Personal Wealth Management / Market Analysis

OPEC’s Quota Taper in Perspective

A less disciplined OPEC along with the US’s ongoing production and export boom should keep global oil supply healthily balanced with growing demand.

This lonely oil rig is far from the only one in the Bakken shale. (Photo by mellypage/iStock by Getty Images.)

OPEC, the oil cartel including Saudi Arabia and Iran, met with other major oil exporters—namely Russia—last Friday in Vienna. They gathered not to enjoy summer opera at its famous Karajan Platz,[i] but to discuss what (if any) changes they should make to their year-and-a-half-old agreement (attempting) to curb their collective oil production at 51.7 million barrels per day (bpd). The verdict? The vaguely worded official statement implies a 1 million bpd increase in production targets, with an explicit rationale to counteract oil’s recent strength. However, it more likely amounts to 600,000 – 700,000 bpd as some producers will have difficulty hitting their quotas. Most analysts expected some increase, but the market response—with oil prices up a few percent on the day—suggests investors expected a larger hike. Still, Brent crude—the international benchmark—remains below May 23’s $79.80 high as oil prices weakened before the conference. We don’t forecast commodity prices, but the modest move appears unlikely to alter the global supply-demand balance much, particularly with ready US supply, which should mean range-bound oil prices—neutral for the price-sensitive Energy sector.

Back in November 2016, OPEC agreed to cap production at around 32.5 million bpd, with non-OPEC members like Russia and Kazakhstan also joining in. Historically, OPEC members haven’t perfectly complied with production targets, fueling skepticism about their compliance with the new curbs. Yet not only did they comply, but production fell further than expected, to 31.9 million bpd, exacerbated by cratering Venezuelan output and Libya’s struggles in maintaining output. As a result, Friday’s deal simply brings OPEC to its November 2016 target.

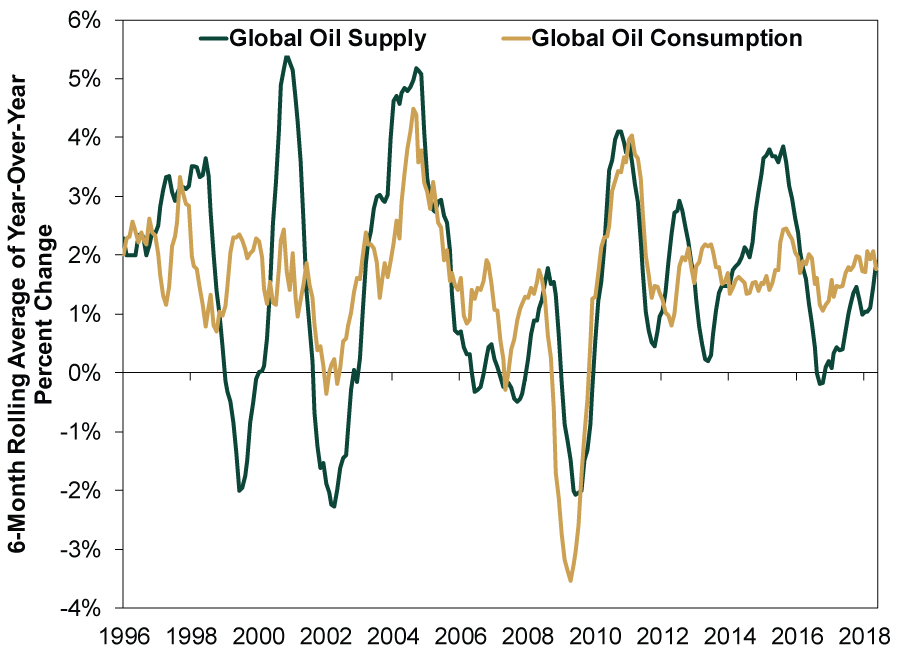

Oil prices move on supply and demand. Global growth broadened and accelerated in 2017, raising demand for oil and resolving much of the global supply overhang even as US production accelerated. Oil inventories in the US and globally have largely returned to normal. With global growth continuing in 2018—and oil demand with it—global oil supply and demand appeared roughly in balance entering OPEC’s meeting. Assuming OPEC and friends increase output by 600,000 bpd, rolling 6-month supply growth would move from 1.8% y/y to 1.9% y/y—in line with demand (1.9% y/y).

Exhibit 1: Global Oil Supply Meeting Consumption Demand

Source: FactSet, as of 6/22/2018. US EIA, 6-month moving average of year-over-year international oil consumption and supply growth, January 1996 – May 2018.

While much media focused on OPEC’s supposedly disappointing supply increases, the US is an increasingly important swing producer. American output is still rising, which should help prevent oil prices from running significantly higher from here. According to the EIA’s latest Short-Term Energy Outlook, US crude oil production is likely to average 11.8 million bpd in 2019, up from 10.8 this year and 9.4 in 2017. Meanwhile, US exports are ramping up, hitting a record 1.8 million bpd in April, triple 2016’s levels.[ii] Expect more to come with some analysts forecasting 3.6 million bpd in 5 years.

Shale oil production technology continues improving, reducing production costs and expanding incentives to drill more. Geological computer modeling is ever more accurate. Steerable drilling technology continues streamlining well production. Producers can now bore longer wells and then hydraulically fracture (frack) them with improved mixtures to yield more oil per wellhead. All of these have raised productivity—and profitability—greatly over the last several years. These techniques sent production in Texas’ Permian basin soaring, and now they are spreading to other promising fields in North Dakota and Oklahoma, where land is cheaper. Oil rig counts have more than doubled in these regions over the last two years. Firms have also been tapping “drilled but uncompleted” wells, further boosting production in North Dakota’s Bakken shale. Breakeven production costs this year average around $44 a barrel—and as low as $25 in some areas—allowing US firms to respond faster to oil price swings, likely enabling output to continue keeping pace with demand.

Although infrastructure bottlenecks likely prevent some of this production surge from hitting the global market in the near term, the industry should fix supply constraints over the longer term. Current pipeline congestion and trucking shortages crimp the amount of oil making its way to ports for shipping abroad. US refiners are also still tuned to processing medium and heavy varieties of crude oil, not the light crude spilling from the nation’s shale formations. But as companies retool and add pipeline and refining capacity, the US should play a larger role in the global market. Some suggest potential Chinese import tariffs on US crude oil present a headwind, but this likely just reroutes oil to Europe (as China buys more from Russia and Saudi Arabia). Substitution costs may hurt some, but probably not as much as headline tariffs would.

Global supply was already likely on the rise regardless of the cartel’s production quota rollback. If anything, OPEC and friends’ decision acknowledges the US’s growing energy dominance. Preserving market share is starting to win out over preserving profit margins. Altogether, global supply and demand suggest production should keep satisfying rising consumption, likely reining in oil prices and keeping most folks—producers and consumers—happy.[iii]

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Inflation, Sell America, US National Debt and More - June 20262026-06-01

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US Jobs, Estate Planning

2026-06-01

2026-06-01 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 25 - May 292026-06-01

-

Market Analysis ‘Sell in May’ Looks to Be Going Astray. Again.2026-05-29

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today