management / Economics

Much Ado About UK GDP

The fretting over perfectly fine growth fits stocks fine.

Midway through November, a month and a half after September’s end, Q3 economic data like the UK’s GDP report (released late last week) are rather backward looking. Yet new GDP releases let pundits make comparisons, and the verdict among them seems to be that Britain is falling behind. You see, on a quarterly basis, UK GDP remains -2.1% below its Q4 2019 pre-pandemic peak, lagging other major developed world economies.[i] Fair enough, to an extent. For markets though, this is trivia. While economic growth supports stocks, it isn’t a race, and stocks don’t move in lockstep with GDP.

Pundits point to the UK’s slowing growth, which decelerated to 1.3% q/q in Q3 from Q2’s 5.5%, saying this means Britain’s recovery is faltering under the weight of post-Brexit supply disruptions and labor shortages.[ii] While those may be crimping growth at the margin, they aren’t unique to the UK. We doubt Brexit is the primary, or even a major, cause. For example, exports fell -1.9% q/q led by a -5.8% drop in goods exports.[iii] But the quarterly decline was driven by non-EU exports. Meanwhile, UK services exports rose, driven by financial services. Imports rose 2.5% q/q, mostly from non-EU fuel imports.[iv] Not everything is about Brexit. Also notable: Services imports rose, too, as easing travel restrictions allowed more Britons to vacation abroad.

Beyond trade, manufacturing and construction fell -0.3% q/q and -1.5%, respectively, due mainly to ongoing chip shortages for cars and building supply delivery delays.[v] But services, by far the UK’s biggest economic driver at close to 80% of GDP, rose 1.6% q/q, with accommodation and food services jumping 30.0% and recreation services up 19.6% in Q3.[vi] Services overall still slowed from Q2’s 6.5% q/q growth, but it is now just -0.7% below its Q4 2019 level. In our view, growth was always likely to slow as output approached pre-pandemic highs and the burst from easing restrictions faded.

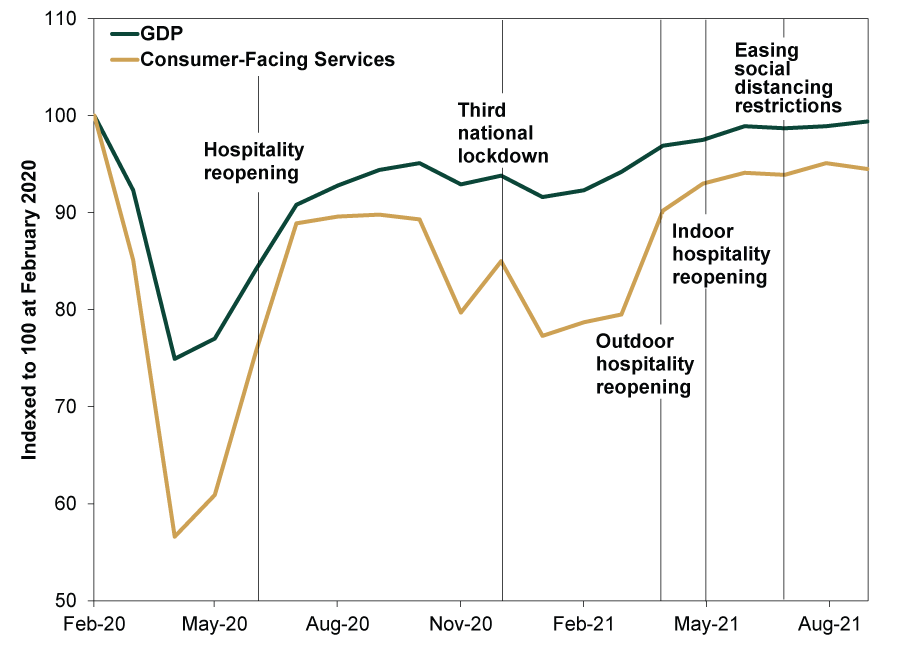

To us, this is pretty much the same story as the rest of the developed world: Outside of lingering supply chain wrinkles as the world restarts, economic activity—and growth rates—are returning to normal after the temporary reopening boom. The UK’s monthly GDP data show this more clearly. (Exhibit 1) September growth accelerated to 0.6% m/m, following a flattish July and August, leaving monthly GDP -0.6% below its February 2020 pre-pandemic level. The rebound in activity coincides with reopening milestones and the end of the so-called pingdemic, in which COVID contact alerts sidelined countless workers for weeks. The more restrictions have eased, the more activity has returned closer to pre-pandemic norms. The latest blip higher stemmed from the resumption of face-to-face doctor appointments, allowing human health activities to rise 6.4% m/m.

Exhibit 1: Monthly UK GDP Almost Back to Level, But Still Some Work Left

Source: ONS, as of 11/11/2021. Monthly UK GDP and consumer-facing services, February 2020 – September 2021. Consumer-facing services consists of retail trade, food and beverage serving activities, travel and transport, and entertainment and recreation.

While overall services in the UK has unsurprisingly tracked GDP closely, the subset of consumer-facing services continues to lag, remaining -5.5% below what they were in February 2020.[vii] As the Office for National Statistics (ONS) noted, the main culprit for September’s -0.6% m/m dip in these categories was a -13.3% decline in car sales from lack of supply. But as the ONS also pointed out, travel and entertainment categories are starting to pick up strongly. Although they remain historically depressed, as restrictions lift, they appear to be following a familiar script: big gains as pent-up demand releases, which subsequently subsides. This hasn’t been a smooth process, occurring in fits and starts at different times in different sectors. More COVID waves this winter could spur further wobbles, and supply chain issues may persist. The UK economy has shown over the last year it can handle them though. We suspect markets are well aware of this, mitigating any impact on stocks.

Looking forward, there is likely some more catch-up growth ahead, particularly as supply bottlenecks resolve. But the potential for new kinks aside, we think markets have mostly moved on. Meanwhile, many seem to be overlooking recent positives. UK steelmakers and fertilizer plants have quietly started production again. This is as the energy crunch subsided with wind power generation recovering. Port operators are also rerouting traffic and clearing logjams, which doesn’t get as much attention as when there is “chaos,” but it undercuts perceptions trade is frozen. Volumes are surging even as freight rates hit record levels—there is ample incentive (profits) to move inventory.

Pundits, though, still seem to be searching for a second shoe to drop. They expect inflation, Bank of England rate hikes or Brexit (finally) to bite. They will likely have a long wait, in our view. Not only are these items unlikely to derail the economy, they are well known issues markets have mulled over for months—and found wanting. If they don’t spark a downturn, the result would be a better-than-expected outcome for stocks to enjoy. This doesn’t mean UK stocks are likely to lead the world—sector composition is a headwind. But they should still participate in this global bull market.

Ultimately, markets don’t rate recoveries by comparing country to country, but against prevailing sentiment. On that score, we think the UK is likely to make out fine.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today