Personal Wealth Management / Market Analysis

Resistance Is Futile

Stocks have plenty of ammo to pierce an arbitrary line on a chart.

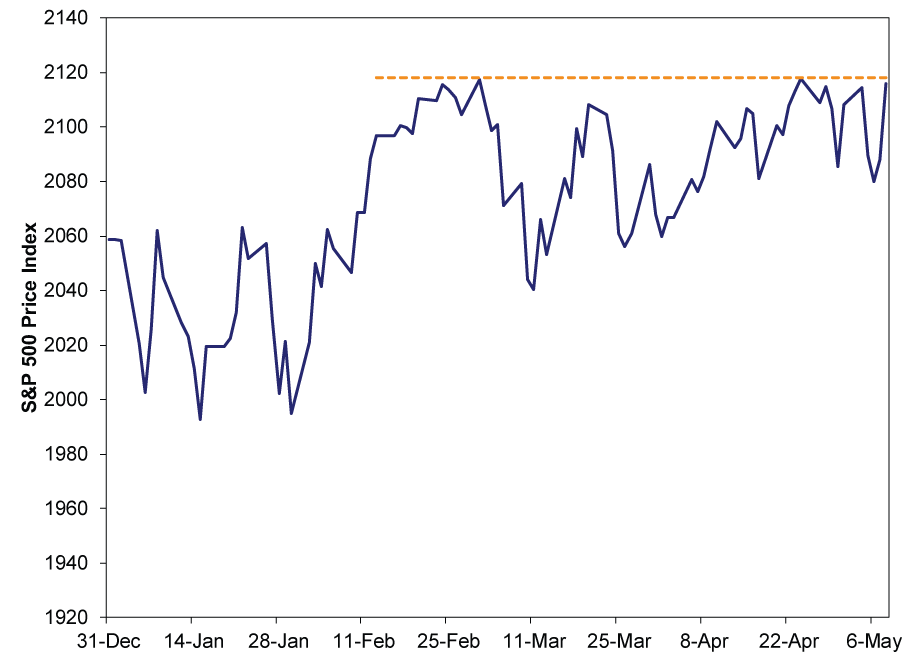

2118. This is the number the S&P 500 Price Index has struggled in vain to cross since mid-February. It came close on March 2, closing at 2117.393. It got even closer on April 24, closing at 2117.69. But no dice. One analyst calls it the "iron ceiling."[i] Technical analysts would call it resistance. We shun jargon and prefer to draw a picture:

Exhibit 1: The S&P 500 Meets a Dotted Line

Source: FactSet, as of 5/11/2015. S&P 500 Price Index, 12/31/2014 - 5/8/2015.

Pundits often say such lines are impregnable without some catalyst to send stocks above, hurtling them into happy new heights. Today, it's fashionable to say the catalyst should be "dry powder," as in cash on the sidelines just waiting for some eager beaver to plow it all into stocks and drive prices higher, but the powder is all gone, so we're all out of luck. But we have no problem being unfashionable, so we will happily correct this misperception: Ceilings don't exist, and stocks don't need new money or new buyers to keep on rising.

