Personal Wealth Management / Market Analysis

Presidential Politics and America’s Economic Relationship With China

Political rhetoric on China doesn't overlap much with reality.

The economic relationship between these countries works pretty well for both sides. Photo by Feng Li/Getty Images.

Editors' Note: Our discussion of politics is focused purely on potential market impact and is designed to be nonpartisan. Stocks don't favor any party or candidate, and partisan ideology invites bias-dangerous in investing.

Tuesday's Republican Presidential debate and campaign rhetoric from both parties suggest Americans should expect one country to hog attention in the run up to 2016's vote: China. Several candidates have championed a need to get tough with the world's second largest economy-with colorful language, sweeping generalizations and harsh accusations. Rhetoric is powerful, and it could scare investors into believing China's status imperils US growth. However, a quick glance at the facts reveals all this China talk is pure politicking, with no grounding in economic reality. The status quo is just fine for America's economy and markets.

Myth #1: Chinese leaders manipulate their currency, keeping it artificially low versus the dollar and thus gaining an unfair trade advantage.

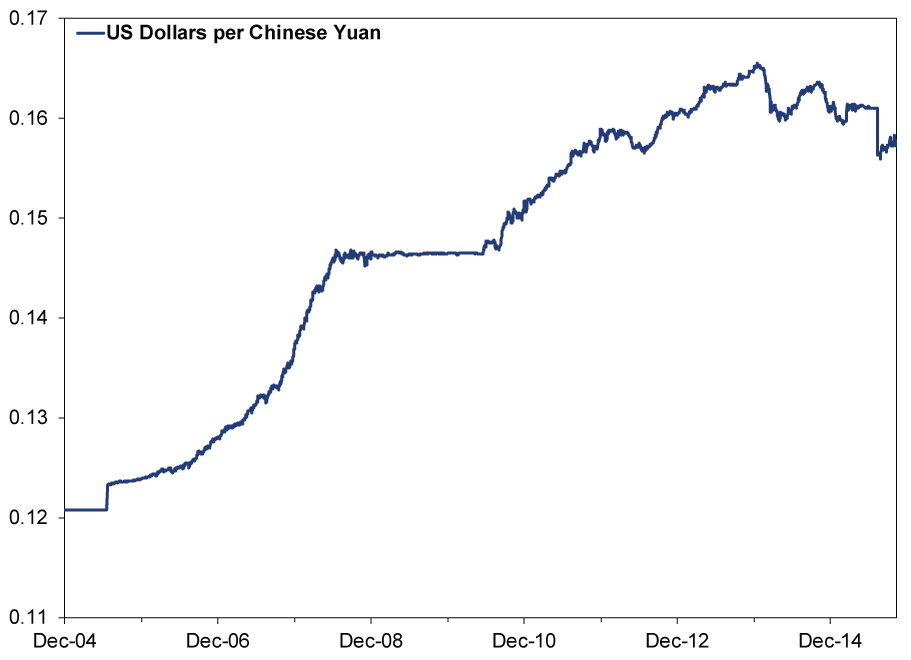

This one surfaces in pretty much every Presidential election. Some candidates claim economists believe the yuan could be undervalued by as much as 40%. This is an extremely outdated estimate, circa 2007/2008 and earlier. Since then, the yuan has appreciated significantly. Accordingly, economists have adjusted their estimates. Earlier this year, the IMF said the yuan was no longer overvalued, and the US Treasury stopped calling the yuan "significantly undervalued." Many economists believe the yuan is trading near its free-market value, if not slightly higher.

Exhibit 1: China's Rising Yuan

Source: FactSet, as of 11/10/2015. CNY:USD spot rate, 12/31/2004 - 11/9/2015

Chinese officials are intervening in currency markets, but not to maneuver the yuan downward. They're trying to stop it from falling. Capital has fled the country this year, and in a vacuum, that would make the yuan fall as investors sell yuan-denominated assets and buy foreign assets. Chinese officials have tried to offset this by selling US Treasury bonds and buying yuan. Word on the street is they have instructed state-run banks to do the same. Bizarrely, those calling for China to stop manipulating its currency are actually arguing for the yuan to weaken. That is how far the rhetoric is removed from reality.

Myth #2: Labeling China as a currency manipulator will allow us to raise import duties, protecting American businesses and restoring our manufacturing base.

