Personal Wealth Management / Market Analysis

One Very Bad Reason to Hold Gold

Gold isn't a reliable buffer during times of uncertainty.

This won't protect your portfolio. Photo by Lisi Niesner/Bloomberg via Getty Images.

After the tragic terrorist attacks in Paris last week, some investors may ponder turning to "safe haven" assets-investments that allegedly do better during extremely uncertain, fearful times. Gold is considered one of the top options in this space, and inquiries about how to invest in the precious metal are rising. While gold's "safety blanket" narrative has returned, reality hasn't changed: Gold lacks any mythical powers that make it a better-performing investment during turbulent times.

Gold has been symbolically significant for different cultures around the world for centuries-if not millennia-and many folks assign special meaning to the precious metal. Because it has occasionally backed money, gold is widely considered a "store of value."[i] Adding to its luster[ii], you can touch it, hold it or bury it in the back yard. To many, that makes gold a hard form of wealth, and investors have long associated owning gold with protection against market volatility. It's physically solid, after all. Thus, the thinking goes, when times get particularly bumpy (e.g., unexpected mass violence), the subsequent uncertainty that will rock stocks (not that terrorism actually does for long) won't affect gold, which will remain steady because of its stability-it may even rise since investors would flock to it for safety.

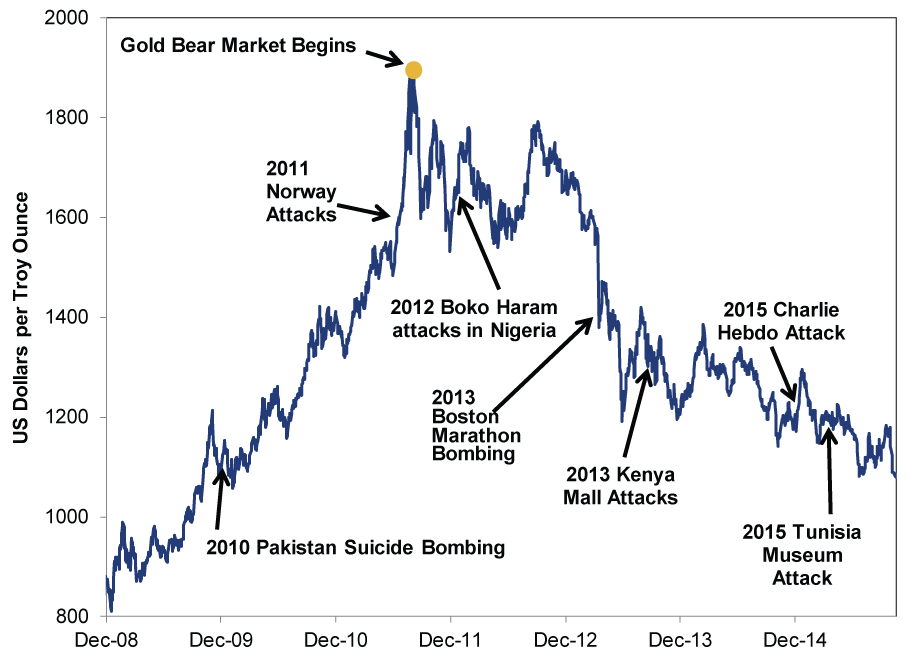

If that were the case, historical evidence would prove this. Yet the data show gold's performance as a hedge is abysmal. While stocks have been in a bull market since March 9, 2009, gold peaked in September 2011 and has been in a bear market for more than four years, notching another fresh low on November 18. Despite plenty of "uncertain" periods of tumult and tragedy since March 2009, stocks have marched on higher while gold has kept falling-seems like its hedging powers don't work very well. (Exhibit 1)

Exhibit 1: Gold Prices During Current Bull Market

Source: St. Louis Federal Reserve, as of 11/17/2015. Gold Fixing Price (3:00 P.M. London Time), Daily, from 12/31/2008 - 11/17/2015.

