Personal Wealth Management / Market Analysis

Income and Wealth Distribution: Overlooked Basics

Our guest columnist provides an in-depth look at income inequality.

(Editors' Note: Income inequality remains a hot topic, and many wonder how efforts to combat it might impact the economy and markets. We've written occasionally on why such efforts would be a solution in search of a problem: Most studies on income distribution fail to account for demographics, taxes and other mitigating factors. Our guest columnist, Monte Stern, has conducted significant research on this topic, and we think his insightful findings present an unusual and fascinating way to think about income distribution-a view you typically won't get from most major outlets, which we've found forsake nuance for sensationalism and soundbites.

For all the bluster in Washington and on the campaign trail, as you'll see from Mr. Stern's analysis, very little needs to be done about income distribution from an economic perspective. Hence, that our gridlocked government is unlikely to advance legislation targeting this issue any time soon is actually quite ok for markets. Yet governments of all political stripes have a long history of advancing popular legislation, regardless of the actual economics underpinning it. (See the Tariff Act of 1930, for just one famous example.) If every politician had access to universally correct economic thinking, it still wouldn't mean they would act on it-an important reason why we believe politics can be a key driver for markets.

As always, MarketMinder endorses no political views and favors no political party. We don't believe you can analyze markets and economics through a biased lens. The views below are the opinion of the author, not Fisher Investments or the MarketMinder editorial staff. We simply enjoyed the analysis and thought you would, too.)

Updated on 11/3/2015.

I wrote two papers on the subject of income inequality in the early 1970s, when I was a student of economics at Stanford University. One of my professors encouraged me to publish the second of the two, but I never did. At the encouragement of a good friend, I picked up my prior work where I left off and have pushed it much further given the comparative wealth of data we have today and the vastly superior ability to process data that the computer revolution has made possible. So here it is.

As Ken Fisher observes, as a general principle, the way a matter is framed is often problematic: "When we experience problems (opportunities) presented or framed one way, we cannot see a solution; but when the problem is framed another way, we see the solution clearly and quickly."[i] I seek to illustrate this same principle in relation to income and wealth distribution.

The thrust of much, if not most, of the popular public discussion about income and wealth distribution is framed around gross statistics of percentage shares of the total pie going to different quantiles of households. The argument tends to go like this: X has this percentage. Y has that percentage. That's obviously unfair on its face. End of discussion. The gross statistics show more inequality than years ago and more in America than in other countries. That obviously calls for more aggressive government redistribution. End of discussion.

In my opinion, framing the analysis solely, or almost solely, on the basis of the gross statistics tends to mask basic facts and dynamics that I suspect would lead many who currently believe things have gotten so much worse as to require more aggressive government redistribution to reconsider their initial impression. As expressed by professor and economist Thomas Lemieux, in a book chapter entitled "What Do We Really Know About Changes in Wage Inequality," published in 2010 by the National Bureau of Economic Research[ii], "...what is often presented as the basic inequality trends ends up mixing up composition effects and true underlying changes in the wage structure." Further, as expressed in a 2007 US Treasury study[iii], "While many studies have documented the long-term trend of increasing income inequality in the U.S. economy, there has been less focus on the dynamism of the U.S. economy and the opportunity for upward mobility. Comparisons of snapshots of the income distribution at points in time miss this important dimension and can sometimes be misleading."

In this article, I will review the distribution of income and wealth in the US from three basic perspectives that tend to be otherwise overlooked if the subject is framed primarily on the basis of the gross statistics: a) quantity and quality of work effort; b) quantity and quality of capital accumulation; and c) upward and downward mobility.

