Personal Wealth Management / Market Analysis

Rating Agencies: Late as Usual

With Moody’s raising its outlook for US debt on Friday, a look at what happened during our two years on “negative” watch confirms ratings agencies’ decisions aren’t predictive.

The US stock market has been looking up in in spite of credit rating agencies’ less than stellar outlooks. Photo by Spencer Platt/Getty Images.

A ratings agency made another earthshattering proclamation on Friday: Moody’s raised its outlook on US Treasury bonds from “negative“ to “stable,” saying the US economy has shown resilience despite what it considers major government spending cuts. It’s a typical backward-looking assessment, just like Moody’s August 2, 2011, decision to put the US on negative watch due to “the small but rising probability of a default on the government’s debt obligations because of a failure to increase the debt limit”—or, more simply, because Congress was dithering over the debt ceiling. Yet after two years of broad economic gains, fiscal improvement and nothing approaching default, it’s once again clear ratings agencies’ decisions aren’t predictive, and investors should pay them little heed.

With Moody’s threats coming less than a week before S&P’s downgrade of US Treasurys, headlines everywhere fretted the US’s solvency. But not only did we not default—the US’s already strong fiscal footing improved! Debt Interest payments fell, both absolutely and as a share of GDP. Tax revenues rose, bringing the debt service burden below 9% of the government’s intake. All while on “negative” watch.

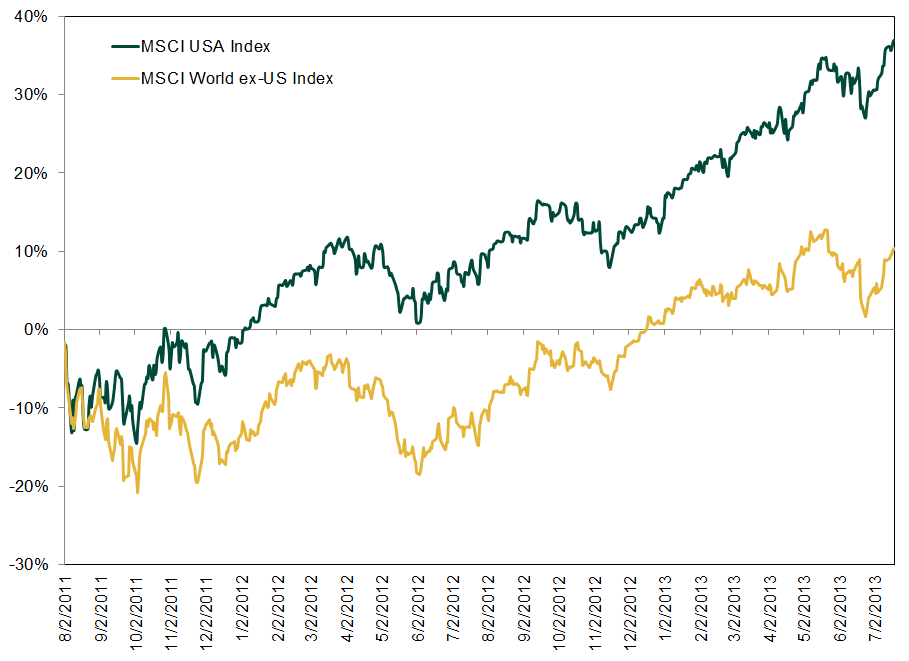

And stocks did great, despite investors’ widespread fears otherwise. While the US was on negative watch, the S&P 500 returned 37.5%i . The US did great relative to the rest of the world, too—the MSCI USA index handily outperformed the MSCI World ex US Index over the same period (Exhibit 1).

Exhibit 1: MSCI USA Vs. MSCI World ex US Cumulative Returns

Source: Thomson Reuters, as of 7/19/2013.

The economy gained momentum, too, despite Moody’s stated concerns about “the strength of potential growth in the coming year or two”—based on “recent downward revisions of economic growth rates.” Not only did GDP keep growing, but it accelerated a touch. Factor out the government spending drag, and you’ll see the private sector sped up even more.

US Treasurys, too, did much the opposite of what you’d expect of a security with a “negative” outlook. Yields fell after Moody’s pronouncement and spent much of the next 22 months near generational lows—investors seemingly didn’t see US Treasurys as higher risk. Rather, they likely considered the US’s deep and liquid capital markets and made their own assessment of America’s innovation-rich, private sector-driven economy—an assessment that didn’t dovetail with Moody’s proclamations.

Alongside the US’s broad economic progress, Congress has kept up the same old politicking that got us downgraded/on negative watch in the first place. Legislators dithered, missed deadlines and kicked the can on the fiscal cliff, still haven't passed a budget in four years and are approaching yet another debt ceiling battle. But the economy, stock markets and Treasury markets haven’t cratered. That Moody’s is willing to raise its US outlook even though the political landscape hasn’t changed suggests even the raters understand the US's brand of heated politicking just isn't very economically impactful and didn't really warrant a lower debt outlook in the first place. (Besides, it’s somewhat humorous an agency tasked with judging creditworthiness says it’ll upgrade in spite of less spending.)

Overall, Moody’s decision to raise its US outlook is just one more backward-looking decision and is really more affirmation of what many are slowly coming to realize: US economic fundamentals still look strong, with the private sector still leading the charge, and corporations are still healthy and profitable. That a ratings agency has seemingly only just noticed is merely proof investors shouldn’t depend on ratings agency guidance when making portfolio decisions.

i Source: Thomson Reuters. S&P 500 Total Return from 8/3/2011 to 7/18/2013.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics On Tariffs, the Supremes Have Finally Sung2026-02-20

-

Expert Commentary This Week in Review | Government Shutdown, Tariff Ruling, UK Inflation

2026-02-20

2026-02-20 -

Expert Commentary Is AI Reshaping the Future of Work2026-02-20

-

Market Analysis “Sell America” Fears Don’t Square With Data2026-02-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today