Personal Wealth Management / Market Analysis

OPECs’ Biggest Problem—in Two Charts

OPEC faces internal struggles to cutting back production, but the biggest complication is beyond the cartel's control.

OPEC's efforts to rein in global oil production-and thereby quell the supply glut that has plagued Energy markets for three years-aren't exactly bearing fruit.

While the cartel did manage to extend its previously agreed-to deal to reduce supply from members and a few select non-members (most notably, Russia), they are struggling to maintain a united front. This week, small-producing OPEC member Ecuador took the unusual step of publicly announcing they'd pump more than their allotted 522,000 barrels per day. And output increased from Libya and Nigeria, two OPEC members excused from the deal, which contributed to June OPEC production rising 1.4% to 32.61 million barrels per day-exceeding the group's 32.5 million barrel ceiling. What's more, compliance with the quotas fell to the lowest rate in six months, 78%. While these are no doubt challenges to the cartel's ability to boost crude prices, there is a far bigger problem-one beyond their control: US shale. In our view, it all adds up to low oil prices sticking around longer than most think, a negative for Energy stocks.

Fast-growing US crude oil production was a key factor generating the glut in the first place, which is largely why OPEC's initial strategy was to try to ramp up output in late 2014. They presumed lower prices would squash producers, fuel bankruptcies and bring some production offline. And for a time, they were right.

Yet that was just for a spell. After Brent and WTI oil prices bottomed in early 2016, US oil producers responded to higher prices by pumping more-and with fewer rigs. As Fisher Investments Investment Policy Committee member Aaron Anderson wrote at TheStreet this week, "[R]ather than kill the shale revolution, it seems this ushered in a new chapter -- one targeted at slashing production costs and massively increasing productivity."

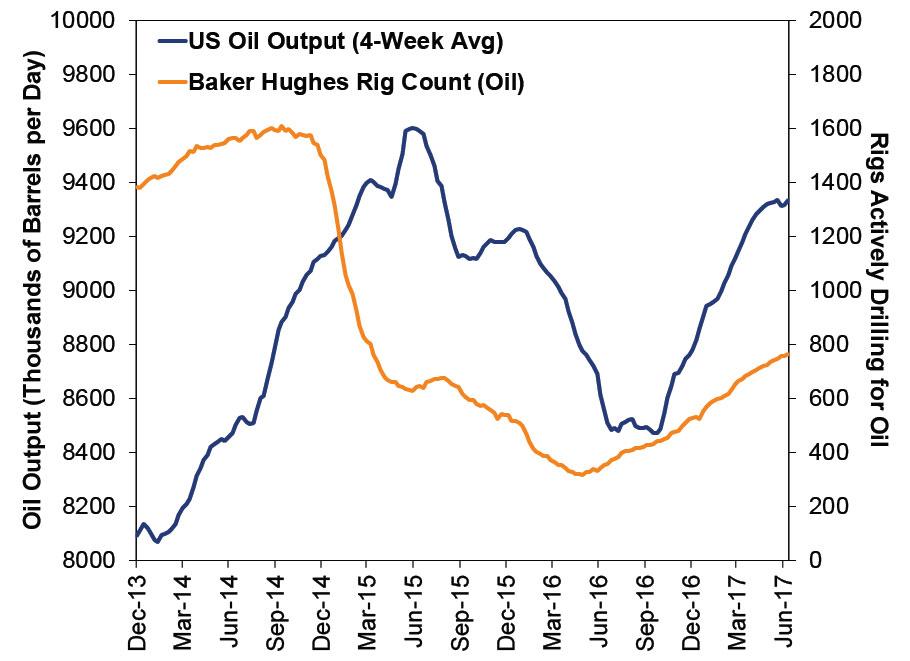

Vast increases in productivity mean US firms are producing about 2% less oil than June 2015's recent high, but with less than half the rigs![i] With rig activity ramping up in recent months, US output looks set to rise.

Exhibit 1: More With Less

Source: US Energy Information Administration, FactSet, as of 7/14/2017. 12/27/2013 - 7/7/2017.

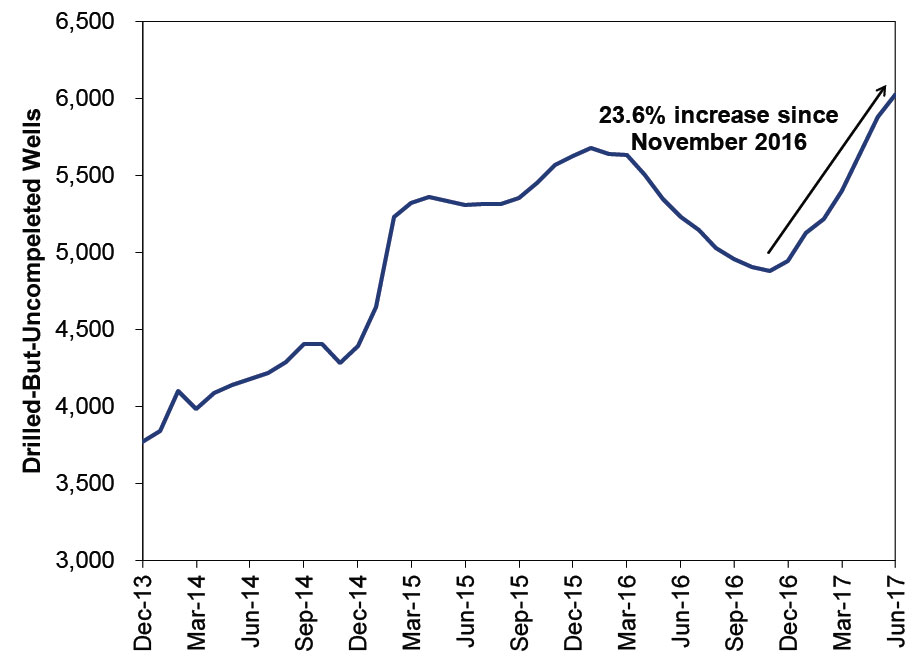

But this isn't all. Above and beyond the production increase, rising rig productivity and the recent uptrend in active rigs, there is a 23.6% increase in drilled-but-uncompleted wells (DUCs) in US shale fields, particularly Texas' Permian Basin.[ii]

Exhibit 2: DUC Season

Source: Energy Information Administration, as of 7/19/2017. Monthly count of drilled-but-uncompleted wells, December 2013 - June 2017 (full data series).

These are already drilled wells that aren't yet producing. They sit dormant, awaiting the injection of water, sand and chemicals-hydraulic fracturing-that cracks the shale rock preventing the oil from rising. If prices tick up, producers will likely frack some of these wells, boosting production. In our view, all this adds up to low oil prices sticking around far longer than OPEC apparently wants. Since oil companies' profits are much more price-sensitive than volume-sensitive, this isn't a good backdrop for Energy stocks.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Interesting Market History Six Years On, Lessons From the COVID-Lockdown Low Endure2026-03-25

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today