QUANTITY OF WORK EFFORT

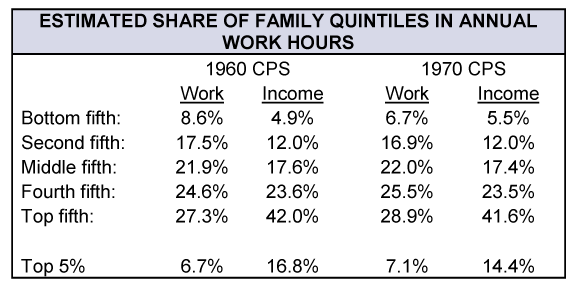

To illustrate, in my college papers, the potential significance of relating work effort to incomes rewarded in the marketplace, I estimated the percentage share of family quintiles in annual work hours. Due to inadequate data, to do so, I had to make some assumptions. In particular, I assumed full-time workers averaged 45 hours per week, part-time workers averaged 20 hours, and secondary earners worked 50% as many hours as primary earners. Using these assumptions, I interpolated and extrapolated from the extant data to produce these two estimated profiles of income and work distributions for families in 1960 and 1970:

Exhibit 1: Estimated Share of Family Quintiles in Annual Work Hours

Most economists at the time opined that the distribution of income did not become more equal during the postwar era. The tables, above, however, clearly suggested increased equality in the sense that the distribution of work effort came closer to matching the actual income distribution.

To be sure, some economists at the time factored into their analysis various underlying demographics, much as Mark Perry, the economist Ken Fisher mentions in his latest book, Beat the Crowd, does today. A few consequently contended that, contrary to popular opinion, the distribution of income did improve during the postwar era. By the way, Mark Perry annually posts a commendable demographic explanation of income inequality. The most recent can be found here: https://www.aei.org/publication/explaining-income-inequality-demographics/

In my experience in the 1970s, I found that when I mentioned demographic observations implying a changing distribution of work effort (changes in the mean number of earners per family, percent of family heads working full-time year round, and the percent of family heads not working), more often than not (and particularly outside academic circles), I lost my audience and my effort to convey the main point failed. The apparent need to distill the net effect of these demographics down into one simple, quick, easily understood presentation motivated the creation of the tables above. Only then did I begin to see the lights go on and hear enthusiastic responses to my work!

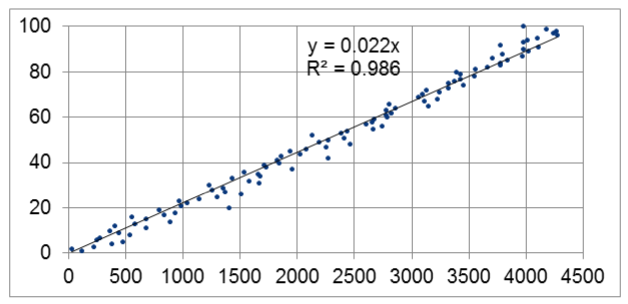

Today, we can download public-use microdata for the Census Bureau's Current Population Survey Annual Social and Economic Supplement (IPUMS-CPS, University of Minnesota, www.ipums.org) and readily prepare visually revealing graphs. Fortunately, these data include, since 1976, survey responses on usual hours worked per week last year and weeks worked last year as well as income figures. From these data, I calculated an estimate of total annual hours worked (hours per week X weeks worked) by all household members and then sorted that data into 100 percentiles by total income for the year 2011[iv]. Exhibit 2 shows the relationship between income percentile (1 being the lowest income percentile; 100 being the highest) and work effort:

Exhibit 2: 2011 Household Total Income Percentile (Y-axis) vs. Annual Hours Worked by the Household

