Personal Wealth Management / Market Analysis

Pssssst—Stocks Don’t Care About the Dollar

If stocks leave a St. Louis train station at 3 pm and the dollar leaves at 6 ...

The S&P 500 keeps clocking new highs, while the dollar sags-and predictably, pundits don't agree whether this is a "despite" or "because of." Did the weak dollar goose earnings and make stocks happy? Or does it reflect darkening fundamentals that stocks overlook? Sorry but reality is probably more boring: The dollar isn't a huge earnings driver, and it doesn't have magic "see the real world" goggles stocks lack. Currencies don't work like that, and outside of banana republics with unsustainable pegs, we don't believe they are major market drivers.

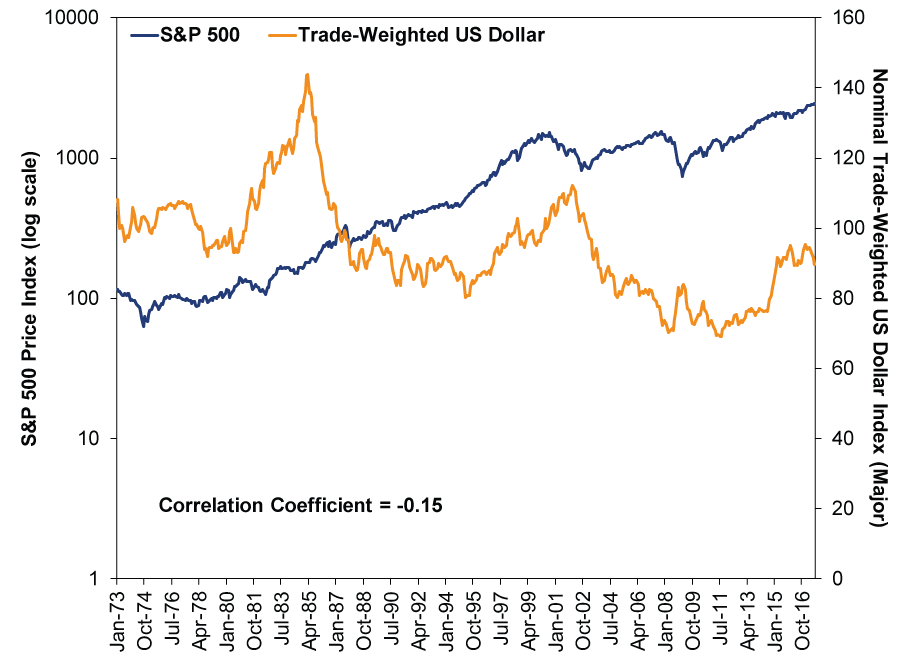

Here is a picture of the S&P 500 and trade-weighted US dollar over the last 43.5 years. As you will see, there are times when both rose, times when they both fell and times when they diverged. The correlation coefficient, which is statspeak for "a number showing how much movement in A relates to movement in B," is -0.15. A correlation of 1 would imply a perfect positive relationship-always moving in the same direction at the same time. A correlation of -1 would imply they always moved in opposite directions. Zero would mean they have no relationship. -0.15 is close enough to zero that you can safely call these two things unrelated. When they move together or opposite, it is coincidence.

Exhibit 1: Stocks and the Dollar Aren't Going Steady

Source: FactSet, as of 8/2/2017. S&P 500 Price Index and Nominal Trade-Weighted US Dollar Index (Major), monthly, January 1973 - July 2017. Price returns used in lieu of total and major index used in lieu of broad due to data availability.

Exhibit 1 is your first clue that the dollar isn't magically more clued into the world or America than US stocks are. Logic is your second clue: The dollar and US stocks are some of the most liquid assets on earth, and all similarly liquid assets digest widely known information instantly and simultaneously. If the dollar had extra-special insight, it probably wouldn't have strengthened in 2008, fallen for most of the 1980s bull market or surged during that early-1980s recession and bear market. That doesn't mean the dollar was ignoring what was going on then! Rather, it means different things influence stocks and the dollar. Yes, both hinge on supply and demand, but in the short run, demand is the primary driver, and stock demand has different inputs than dollar demand. Stocks move most on the gap between economic and political reality and expectations-so, economics, politics and sentiment. Currencies, all else equal, move most on expected yield-money flows to the highest-yielding asset of similar quality.

