Personal Wealth Management / Market Analysis

Not So Sterling Silver

Silver’s on a tear, but history suggests it’s both a poor inflation hedge and long-term investment.

Story Highlights:

- Silver rose again Wednesday, continuing its strong run.

- Folks see silver as a stable store of value and cheaper alternative to gold as a currency hedge.

- Yet history shows silver’s a poor inflation hedge and lackluster long-term investment.

- Silver’s run is fun trivia, but stocks are a better bet for long-term growth investors.

Silver!

Have we caught your interest? Tune into any financial media, and it’s evident silver is the topic du jour. It’s being hailed alternately (or indeed, all at the same time) as an inflation hedge, a stable store of value, and also a “can’t-lose” long-term investment.

First, some facts. Silver’s worth, like any market-traded asset, is determined by a buyer and seller agreeing on a price. But unlike shares of companies, which can adapt to economic conditions and generate shareholder value, silver is a commodity. An object—like pork bellies, only shinier and inedible. Most of its demand comes not from investment, but from industrial uses, photography (waning as digital replaces film), and jewelry and silverware. Long term, its price will likely be driven by these end uses.

As an inflation hedge, historically silver has fallen short. This recent boom has coincided with overall tame inflation. Nor has silver historically proven to be a panacea when inflation was high. Take 1979-1981, when inflation hit double digits. While silver more than tripled in 1979 (largely due to the Hunt brothers’ attempt to corner the market), gains were effectively reversed the next two years. This isn’t how a true inflation hedge should behave.

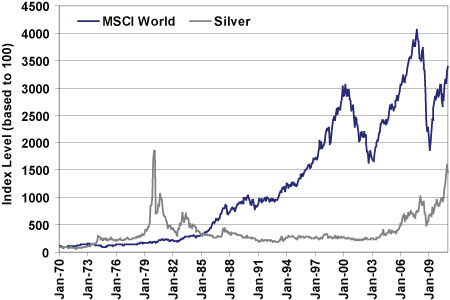

As a long-term investment, Ag also lacks luster. Over the last 40 years, it’s annualized 7.58%, behind global stocks’ 9.07%. It’s lagged, but also been much more volatile—silver’s annual standard deviation is 31.56% versus 15.00% for stocks. And here’s the kicker: Silver is still off its 1979 peak, while global stocks have risen over sevenfold since.[i]

Figure 1: MSCI World Index Versus Silver, 1970 – 2010

Source: Thomson Reuters.

We could go on. Since 1971, silver has posted an annual positive gain just 55% of the time to 78% for stocks. It’s hard to fathom why an asset with a history of lower long-term returns and much higher volatility is considered a stable store of value or viable alternative to stocks.

Silver has had a very impressive recent run—which may, in fact, explain some of its current popularity. And from here, silver could certainly keep rising—just because something rises a lot doesn’t mean it must fall. We’re not in the business of predicting near-term commodity runs. Nor would that be terribly useful, since history teaches us, long term, odds are with stocks. In our view, silver’s recent movements are fun trivia, but they’re not a reason to make either a short- or long-term silver bet.

(For MarketMinder’s views on gold, another commodity.

[i]Sources: Thomson Reuters and Global Financial Data, Inc. As of 12/31/2010.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today