Personal Wealth Management / Economics

Not All Soft GDP Reports Are the Same

We have to dig beneath the surface to see what weak GDP reports really mean.

Here is a common media refrain: The global economy is weakening. Q1 disappointed many, and analysts are ratcheting down forecasts across the board. And hey, we get it, Q1 wasn't exactly pretty. US GDP contracted. So did Canada, Brazil and Russia. The UK grew, but at the slowest pace since Q4 2012. Lest you fear 34% of the global economy is weakening, however, take note: Not all slowdowns and dips are created equally. Assessing which countries to emphasize in your portfolio and global economic health requires digging beneath surface-level similarities.

US GDP's Q1 contraction is more the product of several fleeting and quirky factors than an ominous sign. For one, a labor dispute impacting US West Coast Ports played havoc with import and export data, delaying activity until its late-February resolution. Then, when it was resolved, goods imports surged 7.5% m/m in March. GDP's calculation uses net trade (exports minus imports), and in Q1, delayed exports didn't offset imports' spurt, so net trade detracted a huge 1.9 percentage points from growth. That is GDP math, and it drove GDP into negative territory. But surging imports don't signal economic weakness-they show strong domestic demand. And, for good measure, there is likely a big revision coming. It appears the US Bureau of Economic Analysis' (BEA) seasonal adjustment has failed to account for winter properly in recent years, skewing Q1 data downward. The BEA announced last week it is currently working to rejigger it. And, most importantly, more recent data suggest growth is underway, and The Conference Board's US Leading Economic Index (LEI) is in a solid uptrend-suggesting the economy continues growing looking forward.

Similarly, slow UK growth isn't as bad as it may seem. Headline growth slowed to 0.3% q/q (1.2% annualized), but here too net trade was the biggest drag, reducing quarterly growth by 0.9 percentage point. Exports, sluggish throughout this expansion, fell slightly, detracting 0.1 percentage point from growth. The bigger factor? Imports surged 2.3% q/q, accounting for the other 0.8 percentage point detraction, which doesn't signal weakness. Trade aside, business investment grew by 1.7% q/q, partly retracing the prior two quarters' drops and is closing in on all-time highs. Consumer spending also grew. And, like the US, UK LEI is signaling more growth ahead.

The other major contracting areas-Canada, Brazil and Russia-however, have non-mathematic issues that, particularly in Russia and Brazil, run deeper. Their economies are (to varying degrees) natural resource-dependent, leaving them vulnerable to commodity prices' slump. "So goes oil, so goes growth" is oversimplified, but close.

If mining and oil extraction are two major industries for your economy, you don't want prices falling off a cliff-it discourages production growth. When production goes down, oil-rich regions see less activity, with support industries, government tax revenue and jobs all taking a hit. This is precisely what has happened. Global oil supply growth has easily outstripped demand growth in recent years, causing prices to collapse. High metals prices in the mid-2000s incentivized huge investment in mines, only to see demand growth falter since 2011. As a result, oil and metals prices have cratered. Brent crude prices are down about 40% in the last year. Russia and Canada are in the top five oil producing nations. Brazil is in the top 15. According to the World Bank, natural resources amount to roughly 5.2% of Canada's and 6.5% of Brazil's. Russia's? 18%. Canadian, Brazilian and Russian energy firms' profits have been hammered. Iron ore is down more than 30% since last June, contributing to woes for firms in Brazil and elsewhere.

Yet resource-dependent countries are a small chunk of the global economy. Combined, Brazil, Russia and Canada represent 9.6% of the global economy. The US, UK and China are a combined 40%, while natural resources comprise 1.2%, 1.0%, and 4.6% of their economies, respectively.[i] The eurozone's big four economies-Germany, France, Italy and Spain-have scant natural resources exposure. The total GDP of nations with natural resources rents exceeding the world's average amounts to less than a quarter of global GDP. Commodity production isn't the key to growth the world over.

Not even all resource-heavy nations are the same. Some are suffering doubly from issues that have little to do with a reliance on commodities, while others have strengths to help offset resource weakness.

