Personal Wealth Management / Market Analysis

QuitE Wrong

The eurozone has been doing fine without the ECB's QE.

ECB chief Mario Draghi, before the party started. Photo by Martin Leissl/Bloomberg via Getty Images.

So the eurozone economy is turning up, and the media is praising the ECB's quantitative easing (QE) program for "bearing fruit already." So is ECB chief Mario Draghi, though it wasn't he who threw the confetti at the ECB's presser Wednesday. Even though the ECB has been buying government bonds for all of five weeks. And the eurozone started accelerating months ago. And evidence worldwide shows QE depresses more than it stimulates. That folks are so quick to credit QE and overlook months of improvement shows how, despite improving sentiment, most still underrate the currency union's economic health.

While eurozone sentiment is warming, it is behind the times. The media calls recent growth evidence of "green shoots," which one typically spies as spring (read: economic recovery) begins-an odd thing to say considering the eurozone has grown seven straight quarters through Q4 2014. While growth hasn't been rip-roaring, it is becoming increasingly broad-based. Spain and Ireland are growing nicely. So are the Baltics and Eastern Europe. Growth is broader within countries, too. Markit's eurozone composite purchasing managers' index (PMI)-which measures the percentage of businesses reporting growth-hit 54.0 in March, up from February's 53.3, and the fourth straight month of acceleration (readings over 50 indicate expansion). Italy and Germany hit eight-month highs at 52.4 and 55.4, respectively. Spain jumped to 56.9. Alleged "sick man" France hit 51.5. Ireland led the charge at 59.8-crazily, a 9-month low, which tells you just how long the eurozone has been improving with little fanfare.

