Personal Wealth Management / Market Analysis

Navigating a Choppy Stock Market

While it isn't easy, we'd suggest the best thing for investors to do amid recent volatility is tune out the noise and remain calm.

Keep calm and carry on.

No, we won't offer any cutesy memes featuring those words and a crown, but that is nevertheless our advice amid a volatile stretch pushing US and global stocks near correction territory. (A correction is a short, sharp, sentiment-driven drop exceeding -10%.) US stocks fell -5.2% Thursday and Friday combined. Global stocks fell slightly less, -4.3%.[i] From their highs, US and global stocks finished last week down -7.2% and -8.5%, respectively. And, Monday morning, stocks opened sharply lower before bouncing. At one point, the S&P 500 Index (price level-not including dividends) registered the first correction since 2012, then bounced back above the threshold.[ii] Whether the S&P or world stocks finish below -10% from their prior peaks or not remains to be seen, but however you measure it, these past few days haven't been terribly pretty and seem to have unleashed a good solid dose of fear. However, this move has the sharpness, speed and fear-inducing characteristics that typify corrections-not the greedy buy-the-dips, ignore-the-negatives sentiment common when bears begin.

Our next piece of advice: Turn off the financial media.

Blaring red headlines shrieking "BREAKING NEWS: Futures Point to Massive US Sell-Off at Open" are not doing you any service whatsoever.[iii] Tune out. You also don't need to hear folks drone on about how many points the 30-stock, price-weighted Dow Jones Industrial Average is down. Or display tickers from around the world showing you how much indexes you can't even invest in are down in China. Getting caught up in their negativity is a well-trod path to financial ruin. Opt out.

Stocks falling this fast amid fear-inducing headlines is much more characteristic of a correction than a bear market. As we've written on these pages many times, corrections and correction-like short-term volatile moves are commonplace in bull markets. Being sentiment-driven (caused by investors' whims suddenly shifting), they are, unfortunately, unpredictable. It is entirely possible there is further yet to fall. It is entirely possible the worst of the selloff is now over and a rally is immediately ahead. But the key is, you shouldn't base investment decisions on past movement. And that seems to be what many in the media are engaged in doing. This is a recipe for selling low after buying higher, the opposite of pretty much every investor's intent.

