Personal Wealth Management / Market Analysis

Myopic Media Mind Tricks

A primer in analyzing the supposed "cause" of market volatility.

Thursday, investors were barraged with two things we at MarketMinder make every effort to innoculate readers against: Myopic, skewed headlines and sharply volatile markets that give them fear-induced credence. Volatility such as the -2.0% S&P 500 return on Thursday can be tough to stomach, but it's a mistake to read too much into one day's action.[i] Virtually anything can cause stocks to wobble to this extent and fact is the S&P fell -2% or more in a day an average of once every 30 trading days in the thirty years from 1982 - 2013.[ii] This is not to dismiss volatility; it is to say big moves aren't so abnormal that there must be some bigger meaning behind them. But that doesn't stop the media from trying, which is bad for investors but a plus for us because, you know, it gives us something to do. We at MarketMinder scan north of 100 websites from around the world, apply Fisher Investments' unique, proprietary research and try to leverage the perspective of a global money manager to bring you a financial professional's insight. Act as a media filter, if you will. This requires digging deep beneath headlines, and we generally aim for those stories not from one site, but repeated ad nauseum so they seem like everyone who's anyone agrees. (Or those stories no one is talking about, but we believe should be.) Now, mind you, the media's quest for meaning isn't their fault-without eyeballs, their ratings go poof. But taking these headlines at face value is dangerous for investors, as we'll show.

Argentina was downgraded to Selective Default by Standard & Poor's late Wednesday, the nation's eighth default. The immediate ripple effects, as covered aptly by our own Elisabeth Dellinger here, are pretty much nil. But still, this drove the commentariat nuts, with some oddly claiming Argentina would lose big. Tying this to stocks presumes no one was aware. Default, however, was the widely expected outcome.

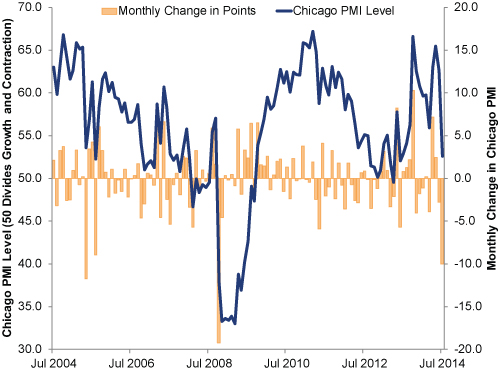

While the Argentine story grabbed the most headlines, it was not alone nor the most off-base news. The ISM Chicago Business Barometer (a Purchasing Managers Index, or PMI) came out Thursday morning, and it really laid an egg.[iii] July's reading showed a 10.0 point drop from June, which was quickly dubbed The Biggest Drop Since October 2008. And it was! But that isn't the full story. You see, October 2008's reading fell 19.2 points-nearly double July 2014's-to 37.8 (readings below 50 are contractionary, so this is a deep dive) during the height of the global financial crisis. July 2014's dip put the index at a still expansionary 52.6. In that way, it seems much more in line with May 2005's 11.7 point drop to 53.6. Looking at those big drops during expansion should be your sign to question whether a regional output gauge is really worth all the pixels it got. Consider Exhibit 1, which shows the monthly change in the index (orange bars) against the index level (blue line). Those bars are all over the map. It's a regional gauge and this is a PMI-a survey-attempting to study the breadth of growth in a narrow area. Volatility comes with the territory.

Exhibit 1: Chicago PMI (ISM's Business Barometer)

Source: Factset, ISM Chicago Business Barometer, monthly change and level for the period 07/2004 - 07/2014. Seasonally adjusted as of 07/31/2014.

Eurozone inflation, if you want to call it that, also grabbed headlines for its near non-existence. Thursday's flash consumer price index release showed overall prices grew only 0.4% y/y in July, down from 0.5% in June. Many pundits bang the drum that a deflationary spiral looms in Europe, hoping for more monetary moves from the ECB. But in actuality, the eurozone is not sliding into deflation. It has experienced disinflation (a slowing rate of price increases), which may or may not become deflation-economic data don't move in straight lines, and if you don't believe that, please see Chicago PMI.

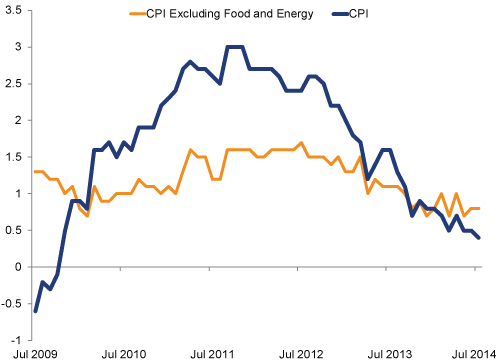

But the real kicker here is most of the decline is tied to the really volatile prices central bankers strip out when weighing monetary moves. Like energy prices, which fell -1.0% y/y in July. Or food prices, which fell -0.3%. No other category in the flash report fell.[iv] In the near term, these factors are more subject to patterns like weather than money supply-which is why central banks tend to strip them out when weighing monetary moves. Stripping them out, prices rose 0.8% y/y in the month-unchanged from June. (Exhibit 2)

Exhibit 2: Eurozone Year-over-Year CPI and CPI Excluding Food and Energy

Sources: FactSet, Eurostat. Eurozone Harmonized CPI for the period 07/2009 - 07/2014.

Always try to avoid getting caught by the media's myopia. Sometimes, looking at data will help. Others, it's just about a simple logic test.

Here are three examples from one article. First, we're told Ukraine rhetoric is heating up, and that's the culprit. But if bombs, rockets and missiles haven't driven much volatility, why would words? Next, we're told "spiking" 10-year Treasury rates may have caused the volatility. Which may seem logical until you investigate what is meant by "spiking." A minute-by-minute tick of the 10-year shows rates traded in a bandwidth of 2.54% to 2.61% all day Thursday, closing basically unchanged.[v] We are more likely to call seven basis points a "rounding error" than a spike, whatever the cause. A third explanation that doesn't pass the logic test: We're told a sports-equipment firm lowering full-year earnings guidance by €180 million this fiscal year or so tied to Russia concerns contributed to the market-wide dip. Hey, maybe. But global market capitalization is on the order of $43 trillion (with a T), so we kind of doubt anything in the millions made markets tremble much. But also, that sports-equipment maker's blaming Russia concerns was only part of its lowered target-the rest was poor results in golf goods.

Digging into actual data and applying a basic logic test are two key tools we use to sift through news. (Another is eliminating mined anecdotal evidence.) When you see articles digging deep for meaning in a single day's volatility, we'd suggest handling them with extreme skepticism.

[i] Source: Factset, S&P 500 Total Return, 07/31/2014.

[ii] Source: Factset, as of 01/23/2014. S&P 500 Price Returns for the period 12/31/1982 - 12/31/2013.

[iii] Not a golden egg, either.

[iv] Remember: Flash is econospeak for incomplete data series that comes out quickly.

[v] Source: Factset, intraday change in US 10-year Treasury rates, 07/31/2014.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Big Gas Price Jump, Still a Small Spend2026-05-29

-

Market Analysis What AI Tech Stocks Are Signaling About This Bull

2026-05-28

2026-05-28 -

Market Analysis Putting Negative Equity Risk Premiums in Proper Perspective2026-05-27

-

Economics A May Global Economic Check-In2026-05-26

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today