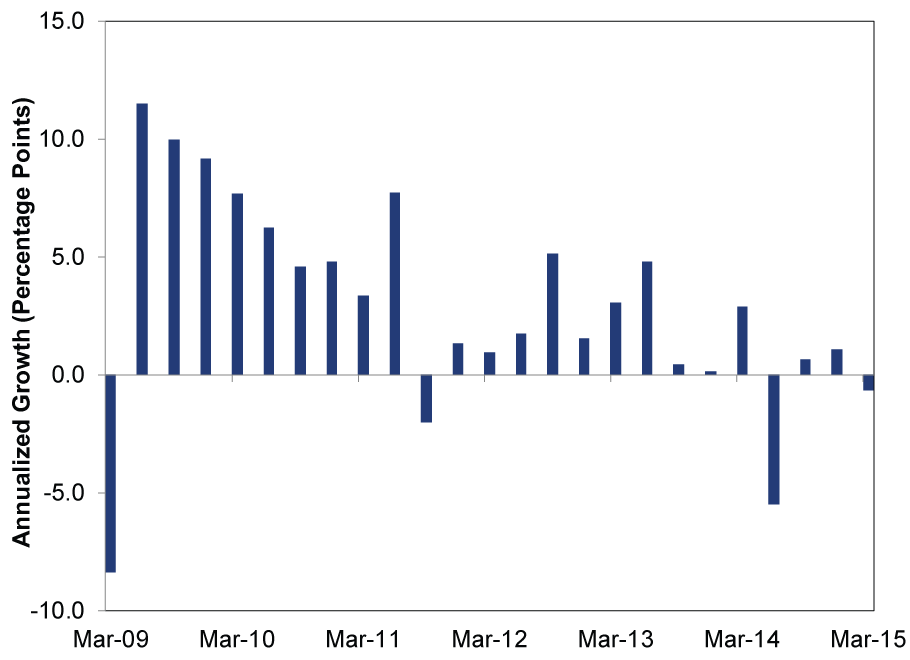

In Brazil, government interference has long caused economic pain-even within its resources sector. Fuel price controls-a long-standing policy-cushioned consumers against high energy prices in the mid-2000s until last year, when global prices fell below the government's set price. That stimulated the national oil firm, Petrobras, to ramp up production in spite of falling global prices. Outside Energy, the government imposed steep tariffs to protect domestic manufacturers, driving consumer prices higher and reducing efficiency. In banking, the government has an increasingly heavy hand, accounting for the lion's share of loan growth. All these factors sum to hot inflation and stagnant growth, and as Exhibit 1 shows, Brazilian weakness is nothing new.

Exhibit 1: Brazil GDP Q1 2009- Q1 2015 (Annualized)

Source: Factset, as of 6/1/2015.

