Personal Wealth Management / Market Analysis

OPEC Plays 'Let's Make a Deal'

OPEC reached a deal aiming to reduce oil output, but it has many asterisks and caveats.

After weeks of will-they-or-won't-they speculation, the 14 OPEC nations released an announcement Wednesday from Algiers, Algeria stating they'd reached an agreement "cutting" oil production. Slightly. Or maybe not even noticeably. Possibly not at all when you consider a broader perspective. But they reached an agreement, and that was better than investors anticipated, resulting in Energy stocks and oil prices leaping higher on the day. Now, if you are someone who's been paying attention to oversupplied energy markets, you might see this as quite bullish news. But there are a huge number of caveats, asterisks and reasons to doubt the lasting impact of this news. In our view, this isn't nearly a significant enough development to change our view that Energy prices likely remain weak for the foreseeable future-weighing on Energy firms' profits and returns.

Since August 8's announcement of a September OPEC powwow, nary a day has passed without some sort of OPEC meeting-related rumor or article hitting the wires. Recently, the flip-flopping has been intense. On September 18, OPEC head Mohammed Barkindo said no deal would be reached in Algiers. The same day, Venezuelan thug Nicolas Maduro claimed a deal to freeze (not cut) production was at hand. The next day, OPEC was said to delay the meeting by a day, and confirmed it was a meeting to discuss a potential meeting at which they may pare back production.[i] Every morning since, there has been a sort of do-si-do in which certain OPEC members claim a deal is at hand, others reject it and the media throws their collective hands up and wonders what it all means. Meanwhile, Energy stocks floundered-lagging the MSCI World in the last three months by about 5 percentage points.[ii]

All this back and forth after months of similar speculation-that proved fruitless-left the punditry and investors skeptical OPEC would do anything at all. No freeze. No cut. Nothing. But Wednesday, they actually did hold that meeting, and in the resulting press release, they announced a production target range of between 32.5 and 33.0 million barrels per day. That's down from the 33.2 million barrels per day OPEC is estimated to have pumped in August.[iii] A cut! Of between 200,000 and 700,000 barrels per day. The market reaction, in the incredibly, ridiculously, almost comically short-term of Wednesday afternoon was that Brent crude oil rose 5.9% and the MSCI World Energy sector jumped 3.2% for the day.[iv]

But this move isn't a statement of what's to come, in our view. It's all about the mismatch between expectations (maybe a freeze, more likely nothing) and reality (a small cut) in the same comically short-term period.

The "cut" brings OPEC production back down to levels last seen ... before the summer. In May. You see, Saudi Arabia usually ramps production up during the summer months-did so this year-and this cut likely results from them agreeing to curtail production in a manner consistent with typical behavior. Moreover, Russia announced the same day it had pumped 11.1 million barrels per day in September-a post-Soviet record, and a rise of 400,000 barrels per day from August. Unsurprisingly, talk of non-OPEC cooperation Wednesday was muted. In case you're keeping score, that's a big chunk of OPEC's projected "cut."

But also, that's all these cuts are: projected. OPEC's targets have often been breached in recent months because the member nations simply can't get on the same page. Venezuela (and others similarly desperate for cash) pump as much as possible. Saudi Arabia, historically the "swing producer"-the OPEC country that would dial up or down production to near overall targets-has eschewed the role since 2014, opting to battle for market share regardless of prices. In this latest deal, who cuts and by how much hasn't even been decided-won't be until November. Who cuts has been the crux of the cartel's issues over the past two years. If they haven't gotten along and followed guidelines thus far, why believe they'll do so now?

