Personal Wealth Management / Politics

Now What?

Did economic reform in Japan just become more likely?

Shinzo Abe is all smiles after his party's latest landslide win. Photo by Bloomberg/Getty Images.

Japan hit the polls Sunday, and the results were a decisive boost ... for the Japan Communist Party, which jumped from eight seats to 21. Oh, and Prime Minister Shinzo Abe's Liberal Democratic Party (LDP) and partner New Komeito maintained their supermajority. This, we are told, gives Abe's "Abenomics" reform agenda a "second wind." Abe vowed to "push ahead" and "give top priority to the economy and bring the warm winds of economic recovery all over the country." And even though Japanese stocks fell Monday, closing at a one-month low, optimists say it's only because global growth jitters just barely, temporarily outweighed investors' election cheer. As ever, we're skeptical. Talk is cheap, and nothing has fundamentally changed on Japan's political scene. Japanese stocks might get a temporary sentiment-driven boost as hopes for change resurge, but it seems highly unlikely Abe can deliver enough to meet investors' high expectations. Longer term, we still think investors are best off outside Japan.

Before the election, Abe's coalition had a 67.7% majority. Post-election, they're up to 68.6%-they gained one seat while the lower house shrunk from 480 seats to 475. So for them, this election confirmed the status quo. For all the talk of the contest being a referendum on Abenomics, Abe's stump speech looked a lot like his first two years in office: lots of general pledges to revive the economy, few (if any) specifics. No proposed legislation to cut agricultural tariffs, complete free trade deals or overhaul the feudal labor code. The Trans-Pacific Partnership-a multination free trade deal-in-progress-which was a cornerstone of his 2012 campaign, barely got a mention. Taxes got some attention, as Abe reiterated plans to delay next October's sales tax hike and bring the corporate tax rate below 30% within a few years, but those are a drop in the bucket. More competitive corporate taxes would be a positive, but they're far off, not yet law, and only a small step to improving Japan's economic structure.

Abe's victory address struck a similar note. Plenty of feel-good economic pledges! But the only specifics were promises to draft a fiscal stimulus package by year-end and be extra persuasive in his efforts to elbow corporate Japan into hiking wages at next year's annual labor negotiations. Some of the stimulus package will likely be aimed at assisting the small businesses and consumers who've been whacked by the weaker yen-the flagship policy of his first two years. Real (inflation-adjusted) wages have overall fallen since he took office, highlighting the inability of fiscal and monetary stimulus alone to create a virtuous cycle of growth, rising wages and rising prices after over 15 years of deflation.

If Abe couldn't pass anything of note with a supermajority and sky-high poll ratings during the last two years, it's hard to see what's so different now. The reforms that are likely necessary to address Japan's structural issues are not very popular with Japanese people, and Abe would need to overcome entrenched interests within his own party and several key supporters, like the agricultural industry and old boys' network of Japan, Inc. If he didn't display much willingness to do unpopular things when his personal approval ratings were well over 70%, we struggle to see how he will act differently now, with his numbers down to 44% and his term as LDP leader expiring next September. He has a huge popularity contest ahead! Some say, "yah, but this election totally strengthens his hand!" To which we say, "yah, but this is Japan, land of 17 prime ministers in 25 years." Those saying the revolving door just slammed shut border on "it's different this time"-the four most dangerous words in investing, as a smart guy once said.

Compounding matters, the economy isn't the only thing on Abe's agenda. It has competition: national defense. Abe's lifelong ambition of restoring Japan's military might has been well-documented by Japanese historians. His grandfather, Nobusuke Kishi[i], was Japan's Prime Minister in the 1950s, and scrapping the constitution's anti-war clause (Article Nine, written in after World War II) was his primary goal-ultimately his political downfall. Abe spent a lot of time with gramps when he was a boy, and the same goal was burned into him at an early age. He championed it in school papers, his early political career and his first term as Prime Minister in 2006-which ended after one year as voters soured on his nationalist agenda. This time around, he has spent significant political capital acting on his inclinations. In July, after being unable to corral enough Parliamentary votes to repeal Article Nine full-stop, Abe's government chose to "reinterpret" the clause in a way that would allow Japan to beef up its military for self-defense purposes. Citizens weren't amused. Protests raged in Tokyo, culminating with one man's tragic self-immolation in one of Japan's busiest pedestrian walkways and another's in a public park. Abe's approval plummeted.