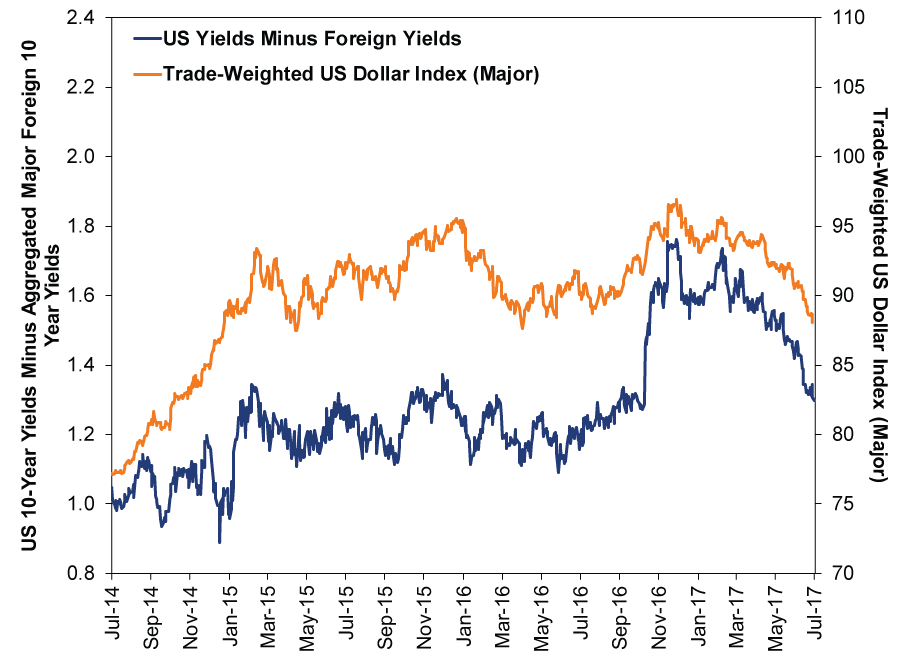

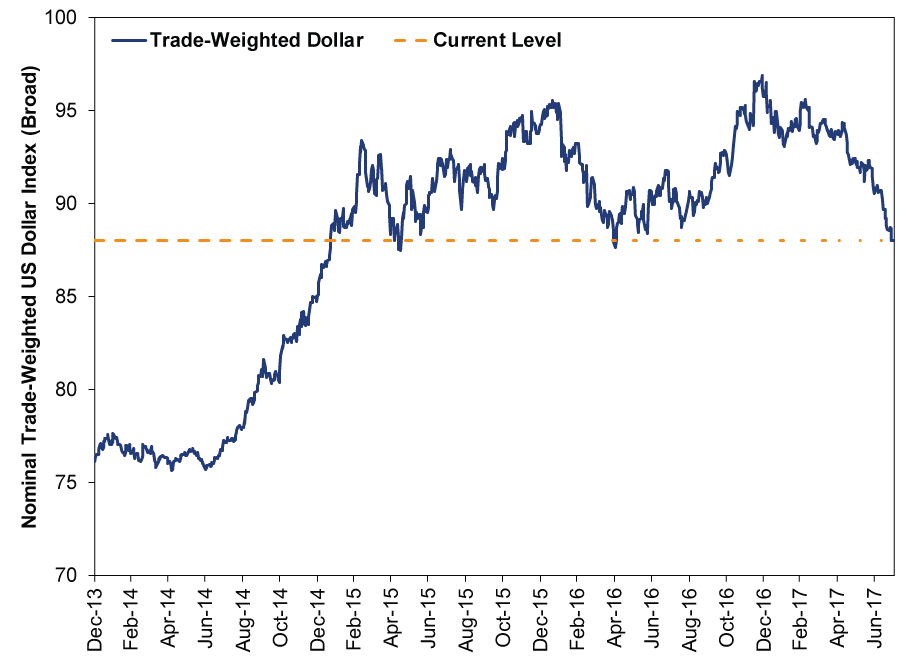

The dollar has won that prize for a few years now, driving demand for the greenback and making the dollar king of the world's major currencies (or something). But since late last year, the gap between US 10-year yields and major trading partners' 10-year yields has shrunk. Its trajectory about matches the dollar's decline over the same period, as Exhibit 2 shows. It isn't that currency market players suddenly hate US fundamentals. Rather, yields elsewhere started showing signs of life, logically driving demand for other assets. Then, too, it isn't like the dollar is hugely weak. As Exhibit 3 shows, it's about where it was back in early 2015. When everyone was complaining it was too strong.

Exhibit 2: Follow the Yield Spreads

Source: FactSet, as of 7/31/2017. Nominal Trade-Weighted US Dollar Index (Major), 10-year US Treasury yields and aggregated 10-year yields from Australia, Canada, Germany, Japan, Switzerland and the UK; 7/31/2014 - 7/28/2017. Yields weighted according to constituent weights in the dollar index basket. Major index used in lieu of broad due to limited 10-year yield data available for constituents of the broad index.

Exhibit 3: Who You Callin' Weak?

Source: FactSet, as of 8/2/2017. Nominal Trade-Weighted US Dollar Index (Broad), 12/31/2013 - 8/1/207.

What about earnings? Conventional wisdom says that when the dollar weakens, US-based multinationals' profits zoom since their overseas revenues are instantly worth more when converted back to USD. Reality, however, is more nuanced. International revenues might get a boost, but international costs rise, too, and US-based multinationals have a lot of those. We are hard-pressed to think of any domestic exporter that sources all raw materials, components and labor from the U-S-of-A. Most have global supply chains. As a result, currency swings' impacts on costs and revenues mostly cancel each other out-to the extent they even show up. After all, most CFOs hedge for this stuff. "Because currency" is about as valid an excuse for earnings ups and downs as "because weather"-and CEOs use it about as often.

So take the collision of all-time stock market highs and a weaker dollar for what it is: trivia. And if you have ever found a pub where this sort of thing actually comes up at trivia night, let us know.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today