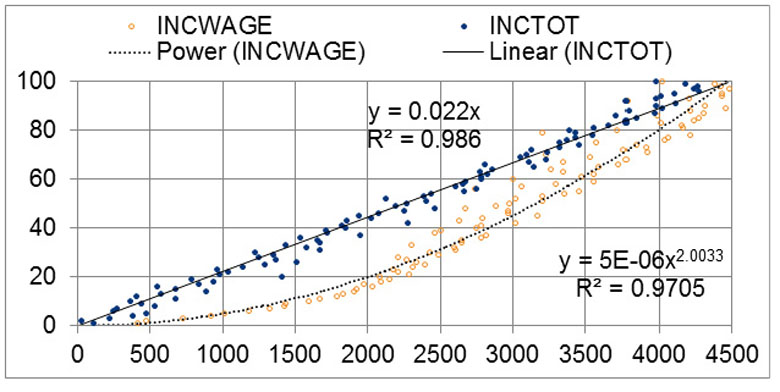

Household income ranking in 2011 was nearly perfectly correlated with the number of annual hours worked by all members of the household. In a household whose members worked 4,484 or so hours that year, the household income tended to be in the top 1% of the country. In a household whose members worked 2,242 or so hours that year, the household income tended to be in the middle, i.e., the 50th percentile. In a household whose members worked 44.84 or so hours that year, the household income tended to be in the bottom 1%. In other words, each additional 44.84 hours of work corresponds, on average, to one additional percentile in household total income rank. An e-mail sent in by an astute reader of a prior version of this article pointed out that Exhibit 1 clearly shows both that the top worked more and the bottom got less pay per unit of work, but the latter point gets lost in Exhibit 2. He suggested this point may need further comment to make it easier to digest Exhibit 2. To be sure, pay rates are not equal in our society. As will be discussed briefly later in this article (and as is recognized in a famous wage model known as the Mincer wage equation), differences in education and age are among the various factors that correlate with wages and, in turn, income ranking. Exhibit 2, however, looks at total income, not just wage and salary income (75.8% of total income) and, as such, reflects a variety of ways, both public and private, by which other income is systematically allocated according to circumstance and need-namely, in descending order of magnitude in 2011: Social Security income, retirement income, unemployment benefits, educational assistance, supplemental security income, veteran's benefits, survivor's benefits, child support, disability benefits, regular financial assistance from friends or family, worker's compensation, welfare and alimony. Exhibit 2b illustrates the difference it makes when looking at total income rather than wage and salary income, alone.

Exhibit 2b: Same as Exhibit 2, With Wage and Salary income, Alone (INCWAGE) Added

A November 2014 report by the Congressional Budget Office (CBO) discusses the redistributive effect of the public sector portion of these other forms of income: "Government transfers ... lessen income inequality because ... payments from government transfer programs generally decline as a share of income as income rises. Between 1979 and 2011, government transfers reduced inequality to a greater extent than federal taxes, based on a standard measure of inequality known as the Gini index." [v]

Keeping in mind that the foregoing charts are based on pre-tax income, consider that there is a further redistribution of income-not reflected on these two charts-in the form of progressive federal taxes. According to the same November 2014 CBO report (p. 2), in the same year, 2011, the tax liability of the bottom quintile for federal taxes was 2.0% percent of income, 7.1% for the second quintile, 11.1% for the middle quintile, 15.2% for the fourth quintile and 23.4% for the top quintile. In other words, the bottom quintile's share of the total federal tax liability was 0.6%, the second quintile's share was 3.8%, the middle quintile's share was 8.9%, the fourth quintile's share was 17.7%, and the top quintile's share was 68.9% of the total federal tax liability. I suspect, when viewing the issue framed in light of the discussion above, many readers who previously believed, based primarily on the gross pre-tax income statistics, that more aggressive government redistribution is urgently needed may begin to see the issue in a new and different light.

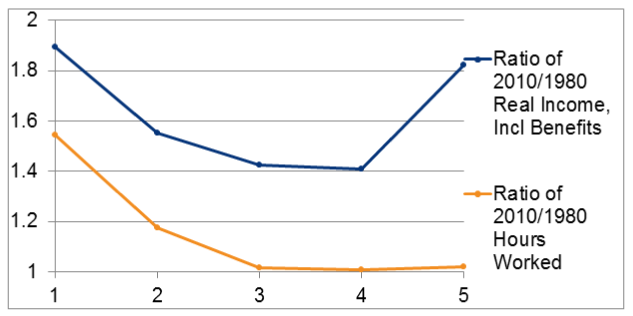

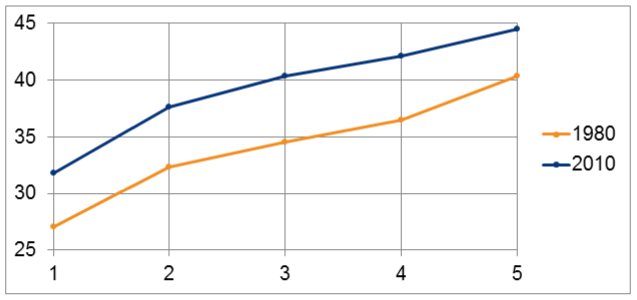

As to trends, by delving deeper into the relationship between work effort and income rewarded in the marketplace, a case can be made that the distribution of income has grown more equal, in terms of the two bottom quintiles, over the past 30 years. For purposes of analyzing the trend in the labor market, I abandon the household unit and household total income in favor of examining individual work effort and individual wage and salary income rewarded in the marketplace, which seems more appropriate. I also limit the analysis to private sector workers, along with other restrictions reported to be standard in the literature[vi]. The resulting picture of the 30 year trend is shown in Exhibit 3:

Exhibit 3: Ratio (Y-axis) of 2010 to 1980 Real Income[vii] and Hours Worked by Income Quintiles (X-axis)

Between 1980 and 2010, the bottom (denoted as 1 on the horizontal axis) of the five quintiles of individual wage and salary earners, ranked by wage and salary income, experienced the greatest percentage gains in both annual hours worked (54%) and in real annual wage and salary income (89%). The next quintile up (denoted as 2 on the horizontal axis) experienced the second-greatest percentage gains, among all quintiles, in annual hours worked (17%) and the third-greatest percentage gains, among all quintiles, in real annual wage and salary income (55%).

QUALITY OF WORK EFFORT

While the top quintile experienced a disproportionate gain in real wage and salary income relative to hours worked, it also experienced by far the greatest percentage gain in years of education than the other quintiles (18.5% increase vs. 6.8% for the bottom two quintiles combined), suggesting a relative qualitative gain in productive merit in terms of knowledge, rather than in hours worked, in the top quintile. The average years of education for the top income quintile in 2010 was 15.6 years, up from 13.2 years in 1980[viii]. As such the top income quintile in 2010 was the only income quintile in either year with an average number of years of education closer to a college degree (16 years) than to a high school degree (12 years).

Lemieux concludes, on p. 50 of the NBER book chapter mentioned earlier[ix], by noting that, "In terms of potential for future research, arguably the most important fact documented in this chapter and in related work (Lemieux 2006b, Goldin and Katz 2007) is the dramatic importance of education in changes in wage inequality."

QUANTITY OF CAPITAL ACCUMULATION: SAVINGS RATES

In free societies, each individual is allowed to make their own decision on how much to save vs. consume out of their income each year. If the savings rate tends to increase with income, then the distribution of wealth that evolves will, in all likelihood, be more unequal than the distribution of income, itself. As Dynan (Federal Reserve Board), Skinner (Dartmouth College and the National Bureau of Economic Research) and Zeldes (Columbia University and the National Bureau of Economic Research) point out on p. 3 in their article, "Do the Rich Save More?," published in Sept 2000 by the National Bureau of Economic Research[x], Nov 2000 by the Federal Reserve[xi] and in 2004 by the University of Chicago[xii], "...the question of whether higher income households save at higher rates than lower income households has important implications for the distribution of wealth..."

In this section and the next, I numerically probe the effect of the savings rate increasing with income quantile on the distribution of wealth. For purposes of emphasizing the equitable implications, I model the distribution of wealth that would evolve in a hypothetical perfectly egalitarian society where hourly wages are exactly equal and everyone has equal opportunity to increase their income not at the expense of anyone else, nor by disproportionate influence, but simply through free choice of how to allocate their time between hours spent working for compensation and hours spent otherwise.

In the first two pages of their article, Dynan, Skinner and Zeldes mention there was an outpouring of research in the 1950s and the 1960s on the question of whether the rich save more, with earlier empirical work favoring the "yes" view but with sufficient work favoring the opposite view to create reasonable doubt. From their ensuing comments on p. 4, it appears that researchers back then generally agreed the answer is yes with respect to current income, but Milton Friedman in 1957 contended the answer is no when looking at lifetime incomes. While some subsequent studies supported Friedman's view, others did not. Given the importance of the question and a wide variety of newer data sources yielding a much richer picture of empirical patterns of savings behavior, Dynan, Skinner, and Zeldes decided to revisit the question. Here's their summary of their findings, from p. 3 of their 2000 article:

"We find, first, like previous researchers, a strong positive relationship between current income and savings rates across all income groups, including the very highest income categories. Second, and more important, we continue to find a positive correlation when we use proxies for permanent income such as education, lagged and future earnings, the value of vehicles purchased, and food consumption. Estimated savings range from less than 5 percent for the bottom quintile of the income distribution to more than 40 percent of income for the top 5 percent. The positive relationship is more pronounced when we include imputed Social Security saving and pension contributions. Even among the elderly, saving rates may rise with income. In sum, our results suggest strongly that the rich do save more, whether the rich are defined to be the top 20 percent of the income distribution (following the Department of Treasury - Pines, 1997), or the top 1 percent. And, more broadly, we find that savings rates increase across the entire income distribution."

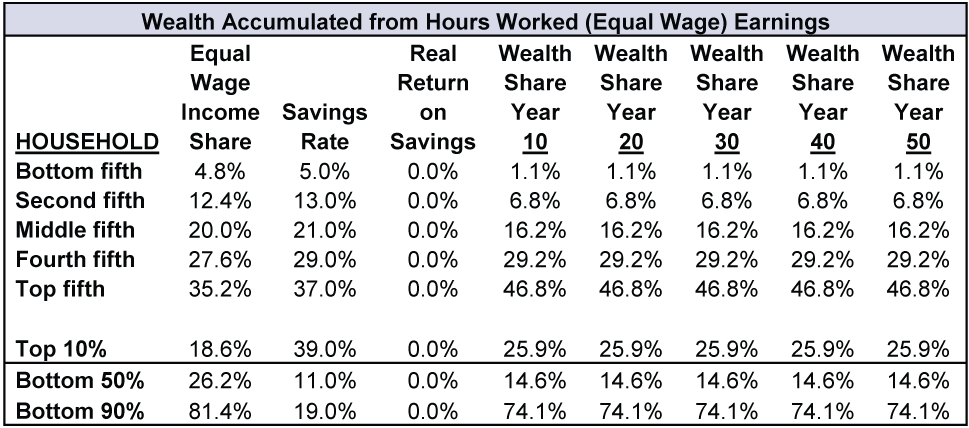

For numerical modeling purposes, based on their summary, I assume savings rates are 5% for the bottom quintile and rise linearly by quantile, topping out at 40% for the top 5 percent. I use my compilation of the ipums.org data for total hours worked by households in 1986 because, by and large, the Dynan, Skinner, and Zeldes empirical analysis was done on household data for that year and years centered on it. I assume, for simplicity, everybody in this hypothetical economy receives the same return on their savings (any rate of return, including 0, will do as it does not affect the results). Further, I assume we start with a blank slate, i.e., no one has any wealth at the start of this exercise. Exhibit 4 shows my calculations of the distribution of wealth as it evolves over time:

Exhibit 4: Model of the Evolution of Wealth Distribution if Wages and Returns Are Equal

As you can see, the distribution of wealth is more unequal than the distribution of income due simply to the differences in savings rates.

