Personal Wealth Management / Market Analysis

Putting the Greenback’s Recent Slide in Proper Context

The dollar’s last couple of months aren’t all that extraordinary once you put them in context.

Does the dollar know something stocks don’t? That is the question on pundits’ minds as the dollar sinks versus the euro, hitting a two-year low. With much of continental Europe having less of a second COVID flare-up than parts of the US thus far, the popular viewpoint holds that currency markets reflect the likelihood that the eurozone economy is stronger than the US for the foreseeable future. Implicit in all of this is that if US stocks don’t outright fall as a result, they will trail badly. In our view, this thesis has a couple of flaws. In addition to wrongly presuming stocks are less efficient than currencies, it ignores the dollar’s longer-term history.

Exhibit 1 gives you a look at the euro/dollar exchange rate in 2020 through July 29. What has people talking now isn’t so much the dollar’s relative strength in early 2020—it is the more recent weakness.

Exhibit 1: Euro per Dollar Exchange Rate in 2020

Source: FactSet, as of 7/30/2020. Euros per dollar, spot rate, 12/31/2019 – 7/29/2020.

That may look extreme, but it is basically a function of the Y-axis being a narrow range—and the timeframe lacking any sort of broader perspective. Consider Exhibit 2, which plots the full history.

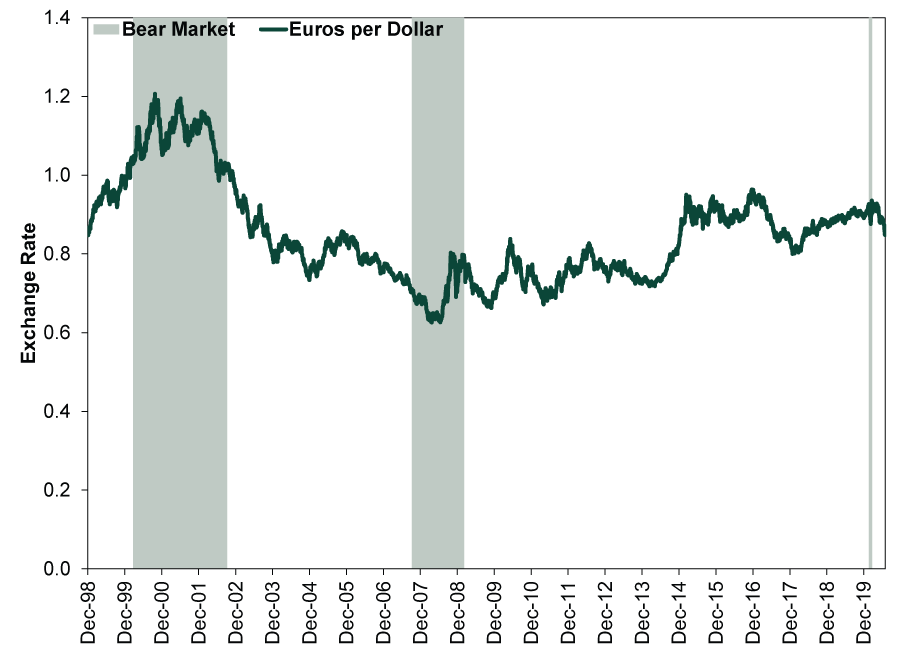

Exhibit 2: The Dollar’s Full History Versus the Euro

Source: FactSet, as of 7/30/2020. Euros per dollar, spot rate, 12/31/1998 – 7/30/2020.

With all the eyeballs on the greenback, you would think its recent performance is somehow unique. But it isn’t—actually, it is rather consistent with how the dollar normally fares in a new stock bull market. As Exhibit 2 shows, the dollar strengthened versus the euro during the past three bear markets, including this year’s. This isn’t mere coincidence. When times are rough, money tends to flock to so-called safe havens, and ye olde US Treasury bonds are many folks’ favorite choice due to Treasurys’ unmatched depth and liquidity. That shows up in currency markets as demand for dollars. But as the flight to quality unwinds in a new bull market and money goes back to assets with higher perceived risk, the dollar tends to depreciate. It is a statement about the global economy’s prospects, not an indictment of America as an investment opportunity. To us, the dollar’s recent performance looks like a typical post-bear market return to normalcy.

A second thing you might have noticed about the above chart: The dollar fluctuates against the euro a lot during bull markets, with no set pattern. In the bull market that ran from October 2002 to October 2007, the dollar overall fell. In the bull market that ran from March 2009 through late February 2020, the dollar strengthened overall, but with several long slumps along the way. One of the steepest encompassed most of 2017, a gangbusters year for the S&P 500.

Contrary to popular belief, the dollar isn’t inherently more prescient than stocks. All similarly liquid markets digest the same widely discussed information at the same speed. People who buy and sell stocks aren’t locked in a room without any information on COVID caseloads and new local lockdowns. They see all the same news nuggets and forecasts currency traders and bond buyers see. To say one market is right and one is wrong is to fundamentally misinterpret how markets work, in our view. Stocks and currencies are equally efficient. They just have no pre-set relationship.

In our experience, the dollar—like oil prices—is just one of those things people tend to fear whether it is rising or falling. Call it a quirk of human nature, we guess. For behavioral scientists, it is probably a gold mine. But for investors trying to figure out their next move with stocks, we would tune down dollar chatter.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17 -

Market Analysis Pumping Up the Yen?2026-07-17

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today