Personal Wealth Management / Market Analysis

RIP, Manufacturing Recession

Manufacturing's most recent soft patch may have passed.

As we enter the final month of the first half of the year, we would like to take you on a mental trip back to late 2015 and early 2016. Remember that five-month stretch when the US was mired in a "manufacturing recession?" Many presumed this heralded dark economic times and justified equity markets' volatility. But now, mere months later, that big ominous event appears to be just a soft patch that may have passed. We aren't saying manufacturing is now poised to rebound in a big way and lead economic growth. However, this is evidence that even the weaker areas of America's economy are trending upward-an overlooked positive.

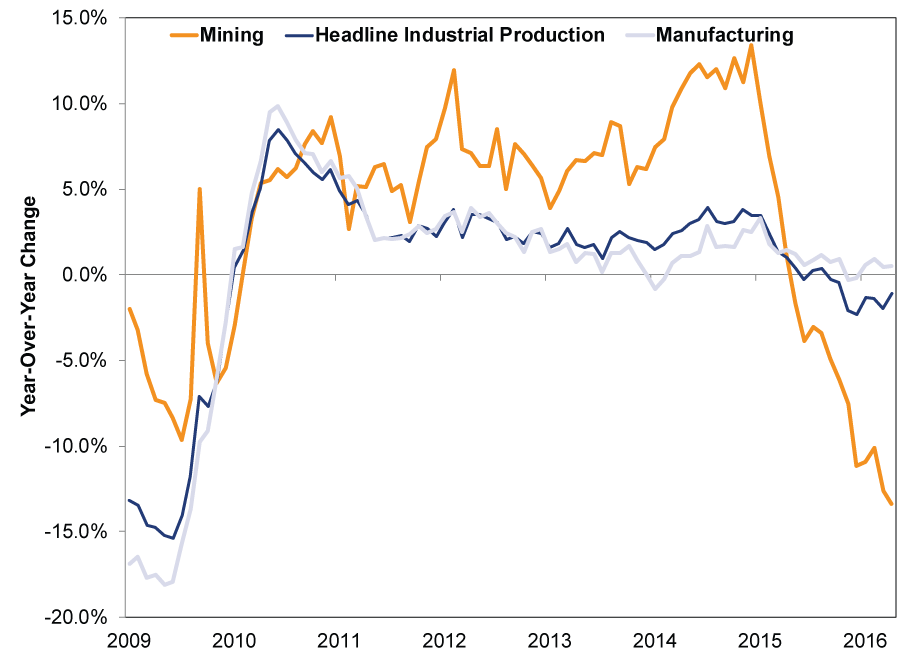

It was only a couple months ago when folks were freaking out about US manufacturing. The Institute for Supply Management's (ISM) manufacturing Purchasing Managers' Index (PMI) posted readings below 50 from October 2015 - February 2016-and results under 50 indicate more surveyed businesses contracted than expanded. Now, while headlines often refer to PMIs as indicating growth sped or slowed, they actually don't show that. These surveys show only how many respondents report growth or contraction, failing to capture the magnitude of growth.[i] That said, US industrial production (IP) numbers-which do tally output-also weakened around this timeframe. Weak overseas data added to worries. However, there was one well-known culprit dragging down these figures: plunging oil prices. ISM's manufacturing PMI, which includes the Petroleum & Coal Products industry (not drilling or mining, which are in the non-manufacturing survey, but the production of refined products), partly reflects oil's struggles. Likewise, IP contains Mining, which has had an outsized impact on the headline figure. In contrast, IP's Manufacturing subsector-which focuses on US factories-has been much steadier. (Exhibit 1)

Exhibit 1: Mining Has Put Industrial Production in the Hole

Source: St. Louis Federal Reserve, as of 6/2/2016.

The data suggest the most recent dip looks like a soft patch, not the start of broader overall weakening. We frequently recommend investors avoid reading too much into any month of data, good or bad. The same logic applies to shorter durations in general-a weak stretch doesn't necessarily mean deteriorating conditions are afoot.

Exhibit 2: An Industrial Soft Patch

Source: St. Louis Federal Reserve, as of 6/2/2016.