QUALITY OF CAPITAL ACCUMULATION: INVESTMENT MIX

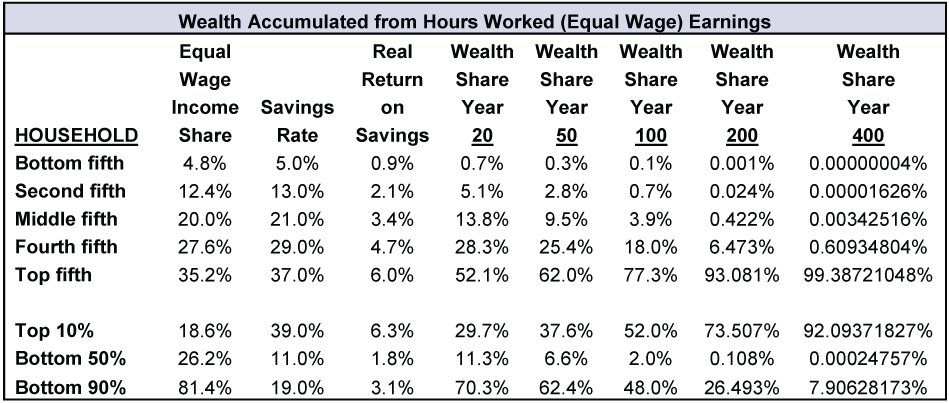

In his best-selling book, Capital in the Twenty-First Century, professor and economist Thomas Piketty suggests on p. 26 that investment returns likely will tend to be higher for those with greater wealth.[xiii] While I don't have quantile-based data, I agree to the extent it seems reasonably likely people with larger savings likely feel more comfortable taking greater risk (e.g., investing a higher proportion in stocks) in the hope of better long-term returns than those with less savings. Evidence from the Federal Reserve Board's Survey of Consumer Finances, though not precisely on point (it gives percentages of families in three quantile groups who own publicly traded stock, rather than percentage of portfolios allocated to stocks), appears consistent with this premise[xiv]. Assuming the foregoing, then, mathematically, the distribution of wealth will grow more unequal over time, all else equal ("ceteris paribus").

To illustrate the foregoing, and for lack of better data, I develop a hypothetical evolution of the distribution of wealth by starting with data on the geometric average annual rate of returns for 3-month Treasury bills, 10-year Treasury bonds and the S&P500 from 1928-2014 as published by Prof. Damadoran on his website[xv]. These annual returns range from 3.49% for 3-month Treasury bills to 9.6% for the S&P500, which, by my calculations, translates into real returns after inflation of 0.38% for 3-month Treasury bills to 6.49% for the S&P 500. I assumed the bottom 5%, on average, invest their savings wholly in 3-month Treasury bills or equivalents; the top 5%, on average, invest their savings wholly in the S&P500 or equivalents; and the brackets in between invest in a mixture yielding returns that increase linearly as one moves up the quantiles. Exhibit 5 shows my result:

Exhibit 5: Model of the Evolution of Wealth Distribution, Equal Wages, Returns Vary by Investment Mix

Even though the hypothetical distributions of wealth shown in Exhibits 4 (equal returns to savings) and 5 (unequal returns to savings) evolve from a perfectly egalitarian society, both distributions, in terms of the gross statistics, show up as more unequal than what Piketty, on p. 258 of his book, defines as a reasonable description of a "mildly" inegalitarian distribution, i.e., one in which the poorest half own 20% - 25% of total wealth.

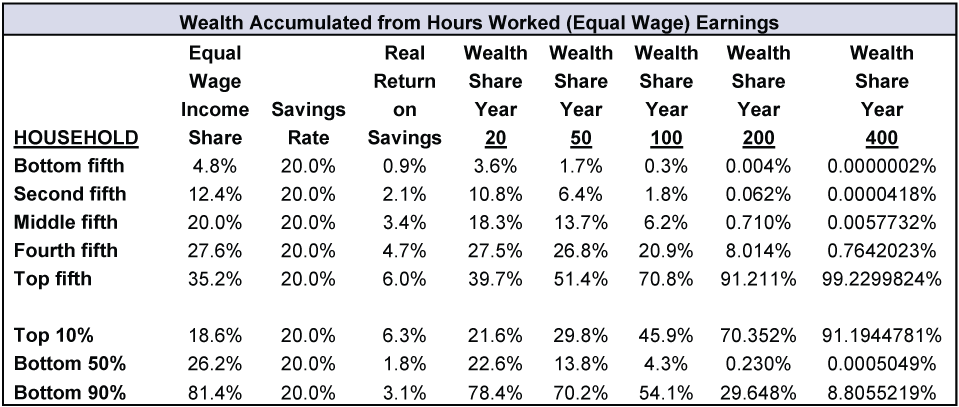

Further, over the span of 400 years (approximately the time elapsed since the founding of America's first permanent English colony in 1607 at Jamestown, Virginia), this hypothetical distribution of wealth evolves to even greater wealth inequality than we see in the US today (top 10% owned about 75% in 2013[xvi]). Moreover, this conclusion stands even if I substitute a uniform savings rate schedule that does not vary at all by household income quintile, as in Exhibit 6:

Exhibit 6: Model of the Evolution of Wealth Distribution, Equal Wages & Savings Rates, Returns Vary

This hypothetical analysis is obviously incomplete: Not only does it lack actual data on returns to savings by income quintiles, it uses before-tax income and before-tax returns on savings, and it does not attempt to factor in the important asset of home ownership, upwards and downwards income mobility over time, estate taxes, nor higher potential returns on investing in one's own start-up business. Nonetheless, this analysis raises the question: Why is the current wealth distribution not more unequal today?