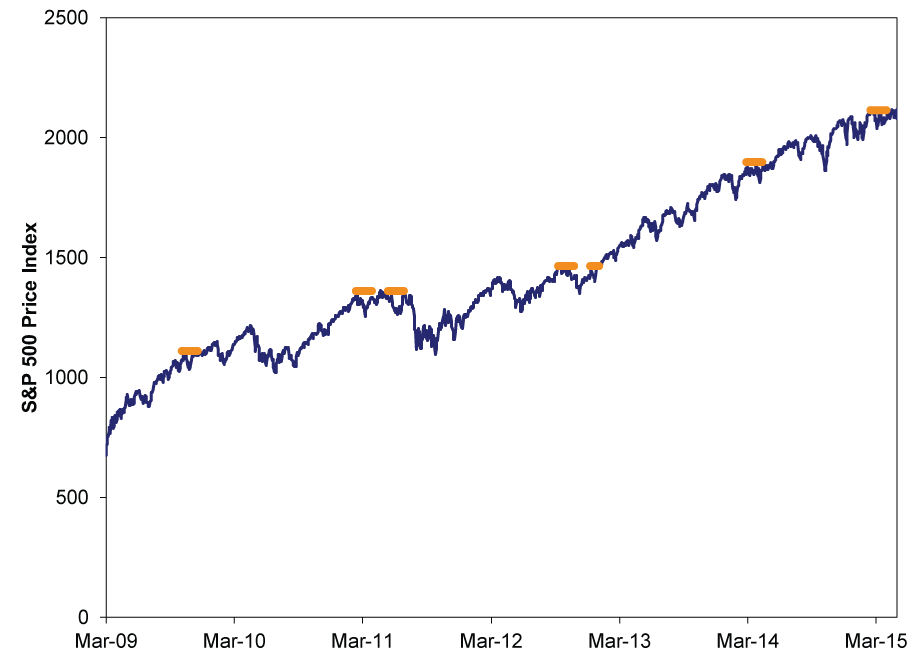

This is not the first time stocks have appeared to stall out at some random number during this bull market, as shown in Exhibit 2. Nor is there any discernible pattern to what stocks do after they bounce up against some arbitrary number for a few weeks. Sometimes they resumed rising straight away. Other times they pulled back a bit before eventually marching higher. None of it really means anything-it's all just stocks being stocks, moving on anything but past performance.

Exhibit 2: The S&P 500 Has Met Many Dotted Lines

Source: FactSet, as of 5/11/2015. S&P 500 Price Index, 3/9/2009 - 5/8/2015.

