Personal Wealth Management / Politics

No Chinese Hard Landing

China reported third quarter real GDP Tuesday at a big 9.1% year over year. It missed estimates of 9.3% and decelerated from Q2’s 9.5% year-over-year rate . But with many fearing a Chinese hard landing, this still-fast growth seems a normal deceleration.

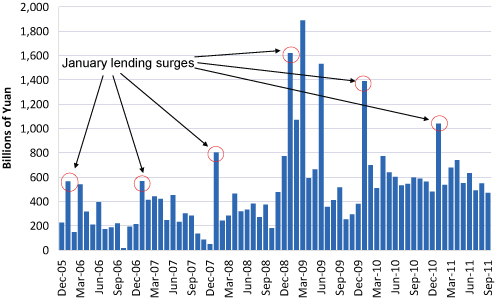

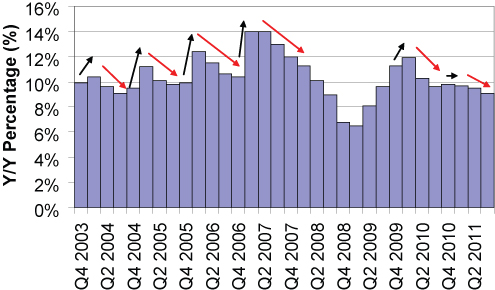

And in China’s case, it seems a planned deceleration. Tied to its use of annual loan quotas, China typically has a jump in loans to start the year. With a limited bond market and most funding coming through the banks, this avalanche of liquidity typically causes economic growth to jump in Q1. As the year progresses and banks begin to restrict loans, GDP usually decelerates slowly. Exhibit 1 shows the increase in lending that occurs at the start of each year, and Exhibit 2 shows the coincident acceleration then deceleration in GDP annually.

Exhibit 1: China New Yuan Loans

Source: Thomson Reuters

Exhibit 2: Q1 China GDP Surges on Annual Loan Quotas

Source: Thomson Reuters

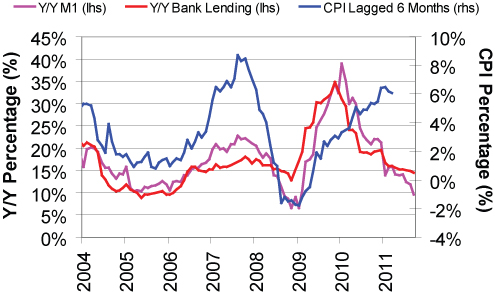

In additional to normal seasonality, this year, China is intentionally attempting to slow its economy more than usual to help combat inflation. Its primary tool here, again, is loan quotas. China has slowed loan growth recently to 14.5% year over year in September—which took money supply down to a decade low. Inflation should follow suit at a bit of a lag and is already showing signs of rolling over. (See Exhibit 3)

Exhibit 3: China Money Supply Vs. Loan Growth

Source: Thomson Reuters

The lower inflation numbers, along with money supply and GDP figures near the lower range of what the government has tolerated in the last decade, should set up a strong 2012—which is likely exactly China’s aim.

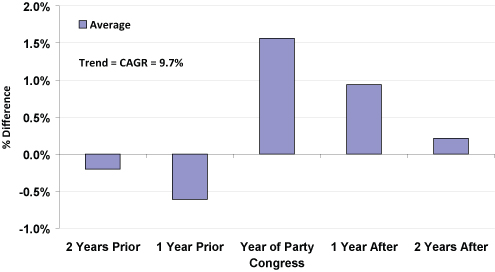

The Chinese government has liberalized in many ways over the past few years, but it in fact remains communist. Therefore, it requires high economic growth and low inflation to maintain social stability given the populace has few ways to peacefully effect significant change. If economic growth falls too far or inflation gets too high, you could get another Tiananmen Square. That’s the last thing the government wants in a normal year—but 2012 is an election year, when the Communist Party announces a new set of rulers. Historically, the government accelerates the economy in these years to maintain stability during the handover of power. (See Exhibit 4)

Exhibit 4: Relative China GDP Growth: Annual 30-year Trend

Source: Thomson Reuters: 1980-2010

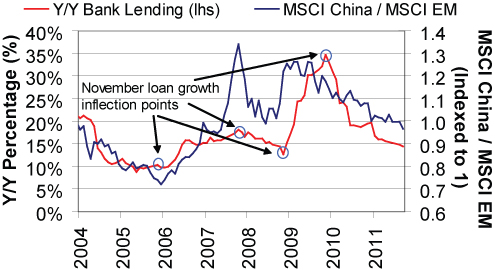

There’s no reason to think 2012 will be any different. If the Chinese government follows historic precedent, look for an announcement of a looser annual loan quota for 2012 at some point in November 2011—which could be a tailwind for China’s equities, as it was in the previous election cycle. (See Exhibit 5)

Exhibit 5: China Loan Growth Vs. Relative Performance

Source: Thomson Reuters

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Don’t Doubt the Old World2026-07-16

-

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today