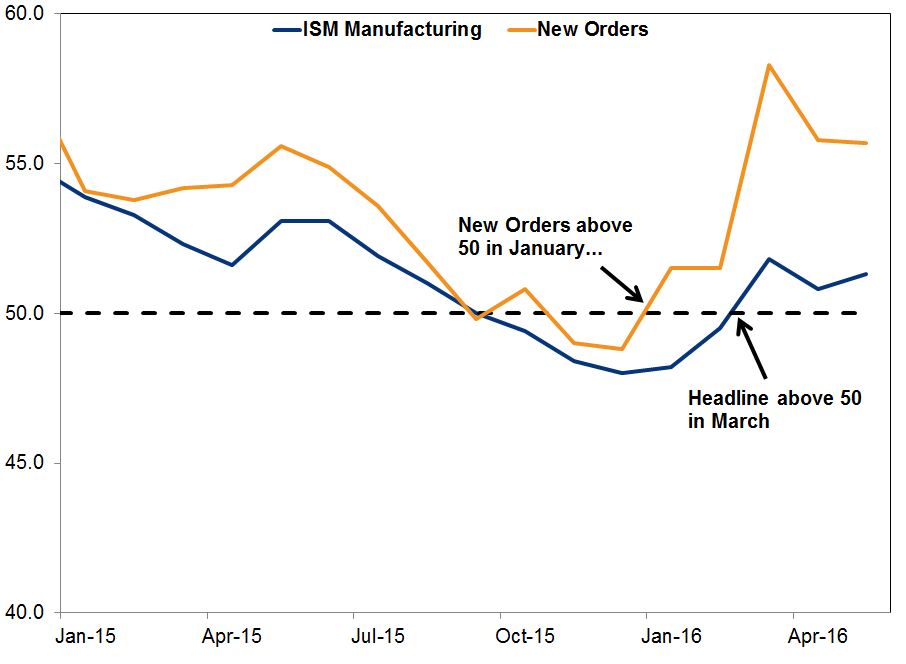

Similarly, ISM's manufacturing PMI appears to be enjoying a similar rebound-not a total surprise, given its New Orders subindex suggested a return to broad growth was likely.

Exhibit 3: Manufacturing PMI's Bounce

Source: St. Louis Federal Reserve, as of 6/1/2016.

We aren't arguing this all signals a big bounce back for US manufacturing-nor that this is even necessary for fine growth to continue. Manufacturing comprises just 12% of GDP, and the slammed Mining sector is less than 2%. Compare that to services industries, which make up almost 70%. However, growth in manufacturing is a sign that even the weaker parts of the US economy are doing all right-which should help boost sentiment a bit.

To start 2016, concerns about China and political uncertainty, coupled with low oil prices and their impact on industrial numbers, exacerbated worries about the state of the broader global economy. These factors knocked investor sentiment and likely contributed to market volatility at the year's onset. Markets have largely recovered since February 11, and manufacturing's improvement should help bolster the case that the US economy isn't floundering. Now regardless of what manufacturing does, its broader economic impact isn't as wide-ranging as headlines make it seem.

More broadly, this speaks to a theme that has persisted throughout the current economic expansion: The global economy is weak. This has frequently led to claims it needs help to keep growing, and just this week the Organisation for Economic Co-operation and Development (OECD) released a report stating governments need to do more to bolster growth-namely, through infrastructure spending. Whatever you think of this notion (we have our doubts such "stimulus" is necessary), for stocks, global economic growth is perfectly fine now. Though many fixate on economies heavily skewed toward commodities-hello, Brazil!-weakness isn't universal. Places like Mexico and Australia, which have sizable commodity-related sectors, have kept growing, boosted by domestic demand. Moreover, most of the world isn't commodity heavy-Emerging Markets and the developed world are overall expanding. For example, outside the US, the UK is chugging along despite Brexit concerns, the eurozone has grown for 12 straight quarters and Emerging Markets like India, China, Indonesia, Malaysia and many others are growing swiftly. With leading indicators suggesting more growth is likely, we believe sentiment will start to warm once investors recognize reality really isn't as bad as they think it is.

[i] But the media rarely lets context get in the way of a snappy headline.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today