Personal Wealth Management / Market Analysis

Oil and Stocks, Hand in Hand?

How meaningful is oil and stocks' recently high correlation?

Is oil driving stocks? Photo by Seth Joel/Getty Images.

Oil! Got your attention? Headlines are blaring about an alleged link between oil and stock prices, with several noting a near-perfect correlation over the last few weeks-and saying high correlation is common during recessions or periods of "financial stress." One prominent article pronounced the correlation over the last month to be the highest since 1990. Many take the link one step further, warning cheap oil is about to cause a recession. Texas jobless claims are now considered a key national indicator. But we've crunched the numbers, and frankly, we don't get the hype. Oil's recent tight relationship with stocks is an interesting observation, but its predictive powers are about nil. And fundamentally speaking, oil's economic impact, for good or ill, just isn't big enough to move the needle in the US or globally.

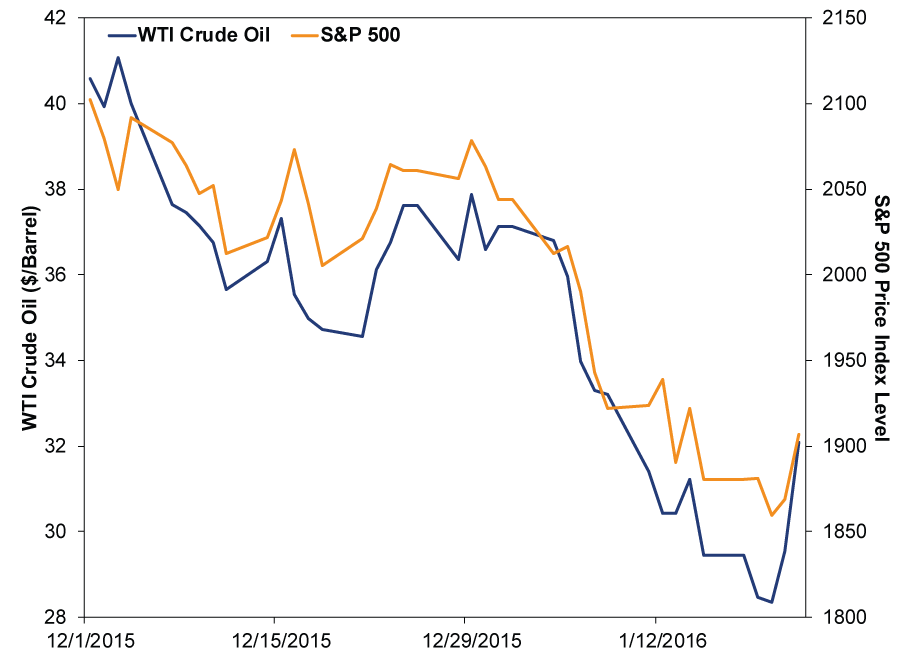

Exhibit 1 shows why everyone is very excited about oil.

Exhibit 1: WTI Crude and S&P 500, 12/1/2015 - 1/22/2016

Source: FactSet, as of 1/25/2016. S&P 500 Price Index and WTI Crude Oil Price, 12/1/2015 - 1/22/2016.