Protectionism is an easy sell, sociologically. However, it has a dark side for US consumers and manufacturers alike. Exporters don't pay tariffs-importers do, and they pass the higher costs on. They are effectively a sales tax on foreign-made goods. Consumers would instantly face higher prices, and lower-income households would feel it most acutely. Retailers would feel a big pinch-particularly big box retailers whose bread and butter is selling affordable imported goods. Domestic manufacturers that import raw materials and components would get pinched, too, forcing them to raise prices or swallow lower profits (which would in turn knock investment, hiring and wages). In addition, it's highly likely domestic producers would increase prices too-reducing competition tends to have that effect, and fewer imports means less competition.

Plus, trade goes both ways. Countries usually don't take tariffs lying down. Most of the time, they throw up retaliatory barriers. China has a long, long history of doing this. Usually, it's limited to one or two products-for example, the EU tried to block Chinese solar panels, so China tried to block European wine. But broad-based US tariffs would probably invite broad-based retaliation from China, making it that much harder for US firms to sell into the world's second largest economy. That would hurt manufacturers here, quite contrary to the initial tariff's intentions.

Time and again, history has shown protectionism is a negative for economies and stocks. The Tariff Act of 1930 (aka Smoot Hawley) and the global blowback to it bear significant blame for deepening the Great Depression. Kill international trade, and you kill growth-even more true today, with supply chains increasingly globalized.

Finally, the evidence America's manufacturing "base" needs saving is sketchy at best. Yes, manufacturing employment is down from decades past, but that trend dates back to World War II. Employment, however, is not output, which is up. Technology-driven productivity gains eliminated many of these jobs, and protectionism-targeting China or anyone else-won't bring them back.

Myth #3: China "owns" us, and we must reduce the amount of US debt owned by the Chinese state.

China is the largest foreign holder of US debt. They own $1.27 trillion as of August 2015, or 6.8% of net public debt.[i] (If you add in Belgium's holdings, presuming most of that is owned by China's proxies there, it rises to $1.38 trillion or 7.4% of the total.[ii]) Japan is right on their heels, with $1.2 trillion, or 6.4%.[iii] Yet no one talks about Japan having huge leverage over US policy, "owning" us or otherwise endangering US finances.

There is a good reason for that: Owning US debt doesn't grant any special status or power. Bondholders don't have shareholder-style voting rights. They can't dictate policy. They also can't immediately demand repayment. They can sell, and sometimes the specter of China dumping our debt freaks folks out-but it shouldn't. There is a huge, huge, huge market for US Treasurys. Banks, individual investors, institutional investors and other foreign governments can't get enough of it. There is also a supply shortage, as the Fed has gobbled up over $2 trillion since 2009 and the falling deficit has crimped issuance. If China were to dump its holdings all at once, the sudden supply increase might temporarily hit prices, but most other investors on Earth would smell a dynamite buying opportunity, bringing prices and yields back where they were. Changes in bond yields impact newly issued debt only-interest rates would have to skyrocket and stay there for US debt service to become unaffordable. A quick blip surrounding a China sale probably wouldn't do it. Note, as China sold over $200 billion in US Treasurys via its Belgian proxies over the past 12 months, Treasury yields moved sideways.

Myth #4: Our mounting trade deficit with China weakens our economy.

Sociologically, trade deficits have a reputation as a giant sucking sound. Economically, they are nothing of the sort. Because we run a trade deficit with China, China invests a heck of a lot here. As a general rule of thumb, if your current account is negative (trade deficit), your capital account is positive (investment surplus). When we buy goods from China, we give China dollars, and China invests those dollars here-they buy bonds, stocks and invest in real estate and infrastructure projects. This influx of capital benefits us handsomely.

Plus, the economy isn't a fixed pie. America is extraordinarily good at creating wealth. Even with soaring imports (a sign of roaring domestic demand, I might add), our GDP and gross national income are at all-time highs and rising. That is what ultimately matters-not net trade. If America were a net exporter but had a stagnant economy and created very little wealth, we'd all be worse off.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets — July 27 - July 312026-08-03

-

Expert Commentary 3 Things You Need to Know This Week | US Jobs, Trade Balance, Earnings Reports

2026-08-03

2026-08-03

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today