UPWARD AND DOWNWARD MOBILITY

Part of the answer to the foregoing question may lie in the fact there is upward and downward mobility. In supplement to Ken Fisher's comments and Mark Perry's comments on this subject, I include some self-explanatory additional references, as follows:

- A Treasury study published 11/13/2007 found, "Roughly half of all taxpayers who began in the bottom quintile in 1996 moved up to a higher income group by 2005...The composition of the very top income groups changes dramatically over time. Less than half (40 percent or 43 percent depending on the measure) of those in the top 1 percent in 1996 were still in the top 1 percent in 2005. Only about 25 percent of the individuals in the top 1/100th percent in 1996 remained in top 1/100th percent in 2005...Overall, the table shows that upward absolute income mobility increased in the most recent decade as compared to the previous decade."

- "The proportion of households in the bottom quintile in 2004 that moved up to a higher quintile in 2007 (30.9 percent) was not statistically different from the proportion of households in the top quintile in 2004 that moved to a lower quintile in 2007 (32.2 percent)" (in other words, the transition rate out of the bottom quintile accelerated from 4% per year in the prior decade to about 7% per year over this 4 year period)."

- "A study by the IRS of the four hundred tax returns each year with the highest incomes finds amazing mobility in and out of this group over time (1992-2008)...The IRS found that only four of the four hundred (1 percent) made the cut every year." Who's the Fairest of Them All? The Truth About Opportunity, Taxes, and Wealth in America, Stephen Moore, 2012, Encounter Books (New York), p. 48. See also primary source, Table 4, at: https://www.irs.gov/pub/irs-soi/08intop400.pdf. See also Mark Perry's comments on this IRS study:

- "According to 'The Myth of Dynastic Wealth,' published in 2015 by the Cato Institute, with respect to the Forbes list of the 400 richest Americans, only 34 of the original 400 in 1982 remained on the list in 2014, while only 24 names appeared on all 33 lists."

Finally, closely related to the concept of mobility and also an important consideration in econometric models of wage determination is the observed pattern suggesting that, in addition to years of education, age is a key determinant of current income:

Exhibit 7: Age (Y-axis) by Wage and Salary Income Quintile (X-axis: 1=bottom quintile; 5 = top)[xvii]

For interesting, though (in my opinion) heavy, reading on econometric models of wage determination, founded in economic theory, I refer you to references that come up at google.com when searching for "James Heckman wage model." James Heckman is an economist and Nobel Laureate. While graphs of models proposed by Heckman and his collaborators suggest their models fit the data impressively well, as far as I can tell, the final word on that subject isn't in yet.

CONCLUSION

I set out to make one main point: Framing the analysis solely, or almost solely, on the basis of the gross statistics tends to mask basic facts and dynamics that I suspect would lead many who currently believe things have gotten so much worse as to require more aggressive government redistribution to reconsider their initial impression. If I have succeeded in making that one point, or if you wish to provide any feedback, I would like to hear from you and invite you to send your feedback to: overlooked.basics@gmail.com. Your comments will help me gauge whether my analysis requires further vetting and also whether there is sufficient interest to merit submitting this article, or a revised version, to other venues for potentially wider publication.

[i] https://www.cxoadvisory.com/4806/individual-gurus/ken-fisher-on-market-analysis/ (emphasis in original)

[ii] "What Do We Really Know About Changes in Wage Inequality?" Thomas Lemieux, Labor in the New Economy, edited by Katharine G. Abraham, James R. Spletzer and Michael Harper. University of Chicago Press, October 2010. Page 19. https://www.nber.org/chapters/c10812.pdf

[iii] "Income Mobility in the US From 1996 to 2005," Report to the Department of the Treasury, November 13, 2007.

