Personal Wealth Management / Market Analysis

Portuguese Politicking

Inside Portugal’s ongoing political upheaval.

Portugal’s latest political rumblings are nothing compared to the 1910 revolution. Photo by Tropical Press Agency/Getty Images.

Two key Portuguese ministers resigned this week, raising the likelihood of a government collapse and renewing eurozone jitters. Heightened eurozone attention could very well contribute to market volatility in the near term, but over time, Portugal’s political troubles shouldn’t much impact global equity markets.

The so-called political crisis began Monday, when Finance Minister Vitor Gaspar resigned, saying Portugal’s failure to meet deficit targets undermined his credibility. Gaspar was replaced by Treasury Secretary Maria Luis Albuquerque—and Foreign Minister Paulo Portas, who heads the junior coalition partner People’s Party (CDS-PP), resigned in protest the next day, deeming Albuquerque’s appointment a continuation of “failed austerity policies.” That threw the CDS-PP’s support of the ruling coalition—and the government’s future—in doubt. Prime Minister Pedro Passos Coelho, who heads the senior coalition partner Social Democratic Party (PSD), said he has no intention to step down and requested support from the rest of the CDS-PP party, but opposition Socialist Party (PS) leader Antonio Jose Seguro has demanded early elections and set a meeting with Portugal’s president to discuss the matter.

CDS holds its annual party congress this weekend, and delegates will likely decide whether to leave the ruling coalition, which likely triggers early elections. If this happens, the contest likely gets scheduled for early Fall.

In my view, Portas’ resignation is most likely political posturing ahead of this potential contest. PS recently took a slight lead over PSD (hence increased calls for early elections), and other parties are seemingly jockeying for position. CDS-PP’s popularity has plummeted recently, and Portas likely believes breaking with PSD—the architects of Portugal’s bailout package—and denouncing their policies will curry voter favor. However, this shouldn’t increase the likelihood Portugal abandons its financial obligations—politicians have made many similar political moves in other peripheral nations, only to toe the line when push comes to shove. In fact, PS cosigned Portugal’s bailout memorandum with CDS-PP, giving them little wiggle room should they take power. They might attempt to further relax deficit targets, but abandoning the program altogether seems unlikely.

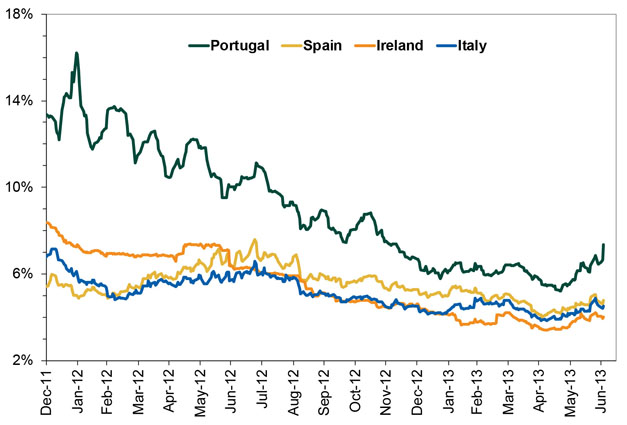

Most importantly, Portugal is well positioned to meet its 2013 bond payments, so there’s minimal risk of default in the near term. But with yields rising in recent days and the economy still in recession, many question whether Portugal can return to primary debt markets on schedule in 2014. Whether or not Portugal does need an extension, however, the impact on the eurozone as a whole appears limited—other peripheral yields haven’t matched Portugal’s recent rise (Exhibit 1). This continues a trend of muted global reactions to negative European news, suggesting investors expect eurozone officials to continue doing whatever it takes to preserve the union in the near term and just muddle along.

Exhibit 1: 10-Year Benchmark Sovereign Yields Since 12/31/2011

Source: Thomson Reuters, as of 7/3/2013.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today