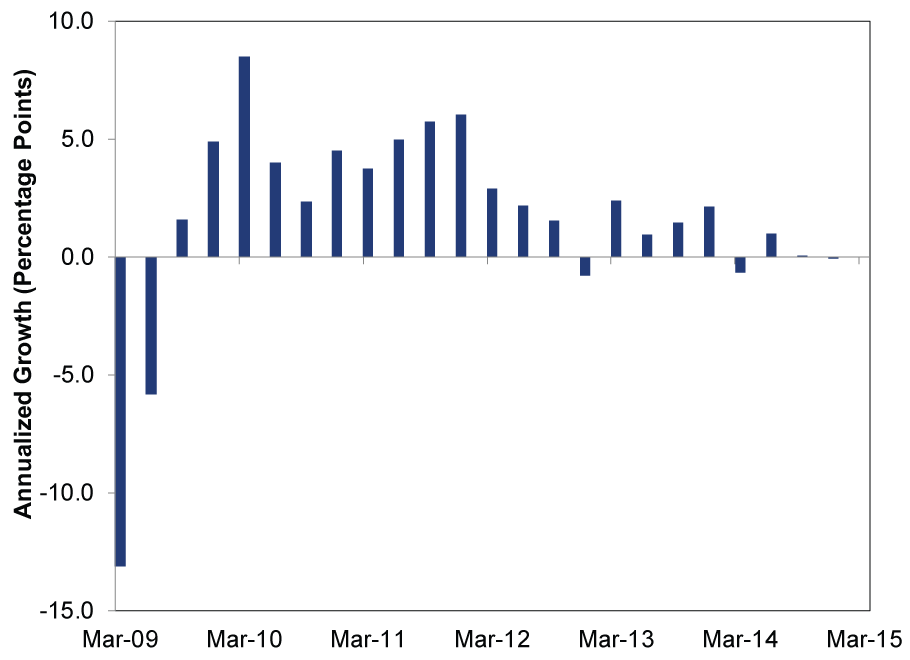

Russia has similar issues. Its government is heavily involved in the economy, and domestic consumption faces hot inflationary headwinds. But it is compounded by state revenues' heavy dependency on energy, which funds social spending. In addition, while the major pressure here is commodity price weakness, "President" Vladimir Putin's military adventures in Ukraine-and the resulting Western economic sanctions-don't help either. These factors caused Q1 2015 GDP to fall-continuing recent weakness. (Exhibit 2)

Exhibit 2: Russia GDP Q1 2009- Q4 2014 (Annualized)

Source: Factset, as of 6/1/2015. Q1 2015 year-over-year data show a -1.9% drop, but quarterly data isn't yet available to annualize, hence this chart covers Q1 2011 - Q4 2014.

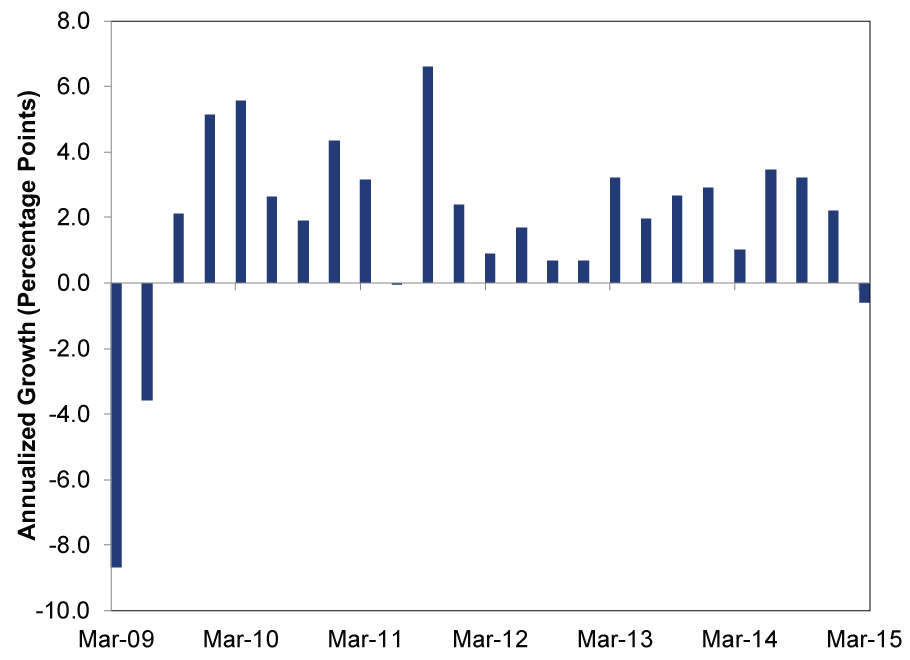

So in Brazil and Russia, weak commodity prices reveal sclerotic economies plagued by longstanding issues. Canada's economy, on the other hand, is in far better shape. And though it is much more natural-resource reliant than the US or UK, it has a robust Financials sector, and Canadian consumers drive growth-creating a more stable environment. Moreover, Canada has a tight trade relationship with its southern neighbor, which happens to be the world's largest economy.[ii] While Canada's Energy sector has detracted from growth in four of the last five quarters, Q1's -0.6% annualized growth was the first time GDP shrank.

Exhibit 3: Canada GDP Q1 2009- Q1 2015 (Annualized)

Source: Factset, as of 6/1/2015.

Low commodity prices create losers in resource-reliant nations, but they create winners elsewhere-like the US, UK and eurozone. Low commodity prices likely help consumers and businesses in these regions, lowering energy and raw materials costs.

To us, that Q1 headline growth was negative in several high-profile nations just doesn't tell you real much about the world economy's prospects ahead. You must drill down into the data, and assess what's behind headline weakness.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today