[iv] Data for 2011 compiled from the 2012 file, which contains responses for hours worked "last year."

[v] "The Distribution of Household Income and Federal Taxes, 2011," Congressional Budget Office, November 2014. https://www.cbo.gov/sites/default/files/cbofiles/attachments/49440-Distribution-of-Income-and-Taxes.pdf (See pp. 3-4, which are pp. 7-8 of the pdf)

[vi] "Following most of the literature, I trim extreme values of wages (less than $1 and more than $100 in 1979$) and keep workers aged sixteen to sixty-four with positive potential experience." "What Do We Really Know About Changes in Wage Inequality?" Thomas Lemieux, Labor in the New Economy, edited by Katharine G. Abraham, James R. Spletzer and Michael Harper. University of Chicago Press, October 2010. (p. 5 of pdf) https://www.nber.org/chapters/c10812 (I also throw out data that has been "allocated" or coded as not in universe or missing.)

[vii] For purposes of this figure, real income has been calculated by an adjustment both for inflation as measured by the CPI and for increases over time in the benefits/wages ratio as reported by the Bureau of Labor Statistics. Since the underlying data used in the analysis was released in March of each year, I used the CPI indices as of Sept of the prior year, that being the mid-point of the past year. For Sept, 1979, the CPI was 74.6. For Sept. 2009, the CPI was 215.969. These CPI figures are as reported by Yale Professor Robert J. Shiller, available at www.econ.yale.edu/~shiller/data/ie_data.xls

In 1980, benefits were 15.8% of employment costs. In 2010, benefits were 30.4% of employment costs. These data are reported, respectively, in: https://www.bls.gov/news.release/archives/ecec_06092010.pdf and https://www.bls.gov/opub/mlr/1981/11/art1full.pdf

[viii] For purposes of this analysis, I allocated 24 years of education to those who hold professional degrees. This number is inferred based partly on higher earnings for those with professional degrees vs. doctorates and partly on the observation that medical doctors may spend as much as 8 years in residency training. If I throw out all data samples with professional degrees, the average number of years of education in the top quintile drops slightly from 15.6 years to 15.21 years.

[x] "Do the Rich Save More?" Karen E. Dynan, Jonathan Skinner and Stephen P. Zeldes, National Bureau of Economic Research, September 2000. NBER Working Paper 7906. https://www.nber.org/papers/w7906.pdf

[xi] "Do the Rich Save More?" Karen E. Dynan, Jonathan Skinner and Stephen P. Zeldes, republished by the Federal Reserve in November 2000. https://www.federalreserve.gov/pubs/feds/2000/200052/200052pap.pdf

[xii] "Do the Rich Save More?" Karen E. Dynan, Jonathan Skinner and Stephen P. Zeldes, republished in Journal of Political Economy, 2004, col. 112, no. 2, The University of Chicago. Pages 394 - 444.

[xiii]Capital in the Twenty-First Century, Thomas Piketty, Translated by Arthur Goldhammer, Bellknap Press, April 15, 2014.

[xiv] "Changes in US Family Finances From 2010 to 2013: Evidence From the Survey of Consumer Finances," Jesse Bricker, Lisa J. Dettling, Alice Henriques, Joanne W. Hsu, Kevin B. Moore, John Sabelhaus, Jeffrey Thompson and Richard A. Windle, assisted by Sebastian Devlin-Foltz and Jacob Krimmel. Federal Reserve Bulletin, September 2014, Vol. 100, No. 4.https://www.federalreserve.gov/pubs/bulletin/2014/pdf/scf14.pdf

[xv] "Annual Returns on Stock, T.Bonds and T.Bills: 1928 - Current" https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html

[xvii] Like Exhibit 3, the unit for Exhibit 7 is individual wage and salary earners, rather than the household unit.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Inflation Data, Currency Reset Risks, Commodity Opportunities and More– April 20262026-04-17

-

Market Volatility Anatomy of a (Near-)Correction2026-04-16

-

Market Analysis An Economic Check In on the UK2026-04-16

-

Macro Insights Q1 2026 Executive Summary2026-04-14

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today