Personal Wealth Management / Market Volatility

On Monday's Volatility and the Yuan

The notion of China “weaponizing” the yuan seems a tad overwrought to us.

Global markets continued their slide Monday as the world reacted to the latest salvo in President Trump’s trade tiff with China, leaving the S&P 500 price level -6.0% below its prior high.[i] The US doesn’t export enough to China for officials to retaliate to Trump’s latest tariff announcement (10% on all remaining $300 billion of previously untaxed Chinese imports), so Chinese policymakers got creative: They directed state-owned firms to stop buying US agricultural products and allowed the yuan to fall below seven to the dollar, the lowest level since the financial crisis. Headlines warned of a trade war without end snowballing into a currency war, potentially destabilizing the entire global financial system. We think this is just a bit overwrought. Not only does it ignore some key issues Chinese central bankers have been dealing with, but it ascribes currencies too much power over markets. Volatility could very well continue as sentiment deteriorates, and this pullback may even hit correction territory (i.e., breech -10%), but a bear market (prolonged decline below -20% with fundamental causes) appears as remote as ever.

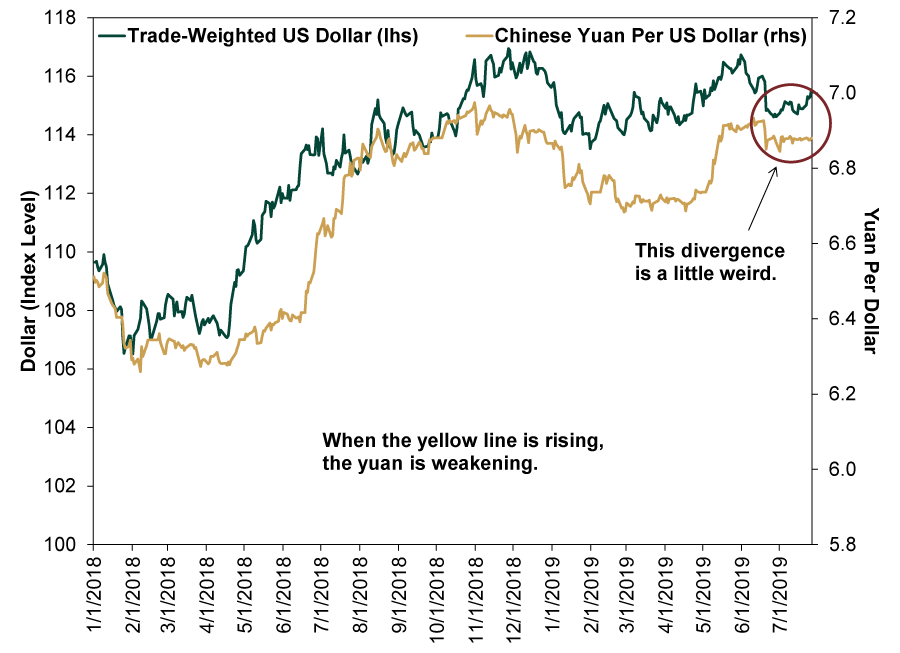

We have seen a lot of talk about China now “weaponizing” the yuan, as if today’s move is only the start in a deeper currency devaluation. Only time will tell whether this turns out to be true, but we have our doubts. While the Trump administration has been jawboning endlessly about Chinese currency manipulation, all indications suggest the People’s Bank of China (PBOC) has been intervening to push the yuan higher in recent months, not lower. Exhibit 1 shows the USD/CNY exchange rate and the Fed’s trade-weighted dollar index since the start of 2018. Note the yuan’s suspiciously flat stretch since mid-June, even as the dollar strengthened against the Fed’s broad currency basket. We don’t know what goes on behind closed doors, but that is a strong indication PBOC officials were intervening to keep the yuan from weakening against the dollar. When officials allow the market more say-so over the yuan’s value, its moves tend to track the dollar index much more closely.

Exhibit 1: The Suspiciously Stable Yuan

Source: FactSet, as of 8/5/2019. Trade-weighted US dollar index (broad) and Chinese yuan per US dollar, 1/1/2018 – 7/26/2019, which is the latest US dollar data available.

So to us, Monday’s move looks mostly like a central bank deciding not to put a floor under its currency for a moment—a market-driven move that plays catch-up with the past month and a half or so. Maybe the data will eventually show the central bank snapping up some foreign currencies to add a bit of deliberate weakness from what the market would have done on its own, but we suspect they didn’t have to help a ton.

