Personal Wealth Management / Economics

Our Perspective on the UK’s August Slowdown

A deeper data dive finds some encouraging nuggets.

The UK released monthly GDP for August today, and with growth slowing from July’s 6.4% m/m to 2.1%, most headlines focused on the seemingly fizzling recovery dashing hopes for a V-shaped rebound.[i] With growth stalling and new restrictions in local hotspots already starting to bite—and GDP still -9.2% below its pre-pandemic peak in February—many fear the road ahead will be long and arduous.[ii] We won’t argue everything from here will be smooth sailing, especially with pubs and restaurants throughout England now facing new limits on operating hours. But digging into the data, we found some interesting tidbits indicating the UK’s economic foundation is a lot stronger than it gets credit for and—for better or worse—reopenings and restrictions remain the swing factor. That doesn’t necessarily make life easier for investors, since these are inherently unpredictable political decisions, but it does suggest “weak economic fundamentals” aren’t reason to shun UK stocks.

The first interesting nugget comes from page three of the Office for National Statistics’ press release: “The accommodation and food services sub-sector contributed 1.25 percentage points to the 2.1% growth in GDP for August 2020, as the combined impact of easing lockdown restrictions, Eat Out to Help Out Scheme and ‘stay-cations’ boosted consumer demand.” Now, pessimists could read this and scoff that GDP was artificially inflated by government largesse, and if it can’t even grow well without the government picking up the tab when folks eat out, then things must be dire indeed. As people who generally believe most sustainable growth comes from the private sector, we won’t try to talk you out of that general viewpoint. But there is another way to view this without casting judgment for or against Eat Out to Help Out: People went out, period. As the UK and other nations started reopening in late spring and early summer, the big worry was that society’s fear of COVID-19 would keep people home and out of restaurants, sapping reopening’s power to generate an economic recovery. Indoor dining was supposedly the most vulnerable to this at all. But August’s results prove that decisively false. Setting aside quibbles over who picked up the tab, the simple fact people actually felt comfortable leaving the house and lingering at their local watering hole suggests that whole notion of psychological scarring causing economic scarring was off base.

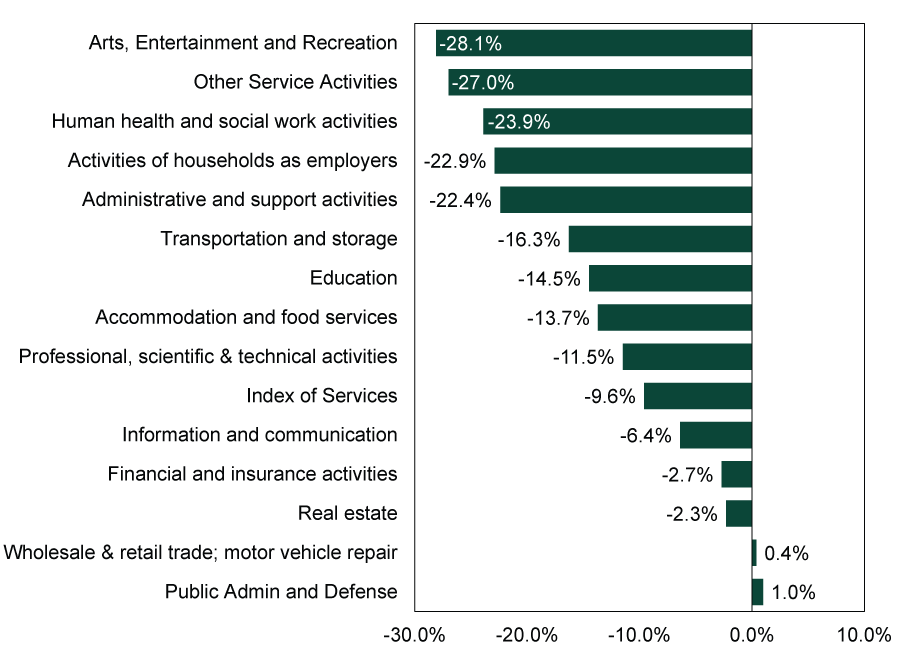

The second set of fun facts comes from page five of the press release, which looks at Services’ 14 sub-sectors. Of those 14, 12 remain below pre-COVID levels, which isn’t surprising. But we were rather struck by which industries are struggling the worst. As Exhibit 1 shows, that includes all the items we wouldn’t rationally expect to recover until the virus is old news and no longer threatens the masses. Stuff like air travel. Rail transport. Entertainment. Elective health care. Paid domestic work. These are all largely still offline. Whatever your opinion of the merits of this, until life on these fronts returns to normal, these areas will likely continue to be sore spots. But when they do reopen, August’s hospitality boom suggests they can recover a lot faster than people might expect.

Exhibit 1: Services and Its 14 Sub-Sectors’ Cumulative Growth Since February

Source: Office for National Statistics, as of 10/9/2020. Cumulative growth in the listed sub-sectors, February 2020 – August 2020.

Now, none of this means stocks can’t continue their recovery. Our research has long shown stocks tend to look about 3 – 30 months out. In young bull markets, they tend to look to the far end of that range. Therefore, in our view, what matters most is that markets can have a reasonable, rational expectation that within the next two to three years, life will be back to normal for everyone. Not just office workers, but the baristas, in-home caregivers, estheticians, shop owners and all other service workers and business owners that depend on in-person commerce. With vaccine progress continuing apace, we think markets are correctly signaling that this outcome is likely.

In the meantime, however, fits and starts in the reopening process could prompt short-term volatility. A second global lockdown as bad as (or worse than) the first could sow panic. But markets move most on probabilities, not possibilities. So watch carefully for that distant bad possibility, but we don’t think positioning for it today makes sense—not with most evidence pointing to recovery and new restrictions much more limited than round one was. To us, today is the epitome of a time to think like markets and focus on the probable future we face.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today