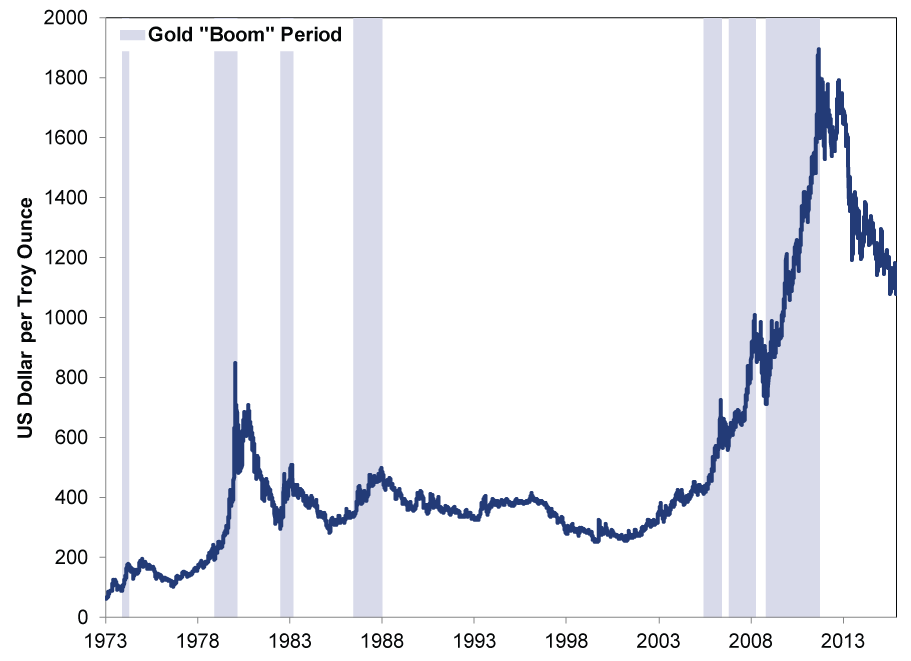

Gold doesn't preserve capital. Yet many think it does. Since gold is tangible-and stocks aren't[iii]-it seems like it will hold its value indefinitely. It doesn't tarnish or degrade. A gold bar will still be a gold bar in a thousand years.[iv] However, like any asset, a gold bar is worth only what someone is willing to pay for it. As its current bear market proves, gold can lose value. Gold's history since the end of price fixing in 1973 highlights the metal's pretty spectacular-and limited-boom (and bust) periods.

Exhibit 2: Gold Since 1973

Source: St. Louis Federal Reserve, as of 11/17/2015. Gold Fixing Price (3:00 P.M. London Time), Daily, from 1/1/1973 - 11/17/2015.

This goes against the whole "capital preservation" thesis. Something that swings so wildly is not a stable store of value. Here is a general truism: If you want to preserve your capital, you shouldn't own something that sometimes goes down. Technically, an asset that truly preserves capital won't lose value at all-its worth today will remain the same in a month, a year, a decade and beyond.[v] That certainly isn't the case with gold. Even during the less boom-and-busty period of the mid-1980s to mid-2000s, gold trended down more than up. If you held gold from the end of its mid-80s boom to the start of its new one in 2005-almost 20 years-gold lost -17.7%.[vi] For investors seeking true capital preservation, cash and its equivalents are the only assets that don't carry the risk of loss. However, even that comes with a big caveat, since inflation eats away at cash's buying power.

None of this is a surprise when you consider what gold really is-a commodity, subject to supply and demand and big swings in sentiment. Strip aside the historical significance and personal bias you may have about gold, and what remains is a metal popular with jewelers and very few industrial uses (e.g., wiring). Given limited physical demand, consider supply's recent history. The global supply glut has impacted commodities from oil to copper the past several years, and gold is no exception-production has steadily boosted supply. The World Gold Council's most recent report shows that even though gold mine production contracted a bit, total supply still rose 1% y/y in Q3 2015-even with gold entrenched in a four year-long bear market. Now, eventually the glut will diminish, and prices will likely rise again to reflect the new supply and demand reality. But unless you can perfectly time[vii] the end of gold's bear market and strategize accordingly-a tall order, given its tendency for quick booms and busts-this seems like a flawed plan for long-term, growth-oriented investors. Successfully investing in gold requires being a consistently terrific market timer.

As developments in Paris continue unfolding, the news may inspire more fearful headlines, adding to the appeal of "safe-haven" investments. But we remind investors that no safe haven asset class exists. All investments carry the risk of loss, regardless of the market environment. And while many will peddle gold as the ideal investment during times like these, glittery ideas may lead investors off the path from reaching their long-term goals.

[i] A store of value could also be a large retailer that rhymes with "ball cart," although we guess the meaning is somewhat different. This alternate definition arguably has a more tangible nature to it.

[ii] Pun intended.

[iii] Unless you have stock certificates or a copy of the trade confirmation.

[iv] Unless you melt it down and fashion it into snazzy jewelry or something.

[v] With no growth, because growth and capital preservation are separate things and impossible to target simultaneously. Anything that grows has risk, as return is compensation for risk taken. To get growth, you must accept the possibility of declines. A true riskless asset, with no possibility of decline, will never grow.

[vi] Source: St. Louis Federal Reserve, Gold Fixings, Daily Pricings, from 12/14/1987 to 2/8/2005.

[vii] And if you can perfectly time the market, it seems to us reading this article is not the best use of your time.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Fed Rate Decision, US-Iran, Inflation in Europe

2026-06-19

2026-06-19 -

Market Analysis Reviewing Q1 Earnings and What Q2 Expectations Say2026-06-18

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today