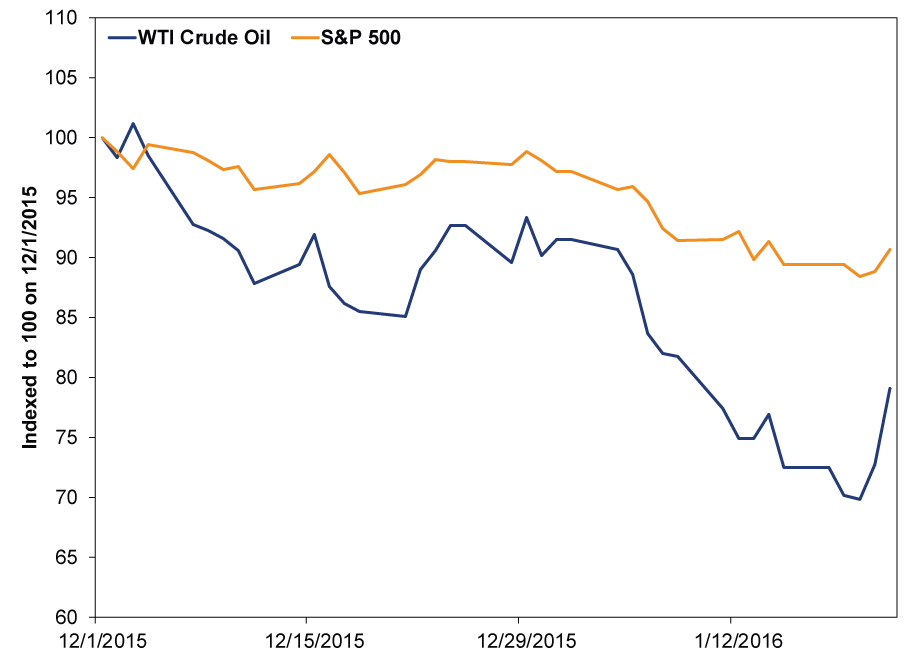

Yes, we manipulated the y-axes to make these look more alike, in magnitude, than they really are. That's what much of the media coverage did-a time-honored trick to "lie with statistics" to whip up a frenzy, as the brilliant Darrell Huff explained in his classic book titled, well, How to Lie With Statistics. If you index each series to 100 in order to show the cumulative percentage change in each, they don't look so striking.

Exhibit 2: A Less Salacious Version of Exhibit 1

Source: FactSet, as of 1/25/2016. S&P 500 Price Index and WTI Crude Oil Price, 12/1/2015 - 1/22/2016. Indexed to 100 on 12/1/2015.

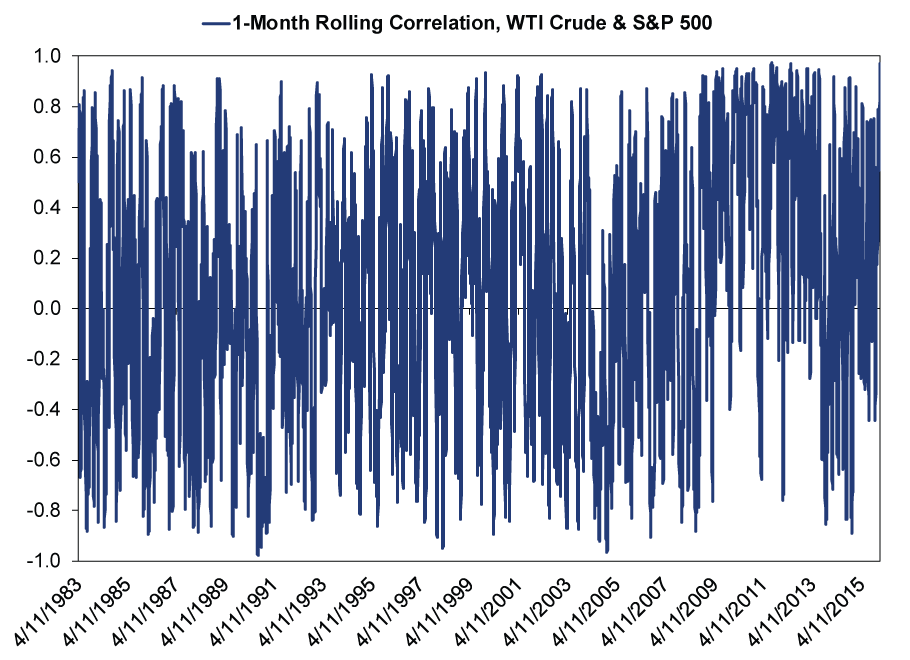

The correlation isn't so striking, either. Yes, over the last month, it's about 0.97, which is about as close to perfect correlation (1) as you can get. But this isn't exactly a unique development. Nor is it especially telling. Exhibit 3 shows oil and stocks' rolling one-month correlation since April 1983, the longest daily dataset we could build. It is perhaps the noisiest chart in the history of MarketMinder, and perhaps the most meaningless.

Exhibit 3: A Meaningless Chart

Source: FactSet, as of 1/25/2016. Rolling 1-month correlation between WTI Crude Oil and the S&P 500 Price Index, 4/11/1983 - 1/22/2016.

Yes, we've seen similarly high correlations during bear and bull markets, recessions and expansions alike. By our calculations, the correlation was a smidge higher in 2011 and 2012-no recession, no bear market.[i] We can only presume it gets hype now because it fits the narrative that oil prices are a key economic driver.