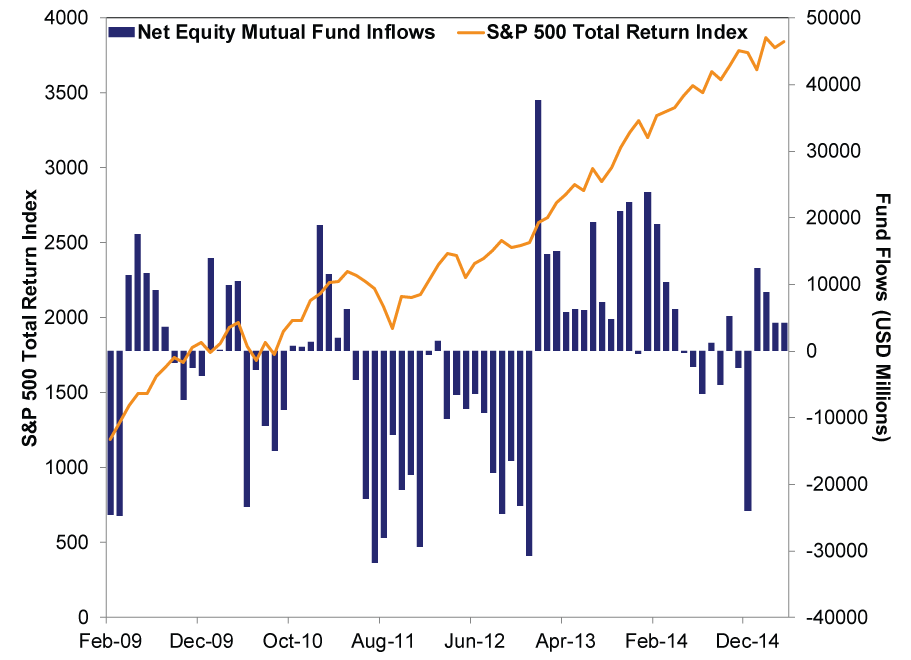

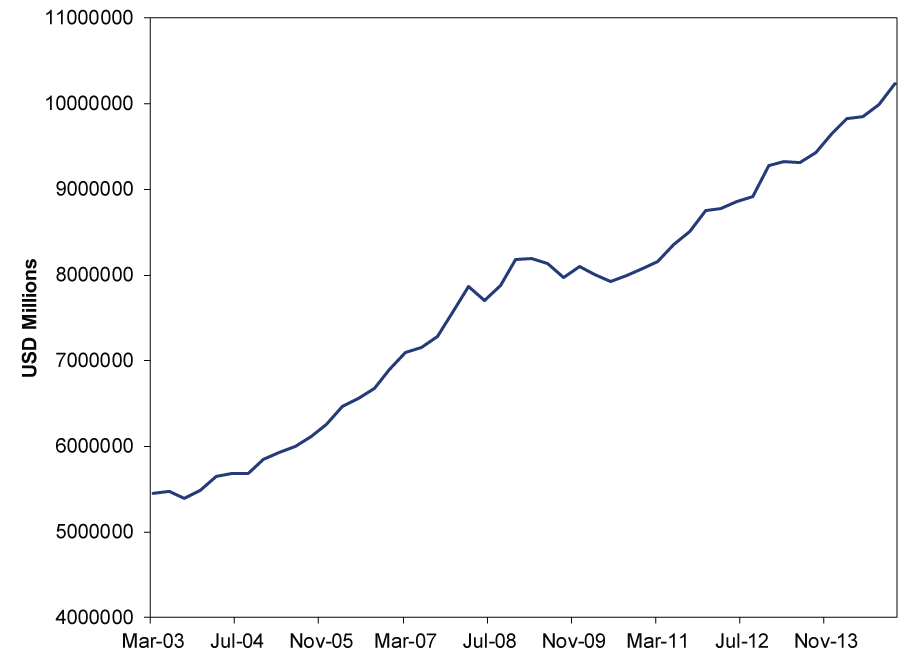

As for dry powder, this bull market's entire existence is testament to the fact stocks don't need some massive influx of retail-investor cash. As Exhibit 3 shows, equity mutual fund flows were negative for the bull's first month and much of its first three years. Household cash balances have risen since mid-2010, as shown in Exhibit 4.[ii]

Exhibit 3: Mutual Fund Flows Don't Drive Stocks

Source: FactSet, as of 5/11/2015. Net Equity Mutual Fund Inflows and S&P 500 Total Return Index, monthly, 2/28/2009 - 4/30/2015.

Exhibit 4: Cash Piles Up During Bull Markets

Source: Federal Reserve, as of 5/11/2015. Total cash on household balance sheets, quarterly, Q1 2003 - Q4 2014.

Repeat after us: Equity demand and dry powder/new money/sidelined cash aren't synonymous. Demand, always and everywhere, is investors' willingness to pay more for stocks. The money they use can come from stockpiled cash or bonds. But it can also come from stocks. If they sell one stock for the going rate, then use their proceeds to bid another stock up, that's rising demand! It makes prices rise!

Heck, when you get down to it, it is mathematically impossible for a net sum of new money to enter stocks. Every transaction is zero sum-money entering equals money leaving. Someone always crosses the spread between bid and ask.[iii] It doesn't always feel this way, because investors are prone to considering only their side of the transaction, but the market is just one big auction. It's bidding wars (or a lack thereof) that drive prices. Once the bidding is over, the deal is always consummated by buyer and seller. The money goes from one to other. It doesn't pile up inside the good sold.[iv] The high roller who bought Picasso's "Women of Algiers (Version O)" Monday didn't stash $180 million in the frame. They paid it to the seller.[v]

Anyway. Bad analogies aside, you don't need a flood of new money or buyers for stock prices to rise. Or any special catalyst. Stocks' natural tendency when fundamentals exceed broad expectations is to move up and to the right. That gap between reality and sentiment-positive surprise-is what gins up enthusiasm for future corporate profitability. Bull markets can run on and on until that gap gets negative and the surprises turn ugly. The time to fear the end is when worries are absent, expectations are sky-high, and reality can't possibly keep up. Not when worries are present, expectations are low, the economy is growing, earnings outside the Energy sector are positive, legislative risk is low, businesses are investing-and pundits are convinced stocks all these positives can't pierce a line on a graph.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] This phrase gives us the bizarre mental image of Margaret Thatcher hitting the campaign trail in 1979 wearing an Iron Maiden t-shirt.

[ii] Hey! We found the dry powder! Ka-ching!

[iii] This is why mutual fund flows are such a limited indicator. They don't show the other side of the trade. If investors leaving them used the proceeds to buy ETFs, is money really "leaving" stocks? But, we show them anyway, because ETF data are limited historically, and at least they show sentiment.

[iv] This is a terrible analogy, and we are sorry, and we blame Picasso.

[v] Ibid. We repent.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today