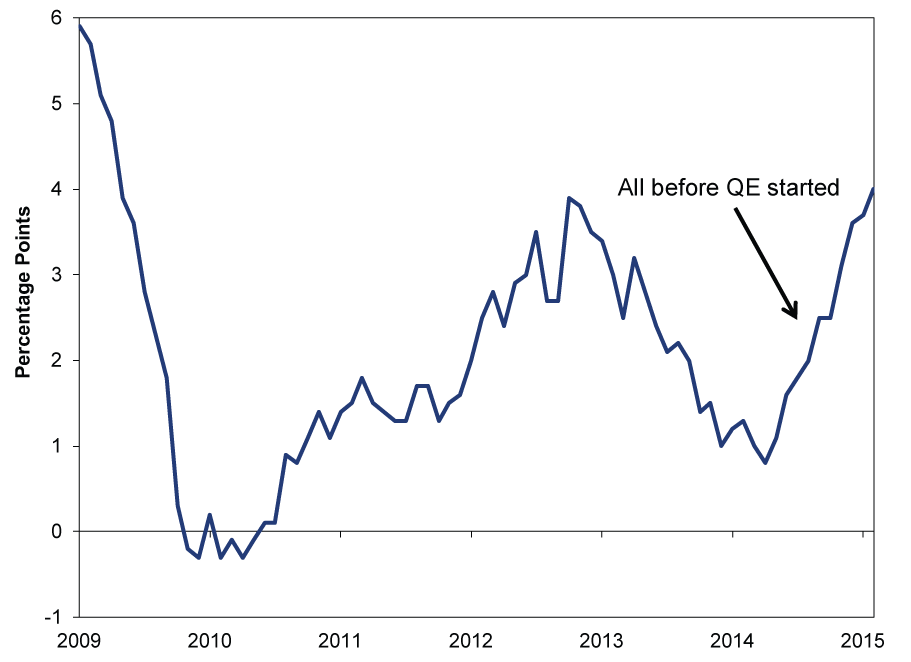

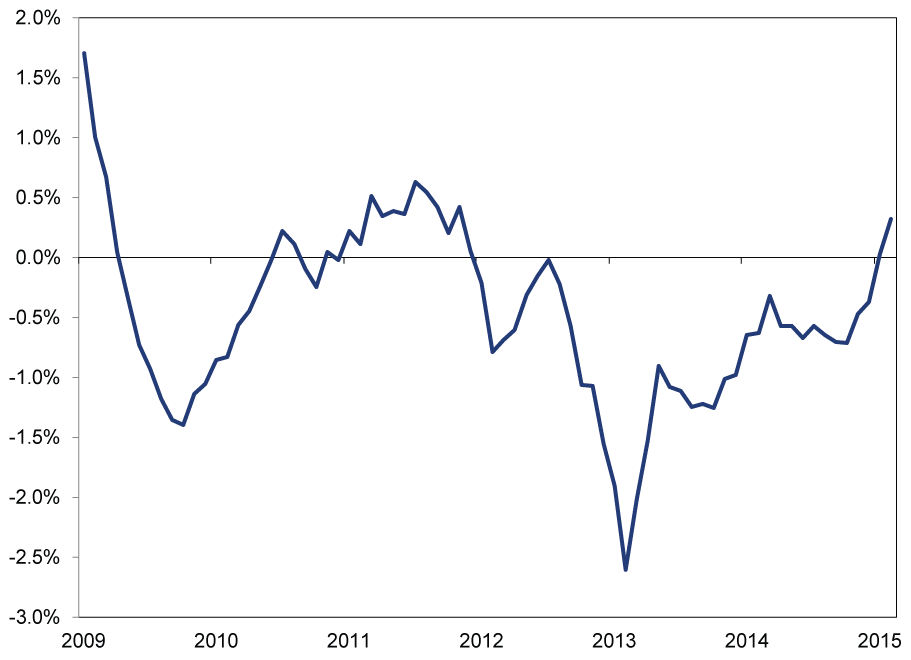

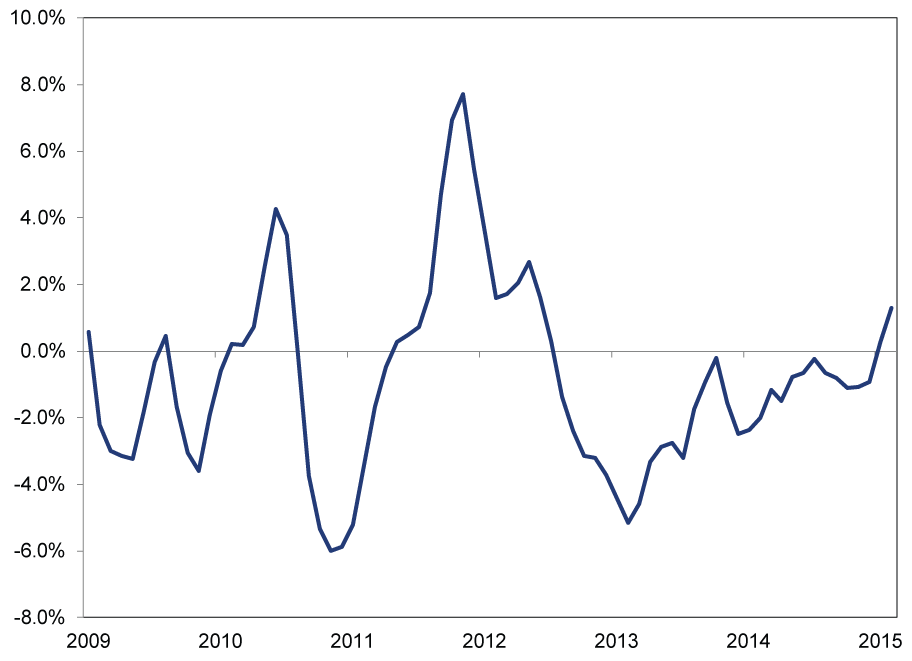

Yet the popular view is that QE drove the uptick, which strikes us as odd. Not just because full-fledged QE began just weeks ago[i], but because broad money supply and lending began improving long before QE, too. QE is designed to boost lending-and the broad quantity of money-as central banks use long-term asset purchases to add excess reserves to the system and reduce interest rates, spurring folks to borrow more. About a century of monetarist theory and real-world evidence shows rising money supply translates to rising output. Yet this started happening without QE! M3 money supply (the eurozone's broadest measure) has accelerated 10 straight months. Year-over-year growth hit a nearly six-year high in February, the month before QE began. (Exhibit 1) Lending soon picked up, too. (Exhibits 2 and 3)

Exhibit 1: Eurozone Money Supply (M3) Y/Y Growth

Source: ECB, as of 4/15/2015. Euro area monetary aggregate M3 annual growth rate, from January 2009 - February 2015.

Exhibit 2: Eurozone Business Lending Rolling Three-Month Change

Source: ECB, as of 4/15/2015. Total outstanding amounts to Non-Financial Corporations, from January 2009 - February 2015.

Exhibit 3: Eurozone Lending to Private Sector Rolling Three-Month Change

Source: ECB, as of 4/15/2015. Total outstanding amounts from Monetary Financial Institutions, from January 2009 - February 2015.

Business loan growth in Germany and France-the eurozone's two largest economies-has been smashing. German business lending rose 1.9% y/y in February-its third straight acceleration-and has been positive 11 straight months.[ii] French business loan growth is even better, accelerating for a fourth straight month to 2.9% y/y in February and positive 14 straight months.[iii] Yes, Italy is lagging badly, dragging down the bloc's total, but that's largely because banks there are still raising capital after several failed last year's stress test-a regulatory issue, not monetary. Overall, the eurozone is already experiencing everything QE is supposed to do. The Conference Board's Leading Economic Indexes also signaled this upturn months before QE began. Eurozone LEI is up six of seven months through February, and German, French and Spanish LEIs have been in long, albeit uneven, uptrends, too. All these cyclical factors suggest the eurozone doesn't need the ECB's help. And almost no one sees it-a bullish gap between sentiment and reality.

That would be fun trivia if it weren't for the fact QE actually depresses, rather than stimulates, growth. By shrinking the spread between short-term rates and long-term rates, QE flattens the yield curve and reduces banks' potential profits on new loans, as banks borrow at short-term rates, lend at long-term rates and profit off the spread. Smaller spreads are a big deterrent to loan growth. Hence why loan growth and broad money supply (M4) fell in the US and UK for long stretches during their QE programs, and why the US and UK actually accelerated after the Fed and BoE stopped QEing.

In the eurozone, life would likely be best if Draghi ran a victory lap and ended QE soon, before the flatter yield curves squeeze lending's recent pickup. What wouldn't be good is if QE did start dragging and the ECB felt compelled to layer on more QE in a vain attempt to flood new money-similar to what Japan did in the early 2000s and is doing today. Japan has had three recessions during its latest QE, which began in late 2010-even as the global economy grew. The BoJ's program is the monetary equivalent of "the beatings will continue until morale improves."

What the ECB ultimately does, of course, is unknowable today. After being interrupted by a protester at his press conference Wednesday, Draghi said QE as having its desired effect, and tried to quash rumors he'd end it early: "I'm quite surprised by the attention a possible exit from the program receives when we've only been in the program for a month. ... it's like asking after the first kilometer, are we going to finish this marathon?" But central bankers have a way of changing their minds, so you never know. In the meantime, though, what matters is most view the eurozone as dependent on a monetary morphine drip, and reality shows no such thing-even with recent acceleration, things are better than perceived.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Quasi-QE began last autumn, when the ECB began buying small amounts of covered bonds and asset-backed securities.

[ii] Source: ECB, as of 4/15/2015.

[iii] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today