Personal Wealth Management / Economics

Q1 Earnings: Why Profits’ Dip Doesn’t Mean Stocks Will Drop

Despite the headline drop, Q1 earnings aren't a sign of impending gloom for markets.

Q1 earnings season is nearly over, and with only two companies left to report, S&P 500 earnings will surely notch their fourth consecutive year-over-year drop-the longest streak since the Global Financial Crisis. Public Service Announcement: This is not a reason to be bearish. Actually, at the risk of inviting some allegations our view is Pollyanna-ish, we see several silver linings when we dig into Q1's results-and some optimistic takeaways for the foreseeable future.

For all their short-term wackiness, in the medium and longer term, markets are pretty efficient. They are also forward-looking. While number crunchers are only now confirming S&P 500 earnings fell -6.7% in Q1[i], markets have long known profits would be ugly-partly because analysts began projecting the decline well before the quarter even began, and partly because stocks lived it. Markets don't wait for confirmation of economic data, earnings or any other tangentially market-related information. They register it real-time, as investors trade based on their observations, opinions, hopes, fears and every bit of information they hear. Every day in Q1, millions of investors bought and sold based on their general perception of the world around them-and the countries, sectors and firms therein. For the quarter's first half, that general perception was decidedly negative, as folks feared a host of perceived ills would wreck profits-and indeed, to an extent, they were right. In the second half, however, some of the gloom lifted, and investors started bidding stocks back up. Folks realized the world wasn't so bad as they feared-and here, too, they were right.

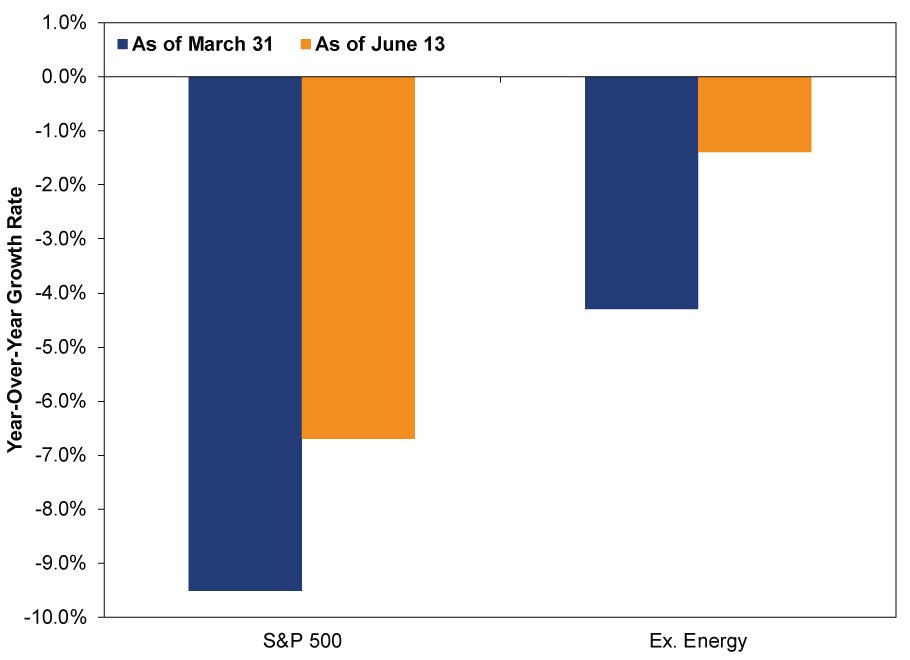

Q1 earnings season is compelling evidence for that last sentence. On March 31, analysts projected a -9.5% y/y S&P 500 Q1 earnings drop, and -4.3% y/y when excluding the much-maligned Energy sector's projected -105% y/y freefall.[ii] Yet as firms reported, they beat those expectations by a decent margin. A -6.7% drop looks bad in a vacuum, but compared to -9.5%, it's an improvement. Same goes for the -1.4% drop ex. Energy-better than -4.3%.[iii] Stocks move on the gap between reality and expectations, and while you can't pin market movement on any one thing, we think it's telling that stocks rose a bit over earnings season as a whole. If they were hugely bothered by the results, that wouldn't be the case. Consistently negative surprises would have taken a toll.

Exhibit 1: Earnings Didn't Stink as Badly as Feared

Source: FactSet, as of 6/13/2016.