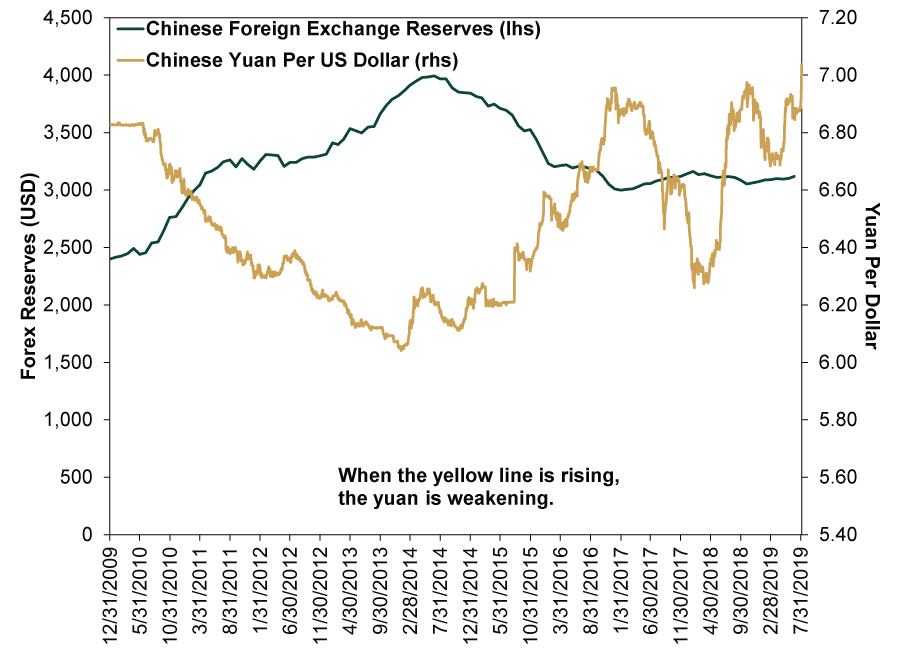

The whole notion of an artificially weak yuan has long struck us as a bit weird. Back in 2015, when the yuan weakened significantly (including a shock devaluation that August), the PBOC burned through about $1 trillion in foreign exchange reserves in an effort to defend the currency—or more simply, to keep it from weakening further. This time around, as the yuan weakened over the past 18 months, they didn’t burn through reserves, but they didn’t amass them either. If there were a deliberate effort to weaken the yuan, we would expect China’s forex reserves to jump.

Exhibit 2: A Brief History of Currency Defense

Source: FactSet, as of 8/5/2019. Chinese foreign exchange reserves (monthly) and Chinese yuan per US dollar (daily), 12/31/2009 – 8/5/2019.

China has logical reasons for not wanting the yuan to tank, which makes us question today’s market speculation that this is only the tip of the iceberg. When the yuan weakened in 2015, capital fled the country as investors feared an economic hard landing. That is a big reason the PBOC had to intervene to support the currency—if they hadn’t, capital flight would have pulled it even further down. Maintaining a stable currency is vital to keeping foreign capital in the country and supporting economic growth. For all the punditry chatter over the alleged benefits of a weaker currency (e.g., cheaper exports and an export-led manufacturing boom), China has long been more interested in beefing up its services sector and enabling consumption to drive growth. With growing consumer demand comes higher imports, which a weaker currency hurts (by making imports more expensive). To say Chinese officials covet a weaker currency is to say they want to hit the rewind button on the past several years’ worth of economic development and reclaim low-end manufacturing from Vietnam. There is just no evidence this is the case.

But there is every indication the government’s primary goal is ensuring economic stability in order to preserve social stability. A stable yuan is key to this effort. China’s government is nothing if not pragmatic. We rather doubt they would risk domestic stability simply to thumb their nose at President Trump. That is just not the sort of thing a one-party government intent on retaining power does.

China’s 2015 currency woes did coincide with a global stock market correction, but that isn’t an indication a weak yuan or strong dollar is inherently bad for stocks. Overall, market history shows currency swings in general have little to no relationship with stock returns. US and global stocks have done fine alongside a weak and strong dollar alike. To the extent China’s currency volatility factored into 2015’s correction, we think it had more to do with the broader fear of a Chinese economic hard landing, which the currency move was just one symptom of.

So overall, it looks to us like markets are making a tad too much of one day’s worth of currency volatility and some cryptic jabs from the PBOC, which called the yuan’s move a product of “unilateralism, trade protectionism and tariff expectations imposed on China” and pledging to keep the yuan at a “reasonable and balanced level.” Yet sentiment doesn’t always catch on to reality quickly, especially when tough words and fearful headlines are involved, so stocks’ freakout could continue. Short-term volatility is impossible to predict. Yet fundamentally, we don’t see any huge changes. As discussed last week, tariffs are still too tiny to wreck the global economy, the US or China. Currency wars are still abstract myths, not economic drivers. An actual currency crisis that devastated the world’s second-largest economy could be a global market risk, but again, there is no evidence China is on the cusp of this. So eventually, we think this market storm should blow over, even if the tariff tempest lasts a while longer.

[i] Source: FactSet, as of 8/5/2019. S&P 500 price return, 7/25/2019 – 8/5/2019.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today