Personal Wealth Management / Market Analysis

Popping Housing Bubbles’ Bubbles

Housing fears are bubbling up, but data broadly show the sector is doing better than many realize.

Source: Clive Rose / Getty Images Sport.

The housing market’s recovery is swimming right along—prices and sales are up and new construction projects are off and running. This has been a nice (if incremental) economic tailwind lately, but some don’t see it as a positive—they see housing’s rise as a new bubble, and fear falling home affordability might be the needle that pops it. In our view, though, these fears are overwrought. Rising home prices have plenty of fundamental support (including affordability), and looking ahead, as housing likely continues outpacing expectations, improving sentiment should lift markets.

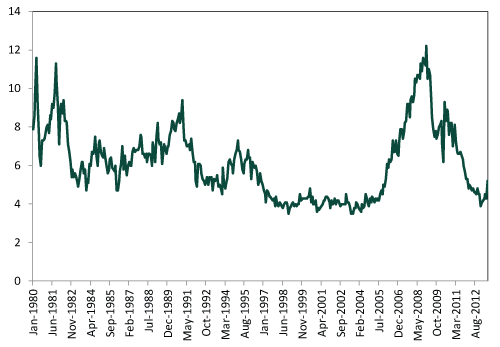

Housing bubbles happen when price increases are out of whack with supply and demand, and that’s simply not the case for housing. The supply of homes for sale is low. Yes, foreclosures have started leveling off and valuations have improved, incentivizing sellers to jump back into the market—but inventories are nowhere near pre-recession levels (Exhibit 1). Conversely, as incomes have risen, more and more buyers are entering the market. More buyers chasing fewer homes create a nice tailwind for prices, as buyers must bid higher to get the home they really want.

Exhibit 1: Monthly Supply of Homes

Source: St. Louis Federal Reserve; 1/1/1980 – 7/1/2013, as of 9/12/2013.

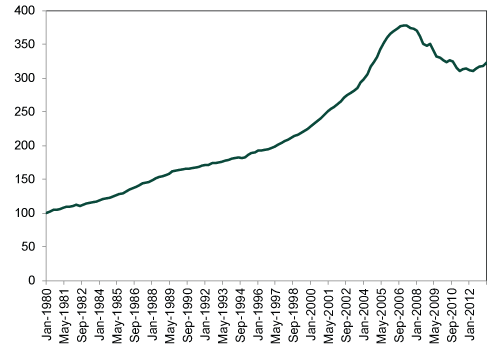

But many folks don’t realize tight supply is driving those bidding wars—they see high demand in a vacuum, deem markets “frothy” and get jittery over a repeat of 2008’s housing crash. But today’s housing gains are nothing like pre-2008, when prices were rising quicker than fundamentals could support them. Today’s price levels are also still nowhere near pre-recession levels (Exhibit 2).

Exhibit 2: All-Transactions House Price Index (Indexed to 100 as of 1/1/1980)

Source: St. Louis Federal Reserve; 1/1/1980 – 7/1/2013, as of 9/12/2013.

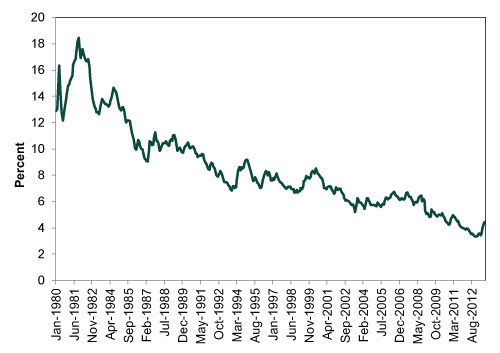

Some folks fear high demand can’t last as interest rates rise—especially as new and pending home sales fell a bit in June amid higher mortgage rates. But coincidence isn’t causality—limited supply is also a big driver of total sales. Plus, rates are relatively low by historical standards (Exhibit 3) and aren’t guaranteed to shoot up from here. Sure, many point to the Fed’s quantitative easing (QE) program for kick-starting the recovery by reducing rates to generational lows—making housing more affordable. The possibility of a taper has sparked fears rates will rise once again and deter homebuyers who would otherwise borrow at lower rates. But the recent rise could be credit markets pricing in QE’s end, which would limit the potential for materially higher rates—credit markets, like stock markets, are forward-looking. Even if rates do rise further once the pressure of QE is lifted, there doesn’t appear to be a catalyst for them to skyrocket out of control. Rising rates could even be a tailwind, potentially, as lenders’ net interest margins expand—higher profit potential increases the incentive to lend, likely increasing mortgage supply.

Exhibit 3: 30-year Conventional Mortgage Rates

Source: St. Louis Federal Reserve; 1/1/1980 – 7/1/2013, as of 9/12/2013.

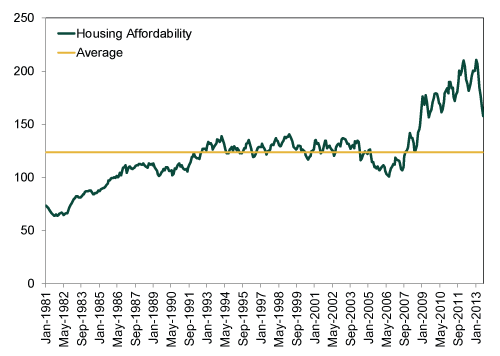

That’s true even with housing affordability ticking down a bit. Affordability may be down some from recent record highs, but housing is still quite affordable. The Home Price Affordability Index currently sits at 157.8—homebuyers earning the median household income have 57.8% more income than they need to qualify for a medium-priced home. This is well above the historical average of 123.7.

Exhibit 4: Home Price Affordability Index

Source: St. Louis Federal Reserve; 1/1/1981 – 7/1/2013, as of 9/12/2013.

In our view, the housing sector is growing steadily and healthily—it isn’t blowing bubbles. But that folks believe it is makes it one more underappreciated positive supporting this bull market. Since housing is only a teensy slice of GDP, its economic impact is small. But as investors gradually realize their housing fears are overwrought, the improving sentiment should provide a nice tailwind for markets.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today