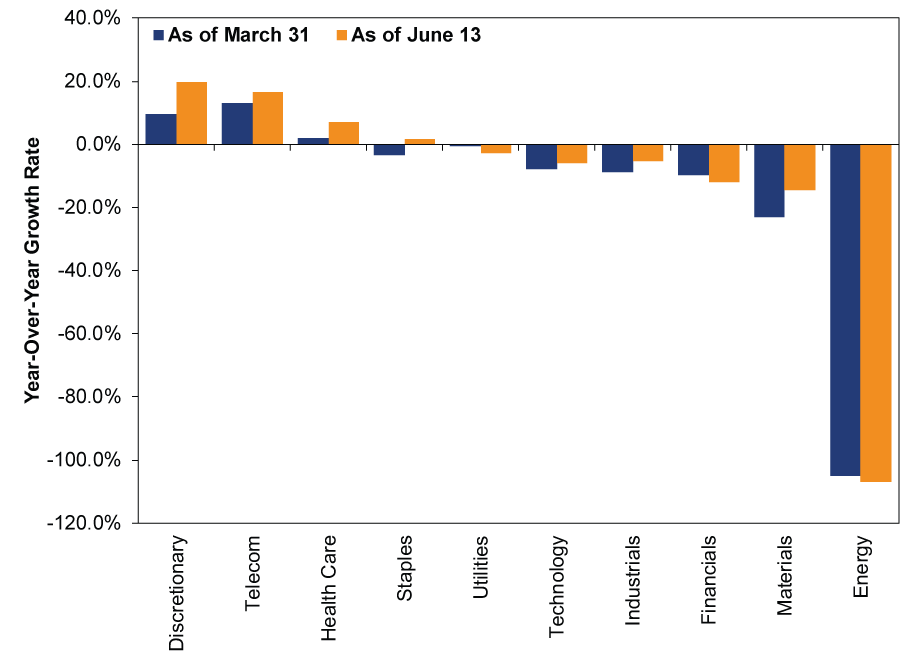

Break the results down by sector, and you'll see some actual positives. As Exhibit 2 shows, earnings rose in four sectors and beat pre-earnings season estimates in seven. The best-performing sector was Consumer Discretionary, an economically sensitive category. Not only did it beat preseason estimates by 10 percentage points-the biggest surprise-but its earnings grew nearly 20% y/y. The less economically sensitive Utilities sector, by contrast, was one of just three to miss expectations. If the US economy were in an actual, troubling rough patch, those results would likely be reversed. (Energy, meanwhile, did even worse than expected, with net income falling 107%, resulting in a small loss for the sector.)

Exhibit 2: Sector-by-Sector Earnings

Source: FactSet, as of 6/13/2016.

But everything we've just written deals with the past-stocks have moved on. They're eyeing the future, and the future looks brighter than the recent past. Analysts expect earnings (total and excluding Energy) to decline again in Q2, but that's widely known. Those expectations are already baked in to prices. After Q2, the math gets more favorable, as last year's lower results become the new base for the year-over-year calculation-an easier hurdle to clear than those high 2015 totals. Hence earnings should broadly stabilize. As we write, consensus expectations are for S&P 500 earnings to rise 0.9% this year, with six sectors positive.[iv] If most firms keep beating expectations, the final tally could easily be even better.[v]

But for stocks, near-term earnings are only one piece of the puzzle. Earnings growth is nice, but it isn't required for a bull market to continue. Earnings suffered some toward the end of the 1990s' long bull as well, and stocks still did great. When firms are profitable and investors have confidence those profits can continue-whether they're a bit higher or lower-then stocks are generally happy. So the question isn't, will earnings grow? Rather, are firms and their customers healthy enough for profits to keep pouring in for the foreseeable future?

To quote everyone's favorite sage, the Magic 8-Ball, signs point to yes. Using the BEA's much broader dataset, national corporate profits inched up in Q1, suggesting corporate America isn't in freefall. Backward-looking, but noteworthy. Firms' net cash flow-funds available to invest-rose too, as sales rose and balance sheets improved. Most economic indicators picked up in April and May, suggesting demand is rising among consumers and businesses. Disposable income is rising steadily. Loan growth is solid in America and improving in Europe. Broad money supply (M4) is rising at a fast clip. Yield curves have flattened a bit lately, but don't read too much into short-term volatility-and a flatter US yield curve earlier in this expansion didn't derail growth or profits. Though it's just one data point, US trade in goods jumped in April, breaking with the recent trend. World trade growth has been weak in recent months, so it is worth watching to see if this turns into a rebound, which would also bode well for firms globally-more goods crossing oceans and borders means more economic activity overall.

Simply put, this is an expansionary economic backdrop. Firms generally stop profiting when the world contracts, not when most indicators point to a global economy with plenty of fuel. Stocks move before economic data do, so this is not a time to dwell on Q1's big earnings drop. Doing so invites recency bias-assuming the future will resemble the recent past-a behavioral error. We think this is a time to focus on the future, see the good signs most others miss, and stay disciplined. Bull markets have a long history of rewarding patience, and we expect this one to do the same.

[i] FactSet, as of 6/13/2016.

[ii] Ibid. And yes, it is odd to see -105%, but it is explained rather easily: The Energy sector was expected to post an aggregate loss versus small profits a year ago.

[iii] Ibid.

[iv] Ibid.

[v] Or it could be worse. We aren't saying it will be, but it would be myopic to dismiss the possibility.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 4 - May 82026-05-11

-

Expert Commentary 3 Things You Need to Know This Week | April CPI, Prediction Markets, Financial Fraud2026-05-11

-

Politics UK Stocks and the Starmer Scuttlebutt2026-05-08

-

Expert Commentary This Week in Review | Tariff Update, National Debt Concerns, April Jobs Data

2026-05-08

2026-05-08

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today