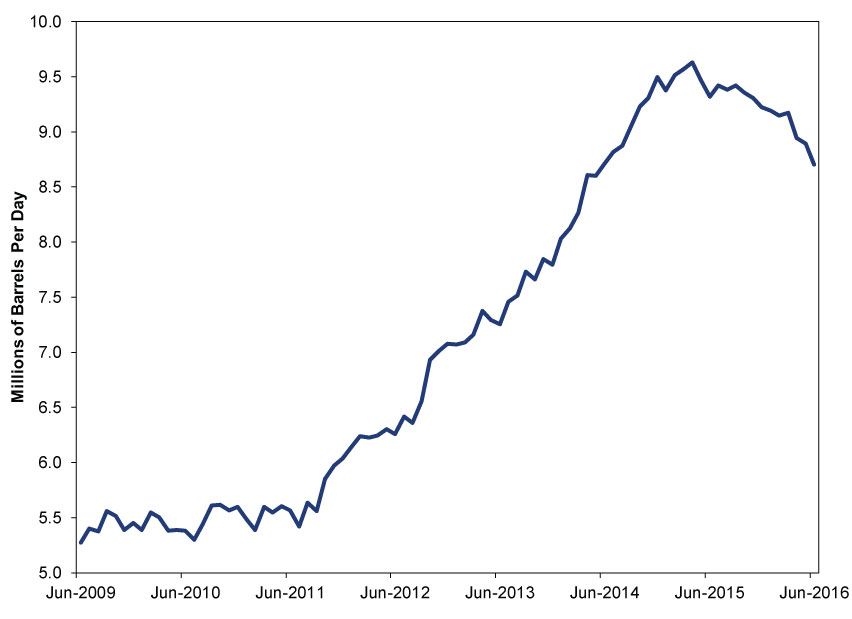

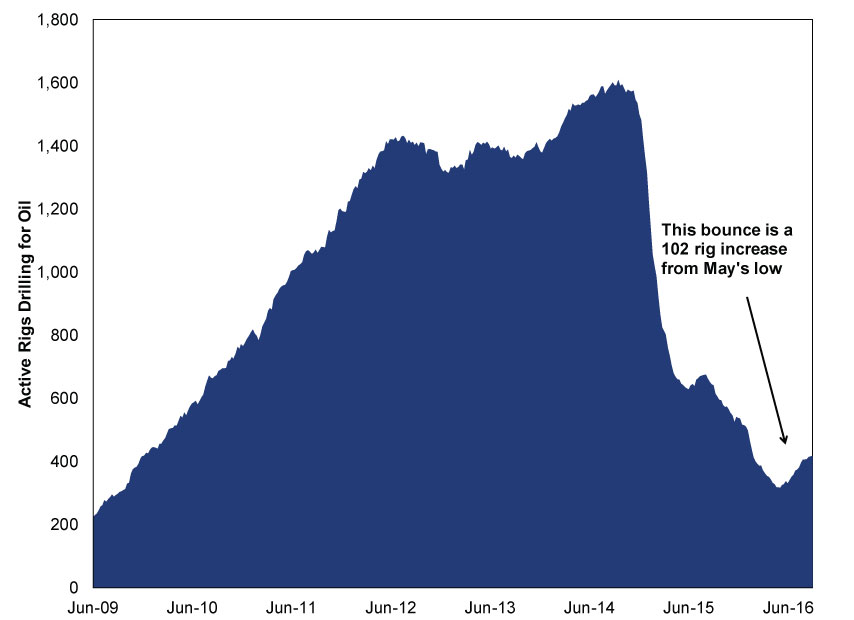

None of this even touches on the US, where production gains since 2009 have massively increased supply. While oil prices' steep decline certainly hit the industry hard, firms have been very slow to materially reduce production. In June 2016 (the latest data available), the Energy Information Administration estimates US oil firms pumped 8.7 million barrels per day. (Exhibit 1) That's down from April 2015's shale-era peak of 9.6 million. But that is only a 9.6% reduction, putting US production where it was in June 2014. Ironically, June 2014 is the month the steep, more than 50% oil-price decline began. Point being: US output reduction hasn't been sufficient to offset the big increases elsewhere. And, now, oil prices rallying from the mid-$20s per barrel in January are spurring renewed activity in US shale fields. The Baker Hughes rig count has been rising for months now, as producers aim for some revenue. (Exhibit 2)

Exhibit 1: US Oil Production, Millions of Barrels Per Day

Source: Energy Information Administration, as of 9/28/2016. June 2009 - June 2016.

Exhibit 2: Baker Hughes Rig Count - Oil Only

Source: Baker Hughes, Inc., as of 9/28/2016. June 26, 2009 - September 23, 2016. Data are weekly.

If OPEC and non-OPEC producers want higher prices, there will need to be lower production than this agreement provides for, assuming producers even adhere to it. Now, it's possible this is merely an OPEC overture to Russia, an olive branch declaring an end to Saudi Arabia's effort to maintain market share at oil prices' expense. Maybe it's the tip of the iceberg, and the Saudi budget's oil-related stress has them seeking higher prices from here, too. All possible. But right now, the fundamental factors are aligned against a sustained rise in oil prices and Energy sector outperformance. We see little in Wednesday's announcement to suggest the change is so major.

CORRECTION: This article originally stated that US oil production peaked in April 2016. This was a typographical error; the peak was in April 2015. Hat Tip: CL.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Interesting Market History Six Years On, Lessons From the COVID-Lockdown Low Endure2026-03-25

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Market Analysis The Golden Paradox2026-03-24

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today