Personal Wealth Management / Market Volatility

Rounding Up Europe’s New Response Measures

New restrictions are still far removed from early 2020’s lockdowns.

Volatility flared up again Monday, with the S&P 500 and most other major indexes globally down nearly -2%.[i] Most observers blamed news of COVID spikes and new restrictions in Italy and Spain, raising the specter of a second global lockdown. Germany’s IFO business sentiment survey, also out Monday, showed folks fear restrictions will soon bite there, too, and across the Continent, expectations are now for any GDP growth from Q3 to prove temporary and recession to resurge in Q4 as lockdowns tighten. That is one possible outcome, and a second sweeping worldwide lockdown could drive weakness. Yet in our view, it is worth noting how far we are from that outcome at the moment. There is another key difference between now and February, too: Then, a global lockdown was unthinkable, but now, with everyone expecting it, we suspect a lot of the surprise power is gone. That is key to consider as you weigh the potential market impact of COVID this autumn and winter.

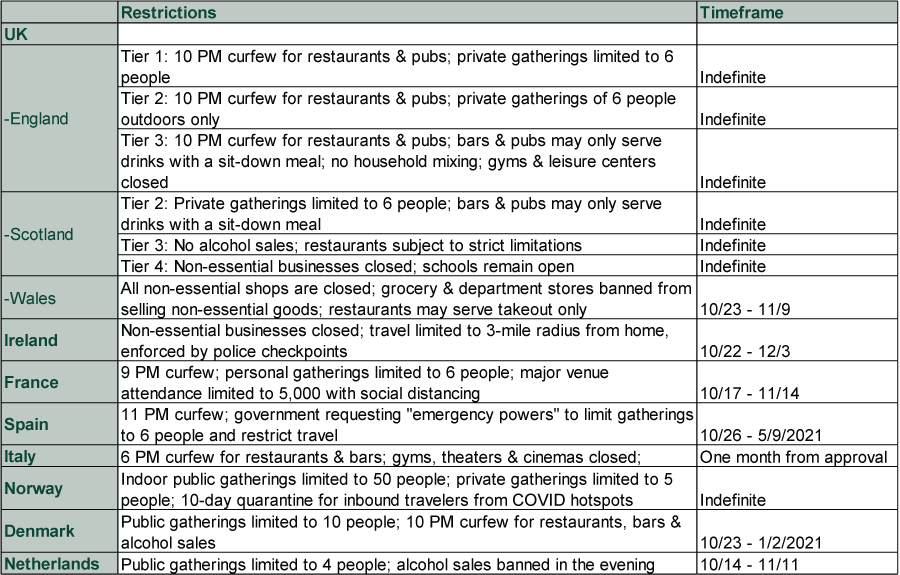

With the heightened rhetoric surrounding the latest restrictions on activity, it may be tough to get a handle on how draconian they are. Statements like Italy implements harshest restrictions since national lockdown ended are abundant and … not helpful, in our view. So to put everything in perspective, we have catalogued the latest restrictions from Continental Europe and the UK.

Exhibit 1: New Restrictions at a Glance

Source: The Telegraph, BBC News, Welsh government, NPR, French government, Financial Times, Reuters, Bloomberg, France24 and TheLocal.dk, as of 10/26/2020. Note: Spain’s curfew is set to expire nationally on 11/9. The emergency powers the government is seeking would last longer.

Schools and most offices that had reopened remain open in all of these places. Outside Wales and Ireland, officials have restricted operating hours, but they haven’t closed businesses outright. This is a world away from this past winter and spring, when non-essential businesses and bars were closed across the board, restaurants could only serve takeout and, in most nations, schools were shut. Today’s measures just don’t approximate those taken in the spring.

Of course, that could change. However, could isn’t will. Markets move on probabilities, not possibilities, and we think positioning your portfolio for a mere possibility is an error—especially if it involves raising the risk of being out of stocks while a bull market continues. The frustrating thing about lockdowns is that, as political decisions, they defy predicting. They aren’t market functions, and it is impossible to assign probabilities to them—there is too much of a human element. One thing that does seem clear, however, is that society is broadly not as compliant this time around. Anti-lockdown protests are escalating in most major European cities, which we suspect is affecting politicians’ appetites for more sweeping restrictions. Heads of government throughout the region are near-unanimous in stressing that they have no intention of reinstating a full-fledged second national lockdown. But their solution seems to be delegating decision making to local authorities or, in England and Scotland’s case, establishing various lockdown tiers that will apply to different areas depending on their caseloads. So just because national leaders say they don’t want lockdowns doesn’t mean they won’t eventually happen anyway.

We aren’t dismissing that risk, and we encourage readers to keep it in mind, as well. But we don’t think acting on that possibility today is likely to prove beneficial. Surprise is generally the swing factor for markets, and even with more lockdowns a risk, there seems to be a very high threshold for surprise right now. We always take sentiment surveys with a grain of salt, but Germany’s IFO survey seems instructive on this front. If the majority of businesses believe Q3 growth is a blip and renewed restrictions will take a severe toll—even as Germany is presently the one major European nation without big new restrictions—that says a lot about just how much pessimism is likely baked into stocks right now. It doesn’t prevent new restrictions from stirring sentiment and volatility at times, but in our view, the lack of surprise power makes it highly unlikely that a bear market is forming presently.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

Market Analysis Due Diligence and the DOL’s DOA Fiduciary Rule2026-03-13

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today