Personal Wealth Management / Economics

One Quadrillion and Counting

What should investors make of the news Japan’s gross publicdebt passed one quadrillion yen in Q2?

As Dr. Evil might say, Japan’s gross public debt is one million billion yen. Photo by Hulton Archive/Getty Images.

One quadrillion. That’s one thousand trillions. One million billions. One billion millions. It’s also, as of June 30, the size of Japan’s total outstanding debt in yen. Or, based on Monday’s preliminary estimate of Q2 output, 206% of GDP. Some suggest this is evidence Japan is in dire need of, um, a sales tax hike. In our view, it underscores how vital structural economic reform is to Japan’s future—without it, Japan’s economy and equity markets likely face a tough road.

First, let’s get one thing clear: Japan doesn’t necessarily have a debt problem. For one, that one quadrillion refers to Japan’s gross public debt. Net public debt, which excludes debt owned by the government and the BOJ, is only about ¥815 trillion, or 166% of GDP. Exclude debt held by state-run banking behemoth Japan Post, too, and the tally falls to about ¥676 trillion, or 142% of GDP (both as of 3/31/2013—the latest available Japan Post data). Still really big, but the cost of servicing it is manageable. Current yields on Japanese Government Bonds (JGBs) range from 0.2% (two-year) to 1.87% (40-year). Per fiscal 2013’s draft budget, debt service will comprise 24% of the budget—the same as in 2000—and total about 4.5% of GDP. Yes, it is far higher as a share of expected tax revenue (about 51.6%), but with demand for JGBs still robust, the government isn’t in danger of missing obligations any time soon. Or, simply, Japan isn’t Greece.

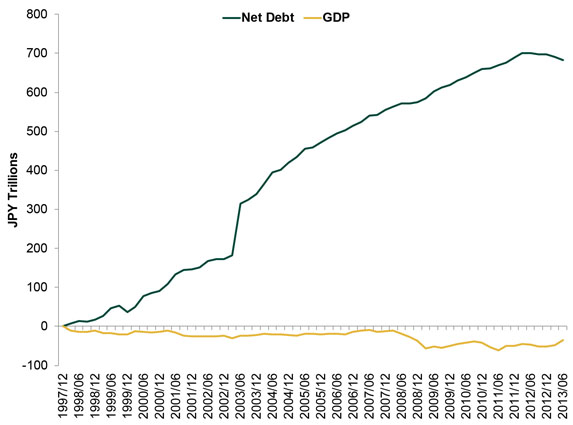

Japan does, however, have long-running economic woes, which bears much of the blame for years of rising debt. Nominal GDP peaked in 1997 at about ¥523.2 trillion. Since then, various administrations have thrown successive stimulus packages at the economy, sending debt skyward, but output has steadily eroded (Exhibit 1). So Japan’s debt-to-GDP ratio has widened from both ends. Nominal GDP has risen lately—including Q2’s 2.9%—but remains about ¥35 trillion below the peak.

Exhibit 1: Cumulative Change in Nominal GDP and Net Public Debt since 1997

Source: Bank of Japan, Japanese Ministry of Finance, Federal Reserve Bank of St. Louis, as of 8/12/2013.

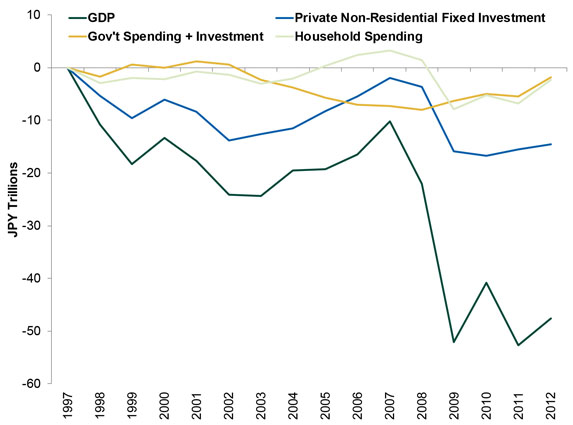

Weak business investment is a big reason (Exhibit 2). This is a symptom of Japan’s many structural issues, which include declining productivity, restricted labor markets, high trade barriers, a lack of corporate dynamism and the world’s second-highest corporate tax rate. Removing the structural barriers to business investment and overall growth, in our view, is likely the most self-sustaining means of tackling Japan’s fiscal issues. Over time, this should reduce the debt-to-GDP ratio and generate higher tax revenues.

Exhibit 2: Cumulative Change in Nominal GDP and Select Components since 1997

Source: Japanese Ministry of Finance, as of 8/12/2013.

But officials are mulling a different tack—hiking sales taxes. Parliament approved this last year, and the first increase takes effect next April. Prime Minister Shinzo Abe and his cabinet are weighing whether to adhere to this schedule. They deem it necessary to raise revenues but fear it could choke consumer spending’s nascent recovery and alienate voters. And because 58% of voters disapprove of the tax hike, many observers see the issue as an indicator of Abe’s willingness and ability to push through unpopular “reforms”—a rather backward analysis, in our view. One, a sales tax isn’t a reform—it’s a Band-Aid on a symptom of a larger issue, and its potential downstream economic effects may prove counterproductive. Two, most Japanese political and business leaders support the hike, so enacting it wouldn’t force Abe to defy the vested interests he’ll have to take on to accomplish meaningful reform. Scrapping it would be a far better sign of Abe’s chutzpah.

For investors, in the meantime, we still don’t see much to be thrilled about. On one hand, sentiment about debt appears too dour—but expectations for reform and economic growth still appear too positive, as evidenced by the backward sales tax views and widespread disappointment over Q2’s GDP growth. Looking ahead, it’s difficult to envision reality exceeding—or even meeting—high expectations. In our view, better opportunities lie elsewhere in the world.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today