Yet he is undeterred. After the election when discussing boosting the military, he promised: "We'll submit relevant bills at an appropriate time during the special Diet session next year and enact them"-far more specific pledges than the economy received. Article Nine revision was front and center on the LDP's election manifesto-another specific pledge, again drawing sharp contrast with the economy.

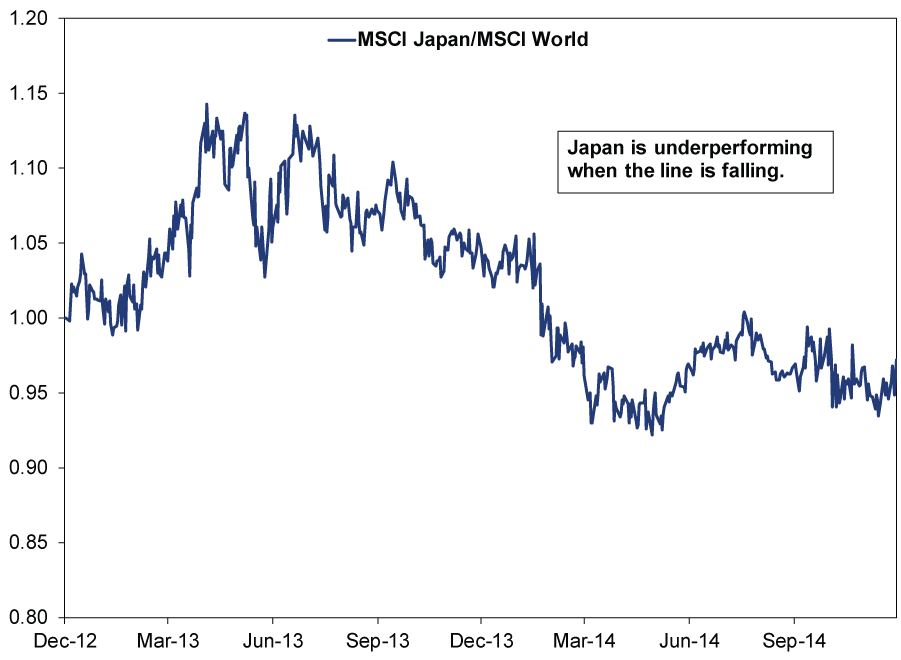

Actions speak louder than words, and it seems increasingly clear Abe is more willing to spend his remaining political capital on nationalist endeavors. They consistently get top billing over the economy, regardless of the costs. Until (and unless) Abe and his government show the same focus and persistence with economic measures, it remains difficult to see the reality of Abenomics living up to the hype. A short-term rally wouldn't surprise at all-the election has sparked a new air of optimism! But the term "suckers' rally" exists for a reason. We'd suggest staying cool. Japanese stocks skyrocketed after the 2012 election, only to lose steam as reality disappointed, and Japan ultimately lagged world stocks during Abe's first two years (Exhibit 1). Any similar surge this time around likely proves similarly short-lived.

Exhibit 1: MSCI Japan Relative Performance Since Abe's Election

Source: FactSet, as of 12/14/2014. MSCI Japan divided by MSCI World, indexed to 1 at 12/14/2012, through 12/12/2014. Returns are in USD and inclusive of net dividends.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] For all you history nerds: Kishi is seen in many parts of Asia as a war criminal, largely tied to his role in overseeing the economy of Japanese-occupied Manchuria in the 1930s. He served several years in prison following the war for this, though the charges against him were eventually dropped.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today