Personal Wealth Management / Financial Planning

No Inside Track

Do CEOs’ inside trades provide investors helpful hints?

Do retail investors gain an edge by following inside traders?

Common wisdom claims they do—that CEOs and other execs have the best view into a company’s future profits, so their buy/sell decisions are clues investors should follow. A new study by S&P Capital IQ purports to back this up, finding companies whose CEOs were “net buyers” from April 30 through October 31 outperformed the Russell 3000. However, if you break down the study’s underlying data, it’s far less compelling. Plus, there are numerous philosophical reasons investors shouldn’t merely follow the CEO herd—it isn’t at all guaranteed to result in well-timed buys or sells, and it could lead investors astray from their long-term goals.

If you decide to copy an insider’s trade in your own portfolio, you’re betting their decision to buy or sell somehow predicts their company’s future performance—that insiders are trading on the likelihood of future profitability and they’re more likely than other folks to be right. Problem is, not all inside trades are based on the executive’s expectations for future earnings. Some execs might buy simply to shore up investors’ confidence. Others might buy for personal emotional factors, like attachment to the company. Selling rationales vary, too. Insiders typically hold high concentrations of company stock—often due to the options included in their compensation packages. Holding all these shares once the options are vested and the lock-up period clears heightens company-specific risk. Even if executives have a high conviction in the company, many will reduce their holdings to diversify. Some execs might also sell because they need the cash for a major purchase, like a new home. Retail investors simply don’t have any insight into the “why” behind insiders’ trades—and the “why” matters.

Then again, even if insiders are buying because they’re confident in future returns and selling because they aren’t, their decisions aren’t necessarily very telling. Very little information about companies isn’t already widely known. Every listed firm’s financial statements are available online, and major deals and personnel changes are disclosed. Any regulatory changes affecting them go through long periods of public comment and legislative debate. Even if insiders do know something others don’t, there is no guarantee they’re interpreting the information correctly. Making well-timed trading decisions isn’t just about having unique information—it’s about correctly assessing this development’s impact on future earnings. Maybe insiders overestimate the profitability of a potential merger or acquisition. Maybe they have too much—or too little—faith in a still-secret product launch. Maybe the plan they were riding on gets scrapped at the last minute.

Plus, CEOs are people. They’re subject to the same behavioral errors as the rest of us. They could be biased toward their company or industry. They could get excited after a big run and chase heat or panic after a drop and sell out of fear. They also might just not be very good assessing their own company’s outlook. Maybe they can’t see deteriorating fundamentals sector-wide. They could overlook the unintended consequences of a regulatory change that could impede future profits. They could over- or underestimate future demand for their products and/or services. And, unfathomable as this may be, they could miss regulatory developments and trade barriers in other countries—yes, we assume execs would be perfectly in tune with these developments, but no one is perfect. If they were, companies wouldn’t fail, lose money or miss earnings estimates. CEOs are surprised and disappointed all the time.

This all explains why the new study on CEO trades shows investors who buy when CEOs buy aren’t guaranteed to do well. The study tracks every CEO purchase from April 30 through October 31 and lists its five-day, one-month and three-month forward returns—and the same for the Russell 3000. First, these are extraordinarily short time periods and say nothing about how these firms do over the mid to longer term, which is more important for long-term growth investors.

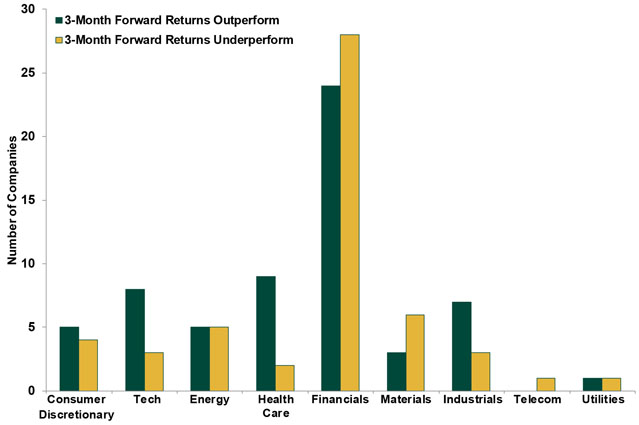

Setting that aside, the findings suggest CEOs aren’t amazingly good at trading their own firms. Of the trades included in the study, 115 had forward three-month returns available (the remainder were too recent). Of these, 62 beat the Russell 3000 and 53 lagged. Perhaps this seems at least somewhat telling—until you break the results down by sector. As shown in Exhibit 1, the winners were concentrated in Health Care, Tech, Industrials and Consumer Discretionary—all of which outperformed during the sample period. In other words, CEOs’ success largely followed sector-specific trends. You don’t need CEOs to make these sector calls for you—the sector breakdowns of S&P 500 earnings and revenues would largely steer you toward the same categories, and they’d tell you far more than an insider trade.

Exhibit 1: CEO Trades by Sector

Sources: S&P Capital IQ, The Wall Street Journal, as of 11/18/2013.

Finally, those who do follow insider trades run the risk of taking a short-term, bottom-up approach, which can erode the benefits of long-term investing. If you recreate executives’ trades in your own portfolio, you’re essentially introducing their goals, biases, emotions and potential flubs into your own finances. Common sense says this probably doesn’t mesh well with your own unique goals, objectives, time horizon and financial circumstances—which should always and everywhere be the basis of a long-term investment strategy.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today