Yet this is a deeply flawed narrative. For broad, diverse economies like the US, cheap oil is neither a huge tailwind nor an oppressive headwind. It is just a thing that creates winners and losers. The same is true when you tally up the entire world. Cheap oil hurts Energy firms, oil transporters (who lose business as cheap prices discourage production) and nations whose GDP and state revenues depend heavily on oil exports (e.g., Brazil, Russia and the Middle Eastern petrostates). Yet cheap oil helps retailers (who often benefit when consumers spend less on gasoline), energy-intensive manufacturers and any firm trying to ship goods. In the US and Europe, the winners outweigh the losers, and the economy usually receives a net benefit.

Oil's share of the US economy is small. Currently, the Energy sector is about 6.5% of S&P 500 market cap. (In June 2014, when oil began tumbling in earnest, it was about 10.9% of the index-larger than today, but still only the fifth biggest sector.) In Q3 2015, Energy contributed less than 5% of total S&P 500 earnings. (In Q2 2014, it contributed 10.8%, the fourth-largest sector.) Excluding Energy, S&P 500 earnings are still growing. Many fear distressed loans to the Energy sector endanger bank balance sheets, but the four biggest banks' Energy exposure ranges from 1.9% to 3.5% of total loans. Certain regional banks are more vulnerable, but even their exposure is around 5% to 10%.

More broadly, in 2014, oil and gas extraction comprised just 1.7% of GDP.[ii] Its support industries were just 0.4% of GDP. To put oil in perspective, it is about half the size of our construction industry, less than one-fifth as big as manufacturing, and approximately 0.025 times the size of the service sector. And while jobs are a late-lagging economic indicator, it's worth noting oil and gas extraction accounts for just 0.1% of all US jobs. Any way you slice the industry, it is small.

We have two hypotheses on why headlines are so hung up on oil anyway. One, when markets are volatile, human nature makes us hunt for a cause-we think understanding can bring comfort. Being able to say "oh, it's because of oil" brings that understanding and, for some folks, something to hope for: oil rebounding so stocks can rebound, too. We get the appeal, but the harsh truth is that this is a behavioral error, not sound analysis.

Two, rewind a year ago, and pundits near-universally agreed that cheap oil would be ginormous, consumer-boosting stimulus. Yet we haven't exactly had rip-roaring growth in the interim, and now they're re-evaluating. But the oil-as-consumer-stimulus narrative wasn't ever really right. As we explained at the time, spending on gasoline is part of total consumer spending. When oil and gas prices fall, we spend less at the pump. Even if we spend every last penny saved on gas someplace else, the impact is only zero sum. But many folks don't spend every last penny saved on gas. They save it or repay debt instead. Don't get us wrong, we like paying less to fill up, but the primary driver of consumer spending is disposable income. Gas prices aren't part of that equation.

Finally, we'd be remiss if we didn't address the China angle. Some argue cheap oil stems not just from a massive global supply glut, but from falling Chinese demand-another iteration of Chinese hard landing fears. The primary evidence here is China's falling imports. Yet those import tallies are skewed by falling prices. Measured in volume terms, which removes the skew, China's oil imports are soaring. They hit a record-high 335.5 million barrels last year, rising 8.8% from 2014. China-watchers expect them to slow this year, but still grow 6%. Chinese oil demand, like Chinese economic growth, is fine. The supply glut just swamps it.

Sensational ghost stories like the oil-stock two-step are normal in corrections. They're part of the fear surge. It can make corrections that much more uncomfortable, which makes it harder to stay disciplined. But corrections often end as suddenly as they begin. Longer-term, fundamentals still look strong, and soon enough we expect the oil-stocks-eek hype to be a distant memory.

[i] The "highest correlation since 1990" claim used slightly different methodology, using 20 trading days to approximate one month-a bit of an undershot. We used 23, which is the exact number of trading days from December 23 through January 22. Considering there are about 252 trading days in the year, 21 days would also be a fair approximation of one month. This all goes to show just how arbitrary this observation is.

[ii] Source: Bureau of Economic Analysis, as of 1/25/2016. Also, we short-handed this a little bit. It's actually the percentage of gross value added, which is equivalent to GDP. But while GDP breaks down total expenditures, gross value added breaks down industry output.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Bourse : pourquoi l’impact de la guerre en Iran sera moins important que prévu – par Ken Fisher2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 4/1/2026

New to Fisher? Call Us.

Contact Us Today