Personal Wealth Management / Market Analysis

Mutually Assured Devaluation?

Talk of competitive devaluations and currency wars seem to be en vogue lately. Let’s take a closer look at recent history and the underlying theory.

Central banks have taken on an ever-more activist role in enacting unconventional—and often misguided—policies over the past few years. Many folks see these actions as efforts by central banks to force down currency valuations relative to heavy trade partners, making exported goods cheaper and, hence, more attractive. In some corners, this is called the academic-sounding “competitive devaluation.” Others use a more bellicose term: Currency Wars—and fear it as a form of trade war.

A very basic discussion of the theory underpinning competitive devaluation goes something like this:

- GDP’s calculation uses net exports (exports less imports).

- Exports therefore buoy headline growth, while imports detract.

- A weak currency relative to trading partners’ can make exports more affordable to trading partners.

- Currency valuations are often influenced heavily by relative interest rates—lower rates than major peers can mean a weaker currency.

- Thus, by reducing relative interest rates or directly intervening in currency valuations, some suggest they’re promoting growth.

Here’s the problem—the theory starts from a fallacious point and ends with an equally fallacious point.

While we don’t argue at all with the notion rising exports relative to imports results in a positive contribution to GDP, we would suggest this isn’t directly equivalent to economic health. In fact, pursuing a policy targeting increased exports merely selects a favored portion of the economy, harming others. Case in point: Shinzo Abe’s Japan.

Japan’s Grover Cleveland won non-consecutive reelection largely on a platform of government intervention in the economy. One intervention Abe suggested was prodding the Bank of Japan (BoJ) to initiate further quantitative easing, with an end goal of weakening the yen. Abe seemingly believes Japanese exporters stand to benefit if the yen were weaker—causing Japan’s exports to fall in price abroad. And the BoJ acceded, announcing a new, unlimited round of QE. And in the short term, the yen has fallen.

However, before hailing Abe’s policy a success, consider: There’s little real evidence an entire economy benefits from a cheap currency.

Assuming continued successes, Abe’s quasi-mercantilist policy might help exporters, but it does precisely the opposite for importers—it makes foreign goods more expensive. In post-Fukushima Japan, much of the power generation is underpinned by liquefied natural gas and other imported sources. Those sources would be more expensive due to a weak yen, hampering economic growth, not fostering it. Further, many times the very exporters Abe seeks to aid were importers a step earlier along the global supply chain. Abe’s narrow view theoretically and simplistically favors one group to the exclusion of others—a common macroeconomic error.

But that’s just the start. The other often-forgotten point surrounding competitive devaluation seems to be the fact exchange rates move in pairs. The dollar, for example, has no absolute up-or-down tick. It ticks versus something in a market: yen, euro, krona, kiwi, loonie, basket of trade-weighted currencies, Bhutan’s ngultrum. So one nation’s actions alone aren’t the only factor—meaning, assuming it’s intended, one country’s attempted devaluation can easily be countered.

Given how liquid and fungible currency markets actually are, there’s no really consistent devaluation tool...or, we guess, weapon...to employ. Take the often-discussed current version—QE. Perhaps it occasionally influences the dollar’s relative standing, but it’s hard to discern any impact on others. For example, consider the Fed’s actions over the past few years.

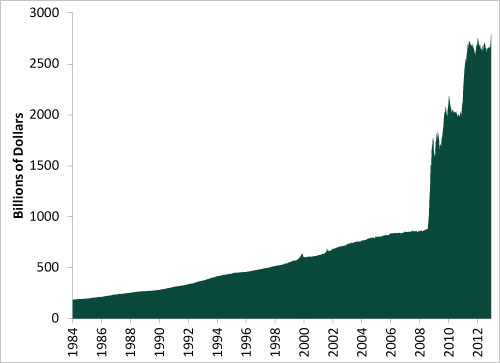

If you took the Fed’s balance sheet expansion at face value, you might think Exhibit 1 would correspond to a consistently declining dollar versus a broad, trade-weighted basket of currencies.

Exhibit 1: US Federal Reserve Balance Sheet

Source: Federal Reserve Bank of St. Louis.

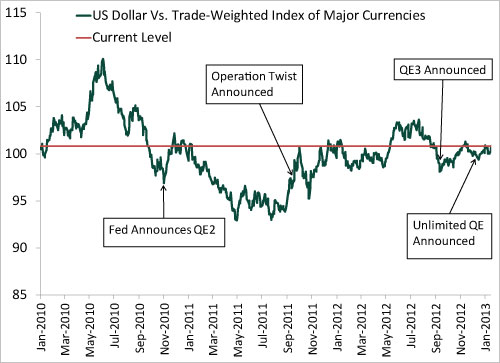

And for a time, the dollar did fall after QE2 was announced in early November 2010 (though correlation doesn’t necessarily mean causation). But it isn’t as though the Fed stopped with QE2, subsequently announcing Operation Twist, QE3 and QE-Infinity. Yet, as Exhibit 2 shows, the dollar hasn’t wiggled much in the wake of those moves—and in fact, it’s since largely recouped the post-QE2 announcement decline and sits incrementally above where it began 2010.

Exhibit 2: US Dollar Vs. Trade-Weighted Currency Basket (Dollar Indexed to 100 at January 2010)

Source: Federal Reserve Bank of St. Louis. Basket includes euro currency, Canadian dollar, British pound, Swiss franc, Australian dollar, and Swedish krona. 01/01/2010 – 01/18/2013.

So in essence, while competitive devaluation may be a rather misguided goal some countries are pursuing, attaining it is far from assured. But even if they did, the results would likely be a combination of pluses and minuses. And assuming two countries compete for a weaker currency, the likely outcome isn’t necessarily devaluation for all parties involved.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Around the World in Tax Policy Talk2026-05-15

-

Expert Commentary This Week in Review | US Inflation, US-China Visit, Fed Chair Confirmation

2026-05-15

2026-05-15 -

Market Analysis Reader Mailbag: May 20262026-05-14

-

Politics The UK’s Political Ructions Hide a Better-Than-Feared Economy2026-05-14

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today