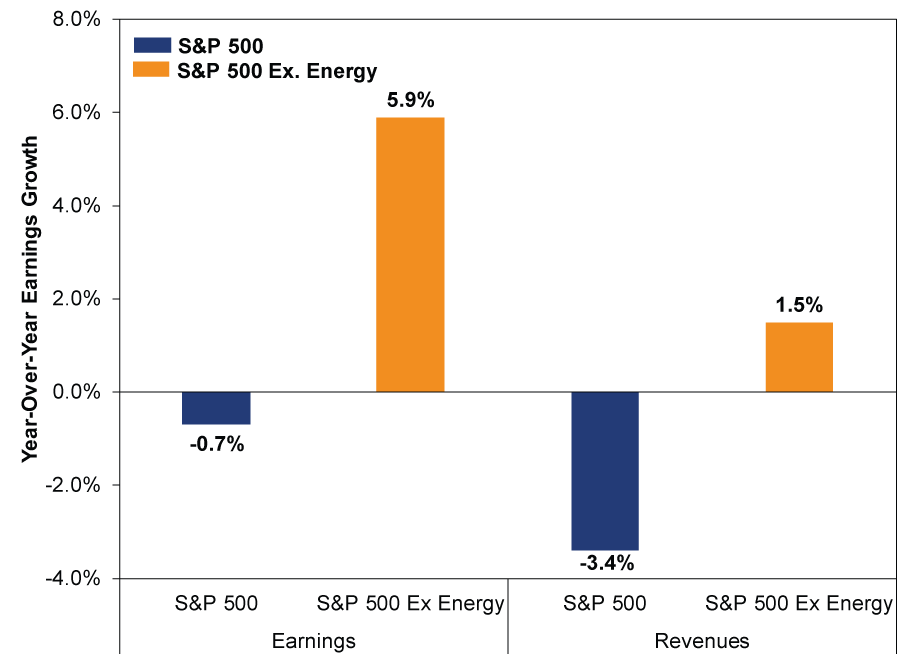

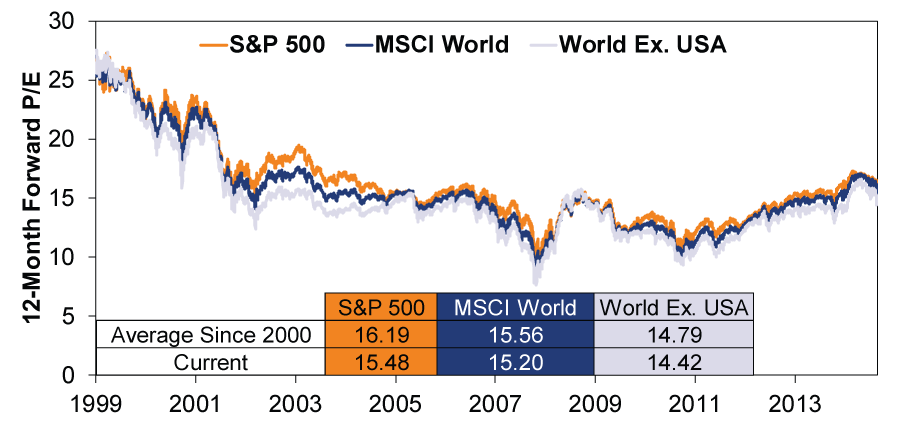

Now, the question many seem to be pondering is: Is this worse than a correction? At this point, we see little reason to think so. Market fundamentals have not radically shifted recently. While media has made much of the S&P 500's headline earnings dip, this is a sector-specific phenomenon, largely. As in this year's earlier reports, Q2 earnings outside Energy stocks were solidly positive, rising 5.9% y/y with 482 out of 500 firms reporting. Revenues, too, are positive outside Energy, rising 1.5% y/y. (Exhibit 1) Valuations are above average but not alarmingly so. (Exhibit 2). Sentiment largely seems skeptical, as measured by the very reaction we've seen commonly to the recent weakness and flattish year.

Exhibit 1: S&P 500 Earnings and Revenues

Source: FactSet, as of 8/24/2015.

Exhibit 2: 12-Month Forward P/E Ratios, MSCI World, USA and World Ex. USA

Source: FactSet, as of 8/24/2015.

Focus on China seems to be blocking out news from the rest of the Earth. Today's selloff seems to stem either from fear China won't intervene enough or fear it will. Friday, China's Flash Caixin/Markit Manufacturing PMI, which showed 47.1% of firms reported rising output, was all the rage. As we've discussed, China's economy has slowed in recent readings-but that has been true for about three years. But this isn't the only news in the world! Far less discussed: the eurozone's composite PMI ticked further into expansionary territory, with forward-looking new orders rising nicely.

The Conference Board's US Leading Economic Index did buck its trend, falling -0.2% m/m in Thursday's release, which is a figure we closely follow. However, only 2 of 10 categories were negative: Building permits, which detracted 0.54 percentage point, and stock prices, which detracted 0.01.[iv] LEI's negative read, itself out of step with the recent uptrend, was due to a big, one-off dip in building permits-positive in four of the preceding five months.

Recent news just doesn't hint at anything fundamentally shifting in the global economy and markets. If your goals and needs are commensurate with investing in stocks, the single biggest risk you can take is exiting stocks. We humbly suggest the only time to do so is when you strongly believe you see something others don't that alludes to a likely bear market, offering you an opportunity to exit now and buy back in later and lower. Without that, making a move amounts to mere speculation on a possibility. Hence, in our view, equity investors are best served to keep calm.

[i] Source: Factset, as of 8/21/2015. S&P 500 Total Return and MSCI World Index with Net Dividends.

[ii] Source: FactSet, S&P 500 Total Return, 4/2/2012 - 6/1/2012. US stocks fell only -9.6% from April 2 to June 1, but we give it the nod anyway because world stocks breached -10%.

[iii] That headline is a direct quote from CNBC Monday morning, 5:24 AM Pacific Daylight Time.

[iv] And even this has an asterisk. The Conference Board averages the S&P 500 price index's daily closing prices during the month to determine stocks' contribution. The average daily closing price was down in July from June. However, July's actual closing index level was up from June. Not that we're quibbling, just noting a little quirk we think you should be aware of.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today